Forward Guidance Failures

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWe Can Hear You Now

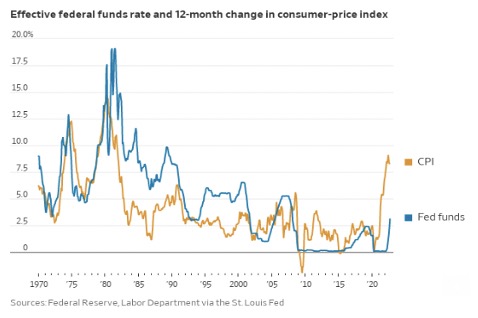

One of the themes I’ve discussed in recent months is the disconnect between a 40 year high in inflation and the lack of experience money managers have in understanding the monetary policy required to deal with such high inflation, including managers with 25 to 30 years of experience. The views of the majority of money managers in 2022 have been shaped by the last 20 years. Money managers learned that when the going got tough the Federal Reserve always came to the rescue. This experience generated the fervent belief in the “Fed Put”. What they haven’t understood in 2022 was that the Fed was previously able to respond with accommodation when trouble appeared because core CPI inflation stayed below 2.5%.

More importantly, the Federal Reserve’s preferred inflation gauge is the Core Personal Consumption Expenditures Index (PCE) and, other than the period of 2004 – 2007, the Core PCE has been less than 2% since 1996. That changed in 2022 but money managers have expected the FOMC to respond as if inflation was still hovering near 2.0%.

The FOMC publishes the minutes of its meetings 3 weeks after a meeting and it’s common for the minutes to show a decent level of discussion and at times a disparity between various members’ views. Often the Doves and Hawks on the FOMC express an opposing view of what the appropriate policy should be. (Think of Dove Kashkari, and Hawk Bullard) This is why the uniformity in the past six months is noteworthy. Rather than different members offering contrasting views about future monetary policy in speeches and interviews, there has been broad agreement. The Federal Reserve believes Forward Guidance plays an important role in communicating to financial markets the direction of monetary policy. The FOMC believes that its Forward Guidance will minimize surprises and prevent excessive volatility.

The heavy use of Forward Guidance last year by the FOMC created a huge problem for the FOMC in 2022, as countless speeches expressed confidence that inflation would be transitory proved spectacularly wrong. This big miss damaged the FOMC’s credibility. In March and April there was broad agreement by FOMC members that the FOMC would increase the Funds rate to the neutral level (2.50%) as expeditiously as possible. Initially financial markets didn’t believe the FOMC would act decisively. When the markets finally realized the FOMC would follow through, the S&P 500 dropped from 4600 in early April to 3637 in June, and the 10-year Treasury yield jumped from 2.42% in April to 3.47% in June. This is an example of investors not heeding the FOMC’s Forward Guidance, even when the messaging is explicitly clear. In April Forward Guidance failed because investors failed to hear the FOMC’s message and doubted the FOMC’s conviction to deliver.

The second and opposite problem is when investors pay too much attention. The emphasis the FOMC has placed on Forward Guidance has created a dependency issue for markets that has become obvious in recent months. This excessive dependence has created a monster as investors scrutinize every phase for the slightest hint for future monetary policy. When Chair Powell didn’t confirm that another 0.75% increase in the Funds rate was coming in July, the financial markets inferred that Powell’s deflection meant the FOMC would only increase the Funds rate by 0.50% instead of 0.75%. The S&P 500 rallied from a low of 3722 in mid July to a high of 4325 on August 15.

On August 25 Chair Powell used his Jackson Hole speech to emphasize that the FOMC would restore the FOMC’s credibility and level of conviction. “Our responsibility to deliver price stability is unconditional. Without price stability, the economy does not work for anyone. In particular, without price stability, we will not achieve a sustained period of strong labor market conditions that benefit all. The burdens of high inflation fall heaviest on those who are least able to bear them. We will keep at it until we are confident the job is done.” In the wake of Powell’s speech the S&P 500 fell from 4202 to 3837 on September 16.

