"Those who cannot remember the past are condemned to repeat it," wrote philosopher George Santayana in 1905. Investors in large-cap core index funds would be wise to heed his warning.

In 2020 and 2021 our organization produced over 100 pieces of empirically robust, historically informed and evidence-based research that appeared both on our website and peer reviewed journals. That work shed light on the most dire risks to investors in the most speculative markets we have seen in 55 years of collective money management. For a short while, going against the crowd was uncomfortable. For those who heeded our evidence-based philosophy and research, the majority of the steepest losses were avoided.

Over time we believe our safety-first approach to investing will help people compound wealth with less downside risk. While avoiding the devastating losses in the morass of overvalued loss-making firms has accrued to our readers’ benefit, this piece highlights what history and the data suggests will be the “next shoe to drop.” We believe there is an easily identified and easily avoided bubble in certain stocks due to the now-prevalent preference for the exclusive use of index funds.

Large Cap Stock Index Funds: Investment Objectives vs. Investment Results

The proliferation of low cost mutual funds and equity ETFs that replicate the large-cap indexes like the Dow Jones Index, S&P 500 Index and Russell 1000 Index have been a boon to investors. With management fees near zero and investment strategies based on the market cap of their constituents these funds are cheap and easy to explain. They have become a staple of investors’ portfolios for good reason.

Generally speaking, large-cap stocks are supposed to be a relatively safe bet. Investopedia says they "tend to be more stable and less volatile than smaller and younger companies." It adds that large-cap companies "generally reward investors with a consistent increase in share value and dividend payments."

In theory, that makes perfect sense. After all, these companies are typically well-established firms with proven business models. From an investment perspective, however, large-cap companies are more of a mixed bag than many people realize.

