In downward trending markets as we have seen for much of 2022, it is important to distinguish price declines which may present similarly. Both index and active fundamental portfolios have moved, but not all securities move for the same reasons. Some investments move because fair value has declined; others move because they are getting “cheaper.” Because indices are designed to be measures of the current market, any market declines experienced in indexed portfolios are inherently a decline in fair value. However, it is the job of the fundamental investor to isolate those securities in which the underlying value is less volatile than security prices, buying as instruments get cheaper and selling as they reach or exceed fair value.

To this end, the job of the value investor is not just to find good companies but to find misunderstood companies. It is a sort of analysis arbitrage. The most attractive securities are those that are not just issued by strong companies but are also cheap. In an undulating market, a value discount can sometimes offset market movements and mitigate volatility. In a rising market, earnings can reveal the additional value to be found in an underpriced security. And when the market or economy is facing headwinds, that is the opportunity to separate the fundamentally challenged from the fundamentally cheap—to avoid the issuer which has experienced a fair value decline in favor of the issuer who has experienced merely a price decline.

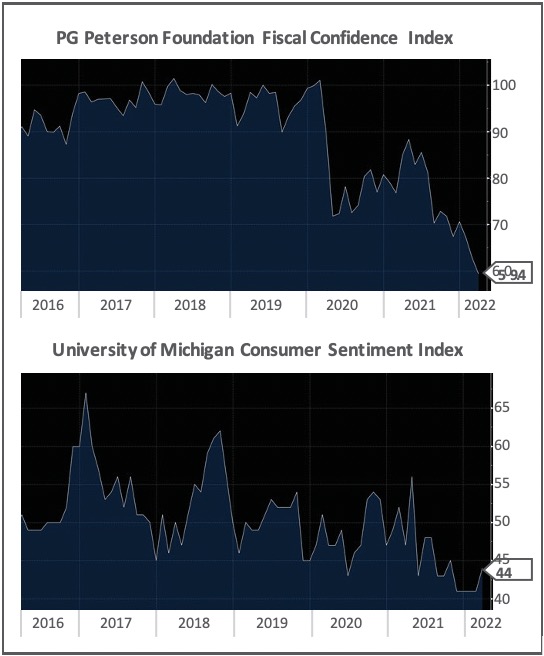

When we look at the economic environment today, this distinction is particularly notable. The first half of 2022 has been a headwind to all credit portfolios, fundamental or not. And there is no way to sugarcoat why. The risk of a recession in the near- to medium-term future is not low. Wage gains have not yet caught up with recent inflation, and the impact is being felt all across the country. However, that consumers are so aggrieved about higher prices tells us less about the purported opportunism of the small business owner as it does about the visceral impact of higher prices on people’s fiscal confidence. In fact, there is no shortage of indicators to show just that (see Figure 1).

As we have moved through the current earnings season, however, we are struck by two significant observations. First, we have seen the same dynamic we saw in mid-2020, where fundamentally attractive bonds which are not members of an index experienced price declines proportionate to the indices but have not yet experienced the same level of recovery. After all, issuers whose strength is demonstrated through earnings and not through the supply and demand of market indices get their momentum from quarterly earnings reports rather than in real-time based on market correlations. In addition, the types of value-oriented investors who buy such bonds in between earnings tend to be more opportunistic, taking more time to accept that the right price to pay is higher than the lowest price paid recently. This means the recovery period of these bonds is not as immediate as higher beta securities. As a result, yields in securities with a fundamental investment thesis are currently higher on average than the yield in market indices. This is not always the case and shows the relative opportunity through careful security selection in the current environment.

Figure 1: As of 3/31/2022, both the PG Peterson Foundation Fiscal Confidence Index (top) and the University of Michigan Consumer Sentiment Index (bottom) show a decided drop off in the financial confidence felt by consumers, as low as or even lower than at the depths of the COVID-19 pandemic. (Source: Bloomberg Finance LP)

However, this brings us to our second observation. Babies are getting thrown out with the bathwater, often for the very misunderstandings that fundamental investors aim to exploit. For example, recently, poor earnings from the company Bed Bath & Beyond caused the market to sell bonds issued by Michaels in sympathy. On the surface, the reasons were logical. Costs were higher, and supply chain issues were front and center. However, also evident in the resulting analyst reports was a failure to appreciate the difference in the two issuers’ underlying customers or the dynamics that drive those customers to shop. The comparison stopped at platitudes: They are both brick & mortar retail businesses with potential cost and supply issues due to inflation.

However, what Michaels demonstrated during the COVID-19 pandemic and resulting quarantine(s) is that it is a business which does well in economically challenged times. Despite the impact of recessionary fears and uncertainty on retail as a whole, crafters and other artists lean into their hobbies in such environments. Even more so than the shoppers looking for the types of basic supplies found at Bed Bath & Beyond, which can also easily be found on Amazon or at Target, the Michaels core customer has few alternatives. Meanwhile, where the Bed Bath & Beyond customer’s discretionary spending may be curtailed, the equivalent at Michaels tends to be seasonal or holiday. This does not mean consumers will not cut back, but as we’ve seen over the last two years, celebrating occasions where possible can be a release valve to the general feeling of strain on the pocketbook.

Often, when one thinks of opportunistic investors, one imagines hedge funds taking outsized risk and profiting if they are correct. However, there is another brand of opportunistic portfolio management which lies more in exploiting misunderstandings in the fundamental nature of a business. In this example, the underlying dynamics of these two companies are different, but the current market has treated them the same. It seems the conclusions of most analysts stop at a superficial view of a business and credit metrics. But therein lies the opportunity.

*****

Venk Reddy is the Chief Investment Officer of Sustainable Credit Strategies at Osterweis Capital Management. Established in 1983, Osterweis Capital Management is an independent asset manager with over $7 billion under management as of March 31, 2022. The firm provides investment management services to institutions and individuals through mutual funds and separate accounts, offering both equity and fixed income investment strategies. Learn more at www.osterweis.com.

Important Disclosure Information

Past performance is not indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by Osterweis Capital Management, LLC (“OCM”) or any non-investment related services, will be profitable, equal any historical performance level(s), be suitable for a specific portfolio or situation, or prove successful. Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your accounts; and, (3) a description of each comparative benchmark/index is available upon request. OCM is neither a law firm, nor a certified public accounting firm, and no portion of its services should be construed as legal, tax or accounting advice. Moreover, you should not assume that any discussion or information contained in this document serves as the receipt of, or as a substitute for, personalized investment advice from OCM. Existing clients should please remember that it remains your responsibility to advise OCM, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing, evaluating, or revising our previous recommendations and/or services, or if you would like to impose, add, or modify any reasonable restrictions to our investment advisory services. A copy of our current written disclosure Brochure discussing our advisory services and fees is available upon request or at www.osterweis.com. The scope of the services to be provided depends upon the needs of the client and the terms of the engagement.

Neither recognitions by publications, media, or other organizations, nor the achievement of any professional designation, certification, degree, or license, membership in any professional organization, or any amount of prior experience or success, should be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if OCM is engaged, or continues to be engaged, to provide investment advisory services.

© Osterweis Capital Management

Read more commentaries by Osterweis Capital Management