In the weeks leading up to the September 21 FOMC meeting the messaging from FOMC members in their speeches and interviews was uniformly clear: The FOMC will increase the Funds rate to a modestly restrictive level and then hold it there for a long time to avoid the policy mistakes made in the 1970’s. I discussed the ramifications of those mistakes in the September Macro Tides. As inflation increased from the late 1960’s to 1979, the FOMC jacked up the Funds rate aggressively, only to reverse course quickly after recessions developed in 1970, 1974, and 1980. This Stop – Go policy allowed inflation to keep trending higher, until Chair Paul Volker brought inflation down decisively after increasing the Funds rate to 20%. A deep recession ensued in 1982 and the Unemployment Rate jumped to 10.6%, so the success in taming inflation came at a high cost. The current members of the FOMC believe that by not increasing the Funds rate too much, so that a recession can be avoided, and then holding the Funds rate at that level in 2023, inflation will fall and the Unemployment Rate will go up so that wage growth moderates. I’ve dubbed the FOMC’s game plan as ‘Hike and Hold’.

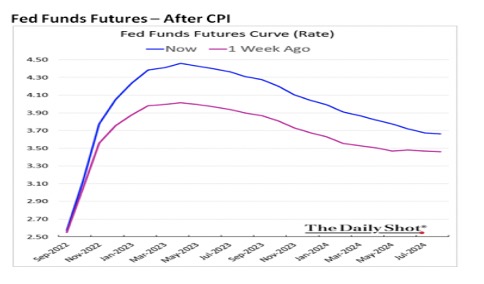

Despite the clear messaging by the FOMC, the Federal Funds Futures market expected the FOMC to lower rates in the second quarter of 2023. What’s more the shape of the curve for the Funds Futures didn’t change, even after the dismal inflation news delivered by the August CPI report. The only difference was that the peak in the Funds rate increased to 4.47% from 3.95% before the CPI report.

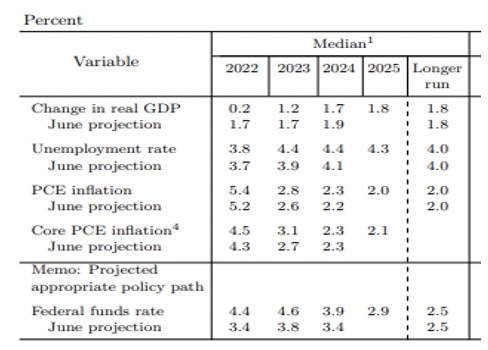

To get Wall Street’s attention, and make it clear that the FOMC would increase the Funds rate and hold it at a modestly restrictive level, I thought the FOMC might use the Dot Plot from the September 21 FOMC meeting to make their point about their Hike and Hold policy. “FOMC members could use the Dot Plot to reiterate the Hike and Hold strategy to further push back against the outlook conveyed in the Federal Funds Futures. Sooner or later the Federal Funds Futures will align with what the FOMC members have been saying and the Dot Plot is likely to advance the learning curve.” When the FOMC projections were released on September 21, the message was clear and financial markets finally woke up – We Can Hear You Now. The Median projection for the Federal Funds rate at the end of 2022 was increased to 4.4% and 4.6% at the end of 2023. The FOMC didn’t indicate that it would lower the Funds rate until the sometime in 2024 and it would be 3.9% at the end of 2024. The S&P 500 traded up to 3907 in the minutes after the FOMC rate announcement, only to fall to 3584 on September 30 This is the third time in the last six months that investors didn’t heed the FOMC’s Forward Guidance, even though the messaging was explicitly clear.