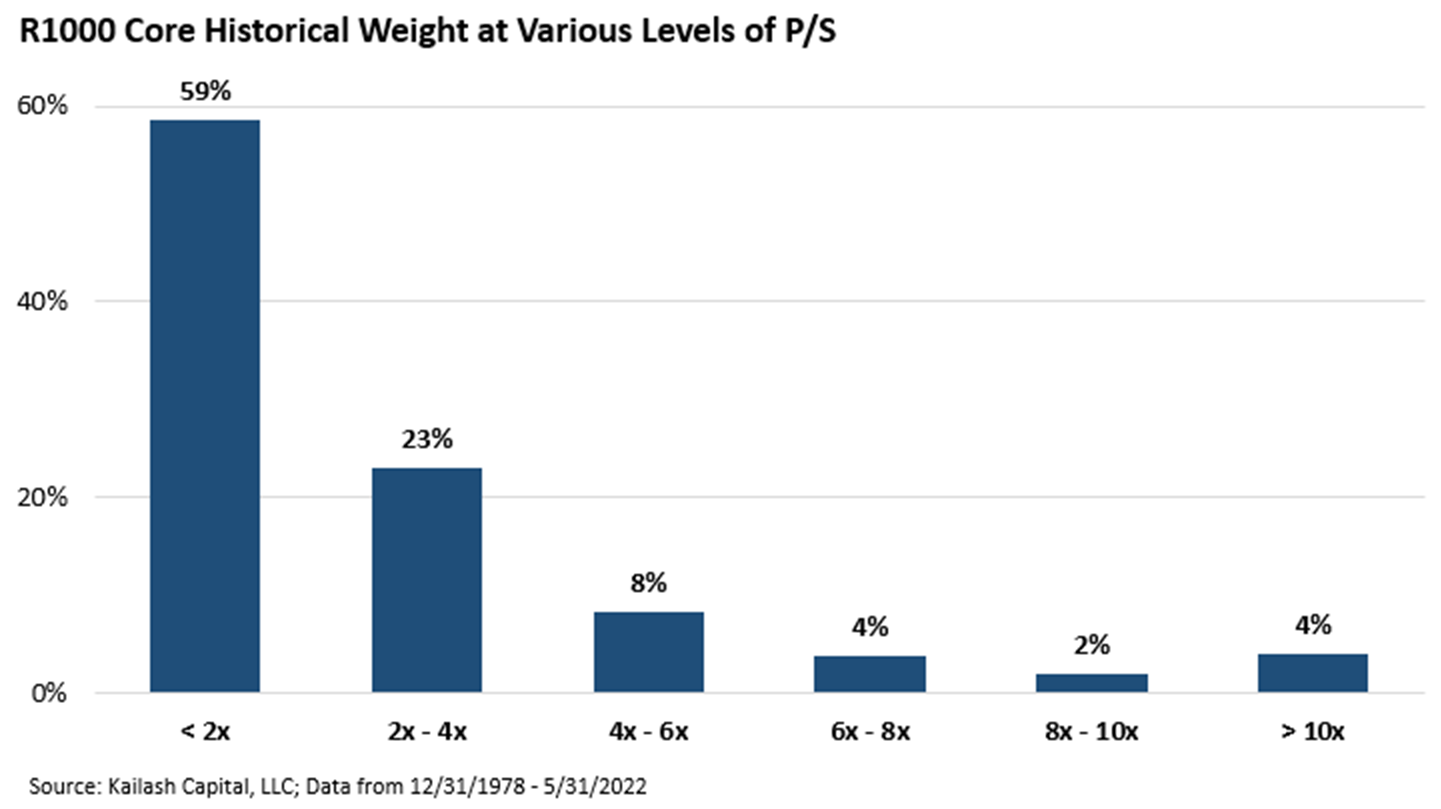

Let us explain, starting with the chart below. It shows the average price-to-sales (P/S) ratio for a typical large cap core index fund from December 1978 to May 2022. The P/S ratio = "market value per share" divided by "sales per share." So, the higher the price-to-sales ratio, the more you are paying for the underlying business.

As recent market action has reminded investors: what you pay for an asset matters.

Historically, investors in large-cap core equity funds had:

- 57% of their money invested in stocks valued at less than 2x price to sales

- 22% of their money invested in stocks valued between 2x - 4x price to sales

- The next three bars combined, covering stocks between 4x – 10x price to sales, sum to only 14% of investors’ money (8% + 4% + 2% = 14%)

Look at the last bar on the right. Over history only 4% of an investors’ money has typically been invested in stocks valued at over 10x price to sales.

A P/S ratio of 10x or more is a major red flag for investors. Scott McNealy, co-founder of Sun Microsystems made the dangers of buying stocks at these valuations painfully clear as the wreckage of the dot.com bubble unfolded.

We highlighted his famous 2002 quote on the precarious merits of stocks at these valuations in our recent missive on Tesla. Over the past four decades, investors in large-cap core index funds have generally had limited exposure to stocks valued over 10x price to sales. Which, based on every empirical study we have seen, is a good thing.

