It’s time for our annual August report, “Charts for the Beach.” Each year we highlight five of our favorite charts we think consensus is currently overlooking. Load up the cooler, get your towel and chair, and enjoy the charts! And, watch out for those sharks!!

The “mathematical” recession

We’ve often suggested investors ignore politics. Politics is about what should be, but investing is about what is. Dispassionate portfolio positioning based on fundamentals, not politics, is critical to being a good investor. The current political debate whether the economy is in recession or not seems one of those irrelevant topics to which investors are paying too much attention.

There is no doubt the economy is in a “mathematical recession” because GDP growth has been negative for two quarters (assuming no revisions to the current data), but there is also no doubt that the economy is strongly creating jobs. That is an unprecedented combination.

Our first chart (courtesy of The Daily Shot) shows the contributors to real GDP growth. The primary drivers of a mathematical recession have been 1) retailers’ poor inventory management when consumers rapidly changed their buying patterns after being locked-down, and 2) trade because relatively few consumer goods are actually produced in the US.

With employment still growing strongly, investors need to consider whether the mathematical recession will provide the weakness in demand needed to curtail inflation. We’re skeptical.

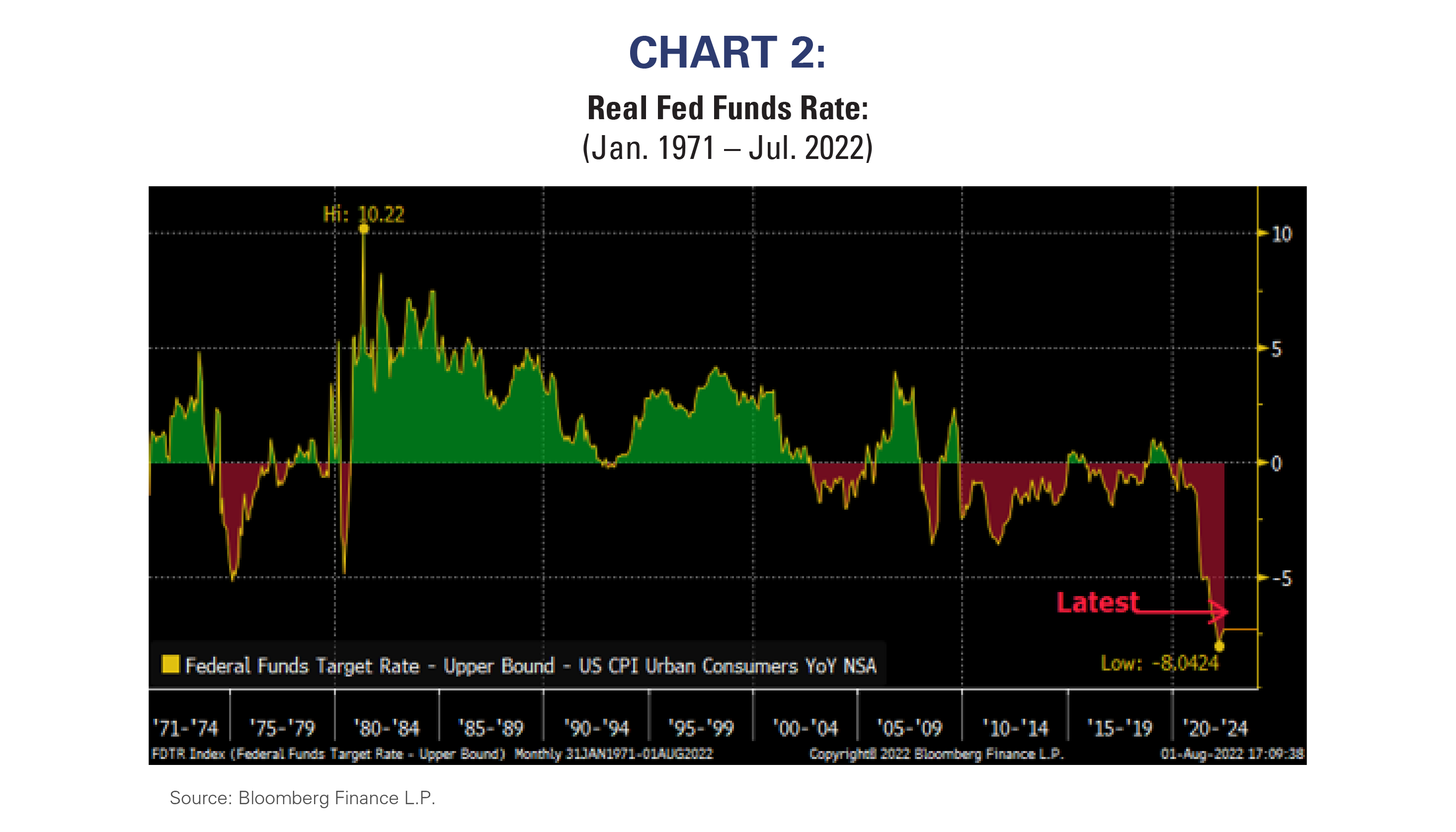

The Fed is historically behind inflation

The real Fed Funds rate (i.e., the Fed Funds rate less the inflation rate) has historically been a reliable measure of the tightness of monetary policy. A positive real Fed Funds rate suggested the Fed was tight, whereas a negative one implied monetary policy was easy.

Our second chart shows the real Fed Funds rate through time. The long-term average is about 1% and the real Fed Funds rate peaked at about 10% during the famous Volcker anti-inflation monetary regime.

Recent monetary policy has gotten tighter in response to the highest inflation rates in 40 years. However, the current real Fed Funds rate suggests monetary policy remains remarkably easy relative to inflation. In fact, the real Fed Funds rate is more negative today than after the Global Financial Crisis.

This implies the Fed is historically behind inflation, inflation might be more stubborn than investors expect, and the tightening cycle might last longer than is currently consensus.