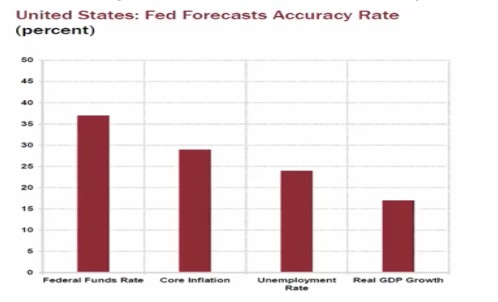

The Federal Reserve should drop Forward Guidance since it is helpful maybe 1/3 of the time. Either the FOMC makes a bad assessment (transitory), or the financial markets misinterpret or simply fail to grasp the import of the message. The FOMC and the financial markets occasionally synch up and the message is correctly received. Since the goal is to eliminate uncertainty and lower volatility in financial markets, the record indicates that it fails the majority of the time. The FOMC’s track record in forecasting the Federal Funds rate, Core inflation, Unemployment Rate, and Real GDP is awful. This is the primary reason why the FOMC should ditch Forward Guidance, besides saving them the embarrassment. Estimating GDP, Core Inflation, and the Unemployment Rate are not under the FOMC’s direct control. Being off a little is understandable. But the FOMC has total control over the Federal Funds rate and the accuracy of the forecast should be excellent. After David Rosenberg reviewed the history of FOMC projections, he found that’s not the case. The FOMC has gotten GDP correct less than 20% of the time, less than 25% for the Unemployment Rate, and was accurate less than 30% for Core inflation. The FOMC’s projection for the Federal Funds rate was correct just 37% of the time. This is a shockingly low number but think about how accurate the FOMC’s projections have been this year. In March the projection for the Funds rate at the end of 2022 was 1.9% and now it’s 4.4%. The FOMC was off by more than 100% in less than 6 months, which is no rounding error.

Soft Landing? Not Likely

The FOMC has been pitching the possibility of a soft landing all year and the September projections show they are still clinging to that hope (delusion?). The Median projection for GDP in 2022 was lowered from 1.7% in June to just 0.2% in September, which is a significant deceleration in economic activity. However, the FOMC thinks GDP will rebound and average 1.2% for all of 2023. This estimate will be coming down as the risk of a recession in 2023 is high, especially if the FOMC increases the Funds rate to 4.4% by the end of 2022 and holds it at 4.6% for most of 2023.

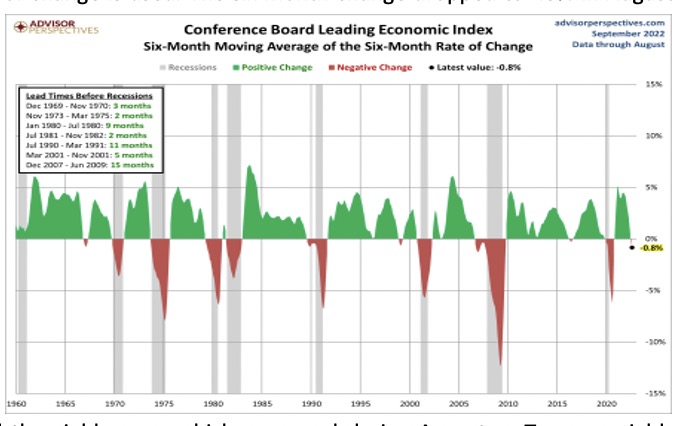

As I have discussed many times, the best recession indicator is the Leading Economic Indicators (LEI). I prefer it over the 10-year Treasury yield minus the 2-year yield curve, since it is comprised of 10 separate economic activity measures including the 10-year Treasury yield minus the Federal Funds rate. These are the 10 components:

Average weekly hours in manufacturing; Average weekly initial claims for unemployment insurance; Manufacturers’ new orders for consumer goods and materials; ISM Index of New Orders; Manufacturers’ new orders for nondefense capital goods excluding aircraft orders; Building permits for new private housing units; S&P 500 Index of Stock Prices; Leading Credit Index; Interest rate spread (10-year Treasury bonds less federal funds rate); Average consumer expectations for business conditions.