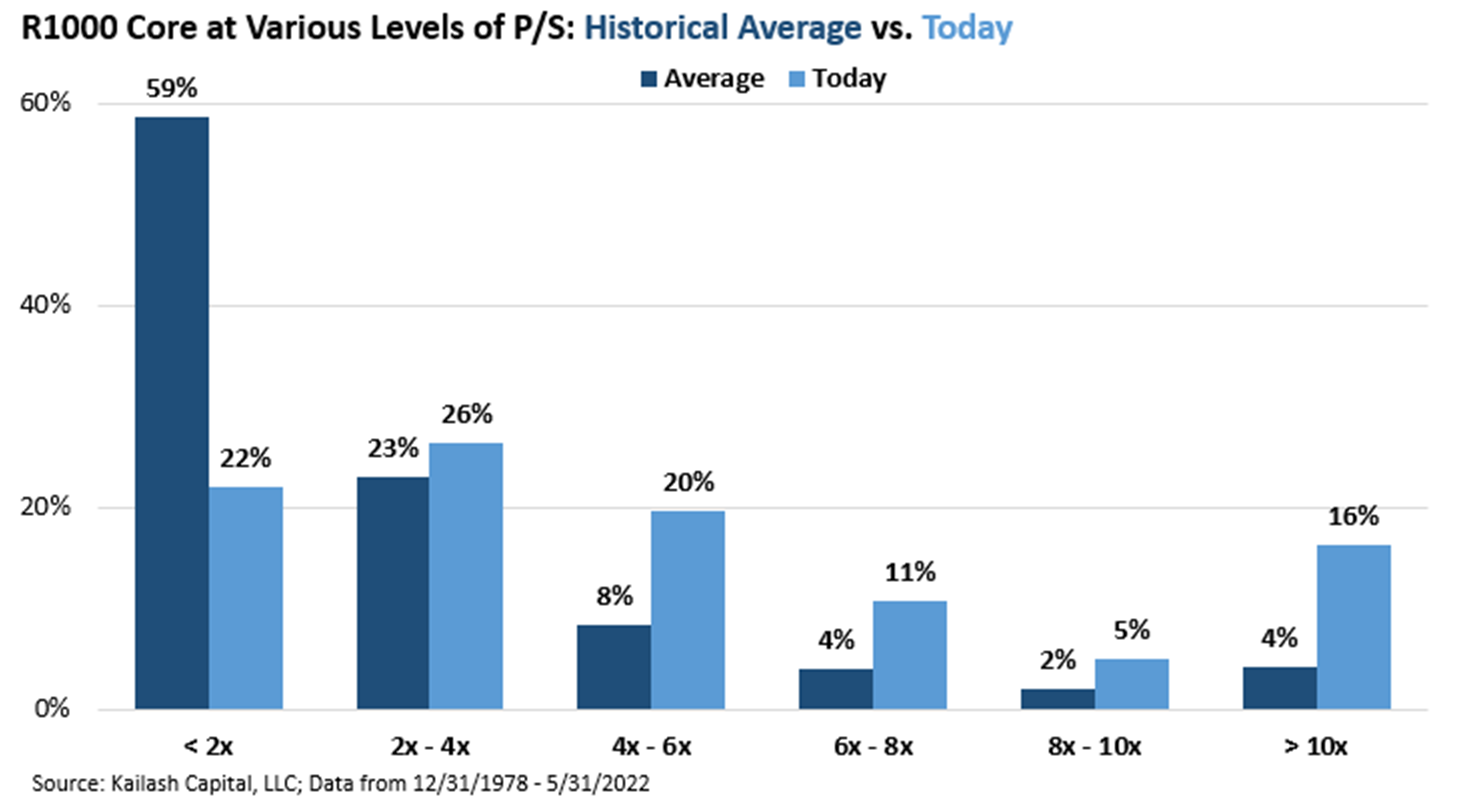

Recently, though, large-cap core index funds have taken on valuation structures that one might expect of a growth fund. In a nutshell, exposure has shifted away from stocks with low valuations (<2x price to sales, left-most bars) toward the dangerously overvalued (>10x, right-most bars).

This shift is a byproduct of human behavior around investment preferences. In the bull market that raged through 2021, money poured into index funds. Since the majority of index funds are market cap weighted, these relentless inflows create an unfortunate and self-fulfilling prophecy.

The largest stocks in the index get a larger portion of each dollar invested. As the money flows accelerate, this creates ever larger buy orders of the largest and most expensive firms. Eventually this can become a self-reinforcing cycle driving the biggest and most expensive firms higher. This becomes a self-perpetuating cycle.[i]

If we described an investment product where the method of allocating your money was the bigger and more expensive a stock the more of it you would buy, would that be an appealing product? This conflicts with common sense, the law of large numbers, and the vast body of peer reviewed literature on the role valuation plays in long-run equity returns.

This leaves owners of large cap core index funds with unusual and outsized exposure to stocks with valuations historically associated with poor future returns. Worse, should flows to index funds slow or reverse as they have in the past, the cycle of relentlessly pushing the index’s largest stocks higher will reverse.