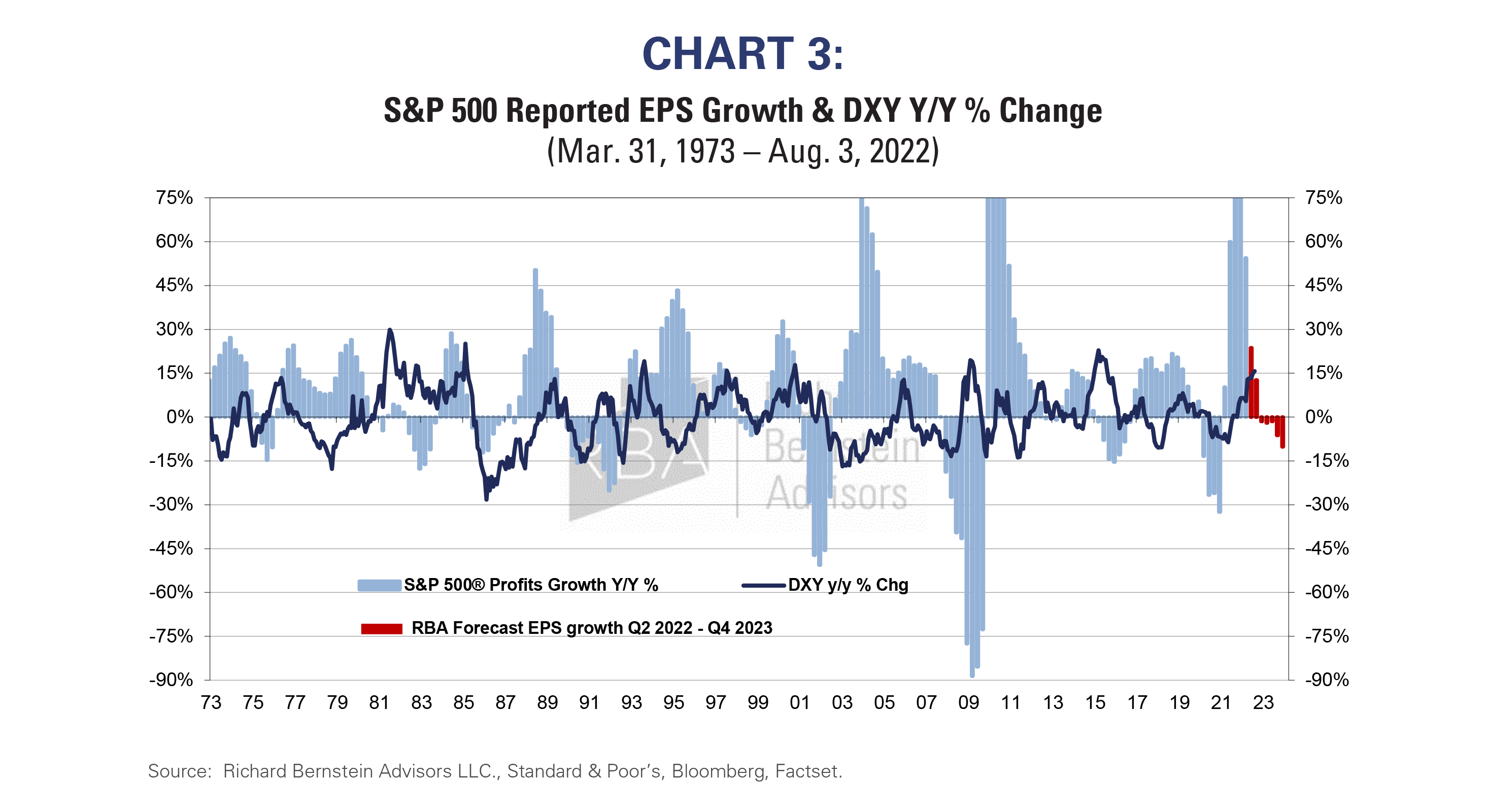

USD strength may mean earnings trouble ahead

The recent strength of the US dollar is not a good sign for earnings. Historically, when the DXY Index (see Chart 3) has appreciated 15% y/y or more, a profits recession has typically followed within one to four quarters thereafter. 1993 and 2009 were the rare exceptions.

The DXY recently pierced that 15% ceiling. RBA’s forecast has been for a full-blown profits recession by 1H23, and the dollar’s recent strength seems to strongly support that forecast.

Investors seem to believe the stock market may have already discounted the fundamental deterioration, however, such thoughts may be premature. First, the profits cycle is still quite strong. S&P 500® Trailing GAAP earnings growth is still up nearly 25% through the 2nd quarter. Second, the most foreign exchange exposed sector is Technology, which remains the favorite of many investors despite the potentially significant earnings headwinds coming from the strong dollar.