The main reason I prefer the LEI over the Yield Curve is its timeliness. The LEI has provided a recession signal about 10 months prior to a recession compared to a lead time of 19 months for the 10-year minus the 2-year Treasury yield curve. The lead time drops to 6.7 months for the LEI when a six month rate of change is used. The six month change dropped to -.8% in August so a recession is likely to start before the middle of 2023. The LEI has fallen for six consecutive months adding weight to the current recession signal. (Chart compliments of Advisors Perspective) Of the ten subcomponents only two were positive, so the breadth of the decline is broad. The two positive factors were initial unemployment claims and the yield curve, which narrowed during August as Treasury yields across the curve fell. The labor market is going to weaken in coming months, so initial unemployment claims will become a negative contributor to the index. In the wake of the September 21 FOMC meeting the yield curve has become more negative, so it won’t be positive either.

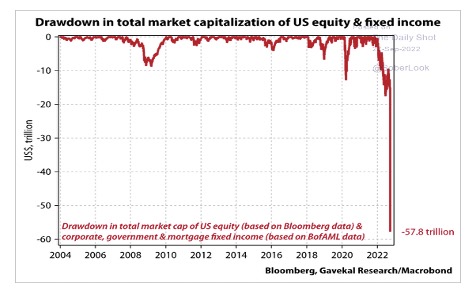

The most common investment portfolio allocates 60% to stocks and 40% to bonds. A low cost way to achieve that allocation is to put 60% in the Vanguard Total Stock Market ETF (VTI) and 40% in the Vanguard Total Bond Market ETF (BND). Through September 30 the stock ETF VTI is down -26.10% and the bond ETF BND has lost -15.30%, so the 60%/40% portfolio allocation is down -21.80%. For the majority of investors this is a shock and this loss certainly won’t inspire more spending, and will cause a cutback. The top 40% of wage earners may have accumulated more savings in 2020 and 2021, but for most the decline in the value of their portfolio is larger. When the losses in stock and bond market are combined, the total loss is almost $8 trillion. During the financial crisis and the early stages of the Pandemic, Treasury bond prices increased in value which offset stock market losses. The opposite has happened in 2022.

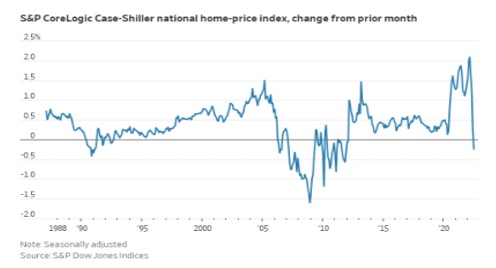

According to the Census Bureau the median home price in the US increased from $327,100 at the end of 2019 to $440,300 on June 30, 2022 a jump of 34.6%. The surge in home values has made homeowners feel pretty good, but that’s about to change. For the first time since March 2012, the monthly change in the Case-Shiller Home Price Index declined in July from June. The 20-City Composite fell -0.44% and the annual increase declined from 18.1% in June to 15.8% in July, which is the largest monthly decline (-2.3%) since the January 1987. The dip in the annual rate of change is understandable given the enormous increase in home values, and won’t begin to really hit home until the annual change becomes negative. For those who purchased their home before the end of 2019, median home price would have to fall more than 25% just to get back to 2019 prices. Median home prices would have to decline by -13.1% to drop to the June 30, 2021 median price of $382,600. What are the odds of a drop of -13.1%?