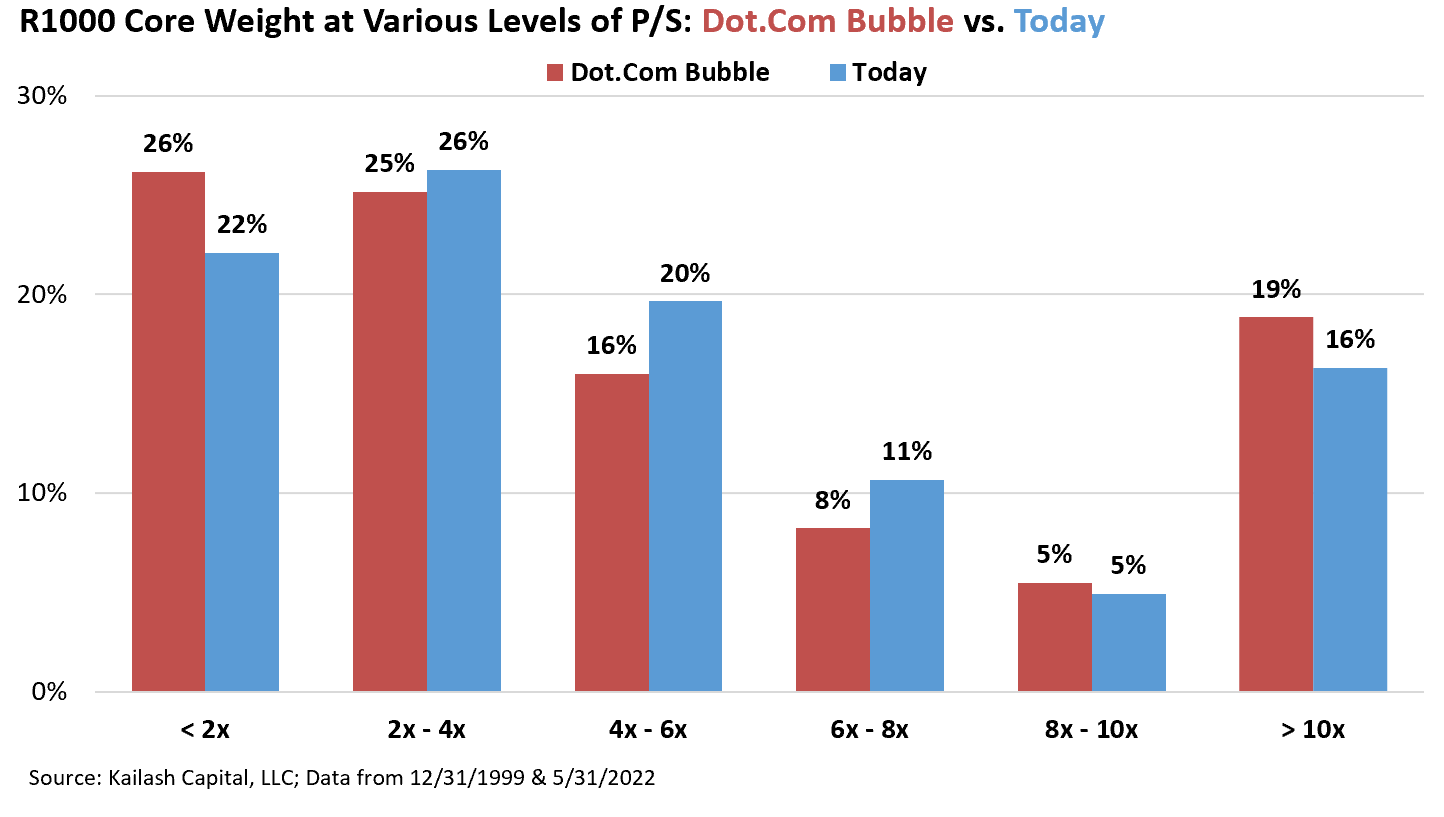

That brings us back to Mr. Santayana's immortal quote. Think back to December 1999 when the dot-com bubble was nearing its peak. Then, as now, investors in large-cap core index funds had a disturbingly high proportion of their money exposed to stocks exceeding a 10x P/S ratio.

The chart below shows investors’ exposure at various levels of valuation in December of 1999 (red bars) and today (blue bars). This is not complicated.

What you pay matters over the long run.

The similarities between 1999 and today are eerie. And that's a cause for concern, given the precipitous crash that wreaked havoc on so many portfolios in 2000-2002.

Make no mistake: A responsibly managed, low-cost index fund has its place in a well-constructed asset allocation portfolio. The portfolio managers who write for Kailash Concepts (“KCR”) even sub-advise a low fee all-cap index fund that tracks the total stock market. But unless you're comfortable with your clients having 16 cents of every dollar invested in companies whose valuations defy logic, it's time to recommend a change of course before history repeats.

The active investment management landscape has been dominated by stories of briefly famous forecasters who generated catastrophic performance data. This is truly unfortunate as these speculative vehicles have occluded the benefits of an emphasis on total returns through a market cycle.

KCR believes that with large cap equity index funds’ bloated valuations, the importance of engaging with a low-cost, low-turnover, and tax-efficient money manager has never been more important.

For more, please visit Kailash Concept’s website.

[i] We understand that some may object to our use of price to sales as this valuation metric does not adjust for a firm’s profitability or margins like a price to earnings ratio. To head-off such concerns, we would note that, according to Bloomberg, the stocks with a P/S ratio above 10x in the popular SPY ETF have a P/E ratio of 41x earnings. For further context the remaining stocks in the index have a P/E ratio of only 18x. Data from Bloomberg using the SPY ETF in the portfolio characteristics function.

© Kailash Concepts Research

Read more commentaries by Kailash Concepts Research