Chart 3: S&P 500 Reported EPS Growth & DXY Y/Y % Chg

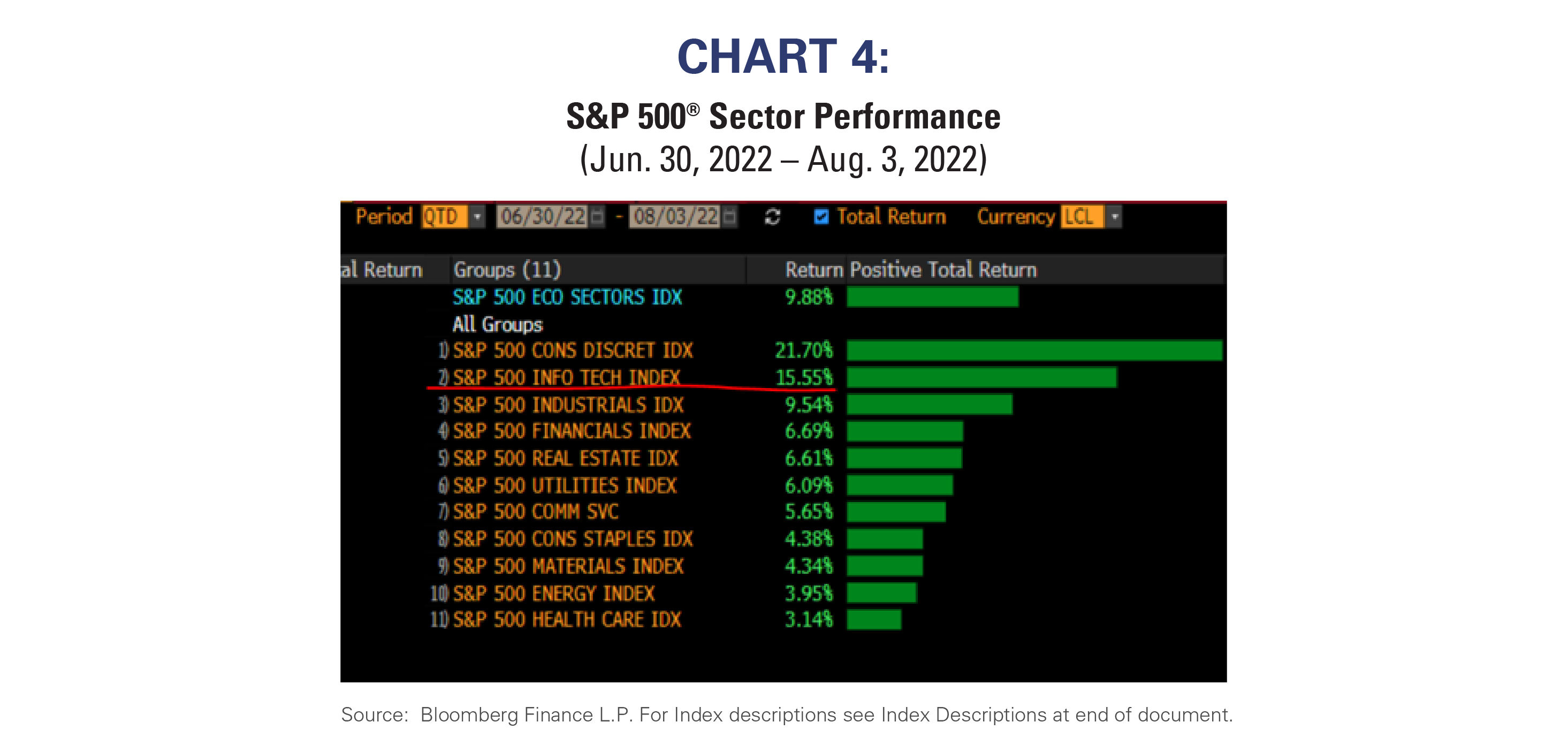

Bull markets don’t start with narrow leadership

Some investors believe the stock market’s recent rally signals a new bull market. We are skeptical because bull markets never begin with narrow leadership.

Stock market leadership is generally quite broad at the beginning of a bull market because the overall economy begins to improve and economic tailwinds benefit the broad economy. Leadership typically narrows as the cycle matures because tailwinds slowly become headwinds for an increasing number of companies. Leadership accordingly tends to be its narrowest at the end of a cycle.

The recent stock market rally has been extraordinarily narrow. As Chart 4 highlights, only 2 of the 11 S&P 500® sectors have outperformed. While speculators and day traders might be enjoying the rally, fundamental investors might want to be more cautious.

Don’t invest myopically

Investors are still mesmerized by the speculative growth themes of technology, innovation, and disruption, and their potential investments seem quite myopic. They can’t imagine investing in non-US stocks or in stocks in sectors other than those attention-grabbing sectors.

Old habits may die hard, and they appear to be increasingly missing out on potential investments outside the US. Chart 5 shows the year-to-date total return of NASDAQ compared to the MSCI World ex US Index, the MSCI Emerging Markets ex China Index, and the MSCI ACWI Natural Resources Index. All three of those indices have significantly outperformed NASDAQ this year, and the Natural Resource Index is actually positive for the year.

INDEX DESCRIPTIONS:

The following descriptions, while believed to be accurate, are in some cases abbreviated versions of more detailed or comprehensive definitions available from the sponsors or originators of the respective indices. Anyone interested in such further details is free to consult each such sponsor’s or originator’s website.