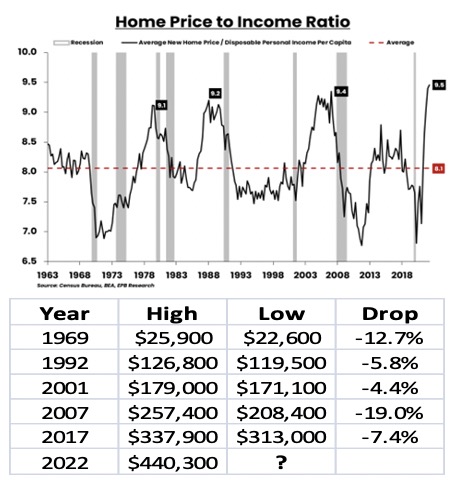

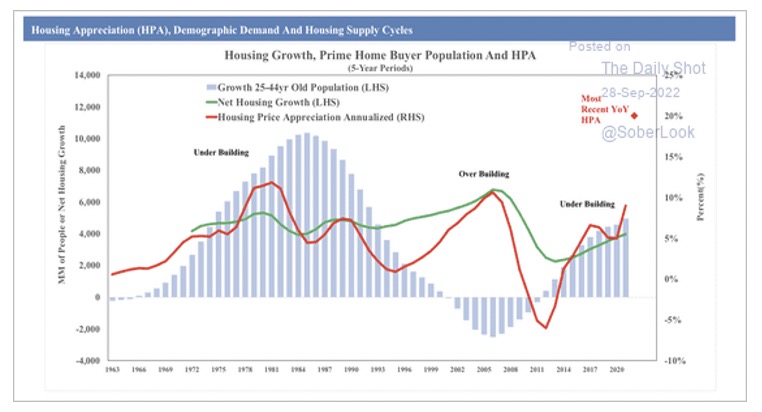

The ratio of home prices to disposable income is at a historically high level that has preceded previous declines in home values since 1963, especially during a recession. Although home prices weren’t high in 1969, the median home price fell -12.7% during the 1970 recession. Home prices went sideways from 1979 until 1983, as favorable demographics and high inflation supported home prices. (Demographic chart page 8) The recession in 2001 was shallow and the Federal Reserve lowered the Funds rate to 1.0% after 9-11, so home prices only fell modestly. In 2007 median home prices were down by -19.0%, but many cities that experienced rampant housing speculation plunged by -30% or more. Mortgage rates increased from 3.4% in September 2016 to 5.0% in November 2018 contributing to a -7.4% fall in 2017.

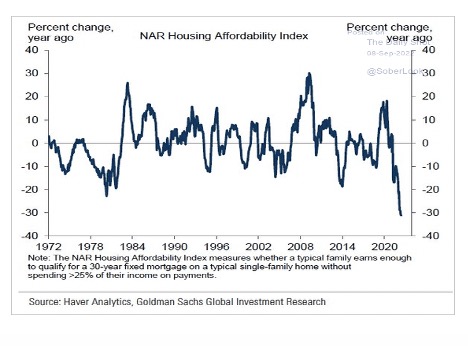

Mortgage rates have rocketed from 3.0% at the beginning of 2022 to 7.0% now. The combination of home price appreciation and mortgage rates has cause the National Association of Realtors Affordability Index to fall more than at any time in the last 50 years. Consider this. In 1980 the average 30-year conventional mortgage was 18.3%, but affordability wasn’t as bad as it is now. High home prices have priced out a significant number of Millennials who are ready to buy their first home, but simply can’t afford to.

The demographic surge between 1975 and 1984 in the 25-44 year old population supported home prices despite stratospheric mortgage rates. Home prices jumped from 2002 to 2006 because of low interest rates, extremely lax lending standards, and a wave of speculation that saw hair dressers and gardeners owning multiple homes without having to verify income i.e. liar loans. The demographics (25-44 year old) were actually negative so there was no pent up demand to slow the housing crash. Demographics turned positive in 2015 and the number of 25-44 year olds has continued to increase, which should provide support once mortgage rates come down a lot.

The annual increase in home prices will turn negative by the middle of next year and combined with the declines in stock prices and bond values will depress consumer spending and contribute to the recession in 2023.

Labor Market

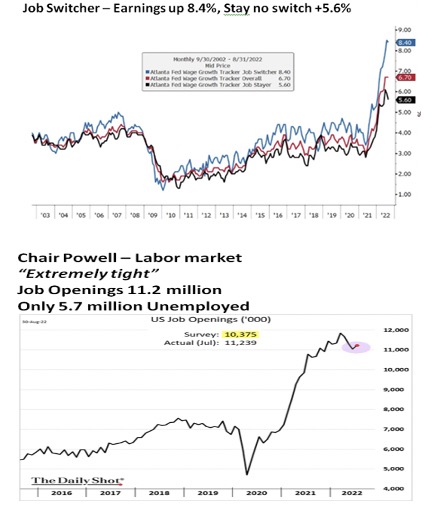

In the last six months Chair Powell has repeatedly talked about how tight the labor market is and he did again in his Jackson Hole speech. “The labor market is particularly strong, but it is clearly out of balance, with demand for workers substantially exceeding the supply of available workers.” There are many symptoms of just how tight the labor market is. According to the Atlanta Fed’s Wage Tracker, overall wages are up 6.7% in the last year, but job switchers experienced an increase of 8.6%. In July 2.7% of the 168 million workers in the US quit their job knowing they would be able to find another job easily and at a higher wage. This has been possible because there are about two open jobs for each unemployed worker. (11.2 million Open jobs vs. 5.7 million Unemployed). In 2018 there were about 7 million Open jobs, so the current level is more than 50% higher. In 2016 and 2017 there were less than 6 million openings, so the labor market began to tighten in 2017.

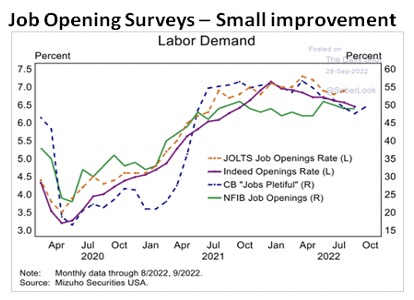

There has been modest improvement in recent months as the number of Job Openings has started to decline in 4 different surveys. The chart shows what the percentage change has been since February 2020 in job openings for each survey. The percentage has eased from a 55% increase at the beginning of 2022 to 50% in July. From Chair Powell’s perspective, the increase will need to fall back to where it was in February 2020 to provide a real reduction in labor market tightness.

The Conference Board’s Labor Differential quantifies the ratio of those who believe jobs are plentiful compared to those who think jobs are hard to get. This measure shows that labor market tightness began in 2017 and progressed right up to the onset of the Pandemic. In 2007 the Labor Differential plurality was less than 10% compared to 38% in February 2020 and 39% now. The National Federation of Small Businesses finds that 49% of small businesses are unable to fill open positions compared to 38% in 2019, and a peak of 34% in 2000 and 28% in 2007. Jobs became progressively more difficult to fill after 2016. Further evidence of how tight the labor market remains can be seen in the number of continuing Unemployment Claims, which have been holding near an all time record low.

The projections by the FOMC indicate that the Unemployment Rate will increase to 4.4% in 2023 and hold at 4.4% through 2024. The FOMC believes that if the ratio of Job Openings to Unemployed workers declines from 2 to 1 to 1 to 1, the Unemployment Rate won’t have to go up higher than 4.4% to create enough labor market slack to eliminate the upward pressure on wages. If employers can attract new employees without having to offer bonuses or higher wages, it will go a long way toward reestablishing balance in the labor market. The FOMC is likely to be wrong and will have to increase the projection for the Unemployment Rate, as the economy enters a recession in 2023, and for reasons discussed in the September Macro Tides.