The past performance of an index is not a guarantee of future results.

Each index reflects an unmanaged universe of securities without any deduction for advisory fees or other expenses that would reduce actual returns, as well as the reinvestment of all income and dividends. An actual investment in the securities included in the index would require an investor to incur transaction costs, which would lower the performance results. Indices are not actively managed and investors cannot invest directly in the indices.

S&P 500®: S&P 500® Index: The S&P 500® Index is an unmanaged, capitalization-weighted index designed to measure the performance of the broad US economy through changes in the aggregate market value of 500 stocks representing all major industries.

Sector/Industries: Sector/industry references in this report are in accordance with the Global Industry Classification Standard (GICS®) developed by MSCI Barra and Standard & Poor’s.

Nasdaq: The Nasdaq Composite Index: The NASDAQ Composite Index is a broad-based market-capitalization-weighted index of stocks that includes all domestic and international based common type stocks listed on The NASDAQ Stock Market.

MSCI EM ex China: MSCI Emerging Markets ex China Index. The MSCI EM ex China Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of emerging markets excluding China.

MSCI ACW Select Natural Resources: The MSCI ACWI Select Natural Resources Index (“Index”) is designed to represent the performance of listed companies within MSCI ACWI that own, process and/or develop natural resources, namely materials or substances occurring in nature.

© Richard Bernstein Advisors

Read more commentaries by Richard Bernstein Advisors