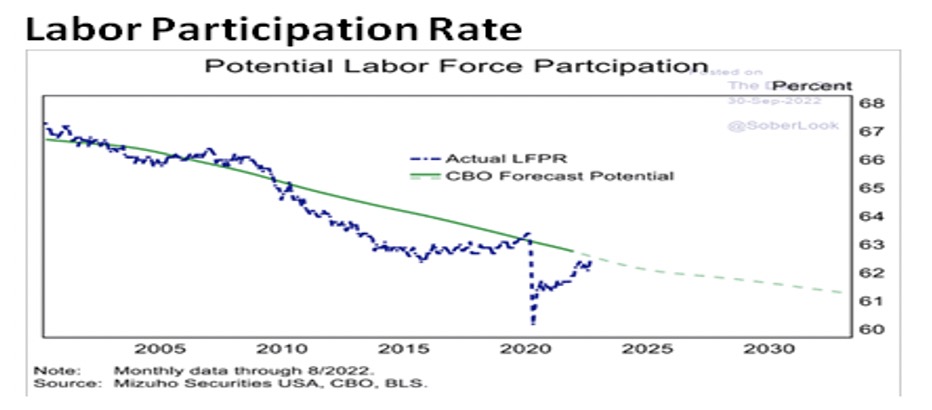

“The Overall Labor Participation Rate has dropped from 67.3% in 2001 to 62.4% in August, and down from 63.2% in February 2020 just as the Pandemic was taking hold. There are 168 million workers in the labor force so each 1.0% change in the Participation Rate represents 1.68 million workers.” The long term decline in the Labor Participation Rate since 2001 suggests that labor market tightness has become chronic, and the increase in tightness after 2016 in the charts above only magnified the problem. While a reduction in the ratio of Job Openings to Unemployed workers from 2 to 1 to 1 to 1 will definitely help, it won’t be enough to address the chronic shortage of workers.

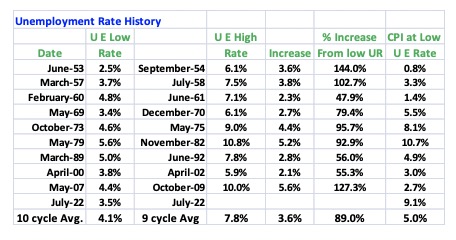

As discussed in detail in the September Macro Tides, the Unemployment Rate can be expected to increase to 5.0% or higher based on my analysis of prior cycles. “In the prior 9 cycles since 1953 (Excluding 2020 pandemic), the average increase in the Unemployment Rate (UR) was 3.6%, as the Federal Reserve increased interest rates to bring inflation down. The average percentage increase in the Unemployment Rate (UR) was 89% from the low in the UR. The smallest increase occurred between May 2000 and April 2002, when the UR only increased by 2.1%. The second smallest increase was in March 1989 when the UR increased 2.8% from the prior low. In May 2000 the CPI was 3.0%, or about 1/3 of the 9.1% CPI in June. The percentage increase in those two cycles was increases of 56.0% and 55.3%. If a similar percentage increase is applied to the 3.5% UR now, the Unemployment Rate would rise to 5.4%.”

There are a number of reasons why the Unemployment Rate will only increase slowly in coming months before a more rapid increase takes hold around after mid 2023. It will take months before the excess of Job Openings falls, as employers react to the slowdown in the economy and adjust their hiring plans. After experiencing the most difficult time in hiring qualified workers ever, many employers are going to resist letting existing employees go. They will wait until the recession begins to materially impact their revenues, before they cut hours worked and eventually lay off workers. To the extent that this process proceeds slowly, the upward pressure on wage increases will fade gradually, and not provide much immediate help in bringing overall inflation down.

Trade and GDP

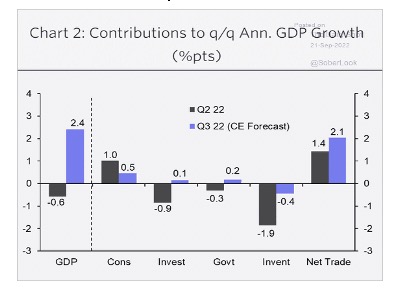

Gross Domestic Product measures domestic production which is why imports are subtracted. In the first quarter the US recorded its largest trade deficit in history. After subtracting imports GDP fell from +1.6% to -1.6%. In the second quarter the trade deficit narrowed from -$124 billion in March, so trade added +1.4% to GDP. Inventories were flat in the first quarter but subtracted -1.9% in Q2 as retailers dumped inventories and cancelled orders. After slashing inventories in the second quarter, inventory liquidation slowed in the third quarter, so the hit to GDP could shrink from -1.9% to -0.4% in Q3. In July the trade deficit was -$70 billion and will likely fall more during August and September (numbers aren’t available yet), so trade could add 2.1% to GDP in the third quarter. The contribution from trade and the smaller drag from inventory liquidation could enable GDP to be up +2.4% in the third quarter. Consumer spending accounts for almost 70% of GDP and in the third quarter it may be half as strong (0.5% versus 1.0%) in the third quarter compared to Q2. On the surface trade made the first quarter look weak when in fact the economy was in good shape. In the third quarter trade will make it look like growth rebounded, but trade will actually mask weaker consumer spending. If GDP does grow by more than +1.5% in Q3 (first estimate for Q3 released on October 27), it will cast significant doubt on whether the economy was already in a recession. The irony is that the economy is on the cusp of a recession irrespective of the illusion of strength due to trade in the third quarter.

Inflation Relief is Coming

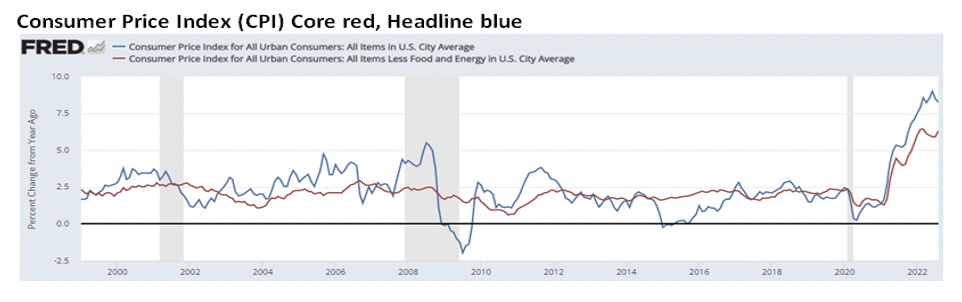

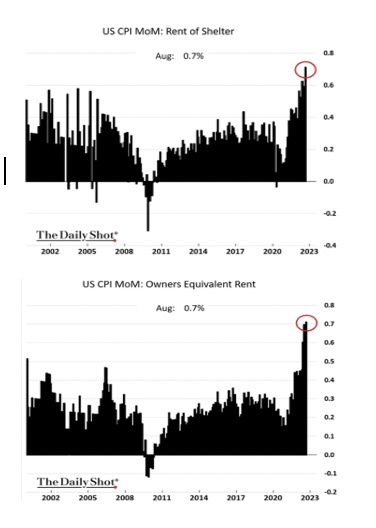

The financial markets were shaken when the August core Consumer Price Index (CPI) came in hotter than expected. Core inflation increased to 6.3% from 5.9% in July, and the monthly change jumped to 0.6% after holding at 0.3% in June and July. One of the largest factors was the 0.7% monthly increase in Rents and Owner’s Equivalent Rent (OER), which lifted the annual increase for Rents to 6.7% and 6.3% for OER. Apartment rents fell by 0.2% in September according to Apartment List, and the annual increase is down to 7.5% after peaking above 17.0% in January. When investors see that home prices and apartment rents are starting to fall, they assume that the decline will quickly show up in the Labor Department’s Shelter data. The methodology used by the Labor Department to calculate Rents and OER lags changes in home prices and rents by 12 months or more. In coming months the Shelter component in the CPI (Rents & OER) will continue to climb and offset some of the declines in other categories as it did in August.

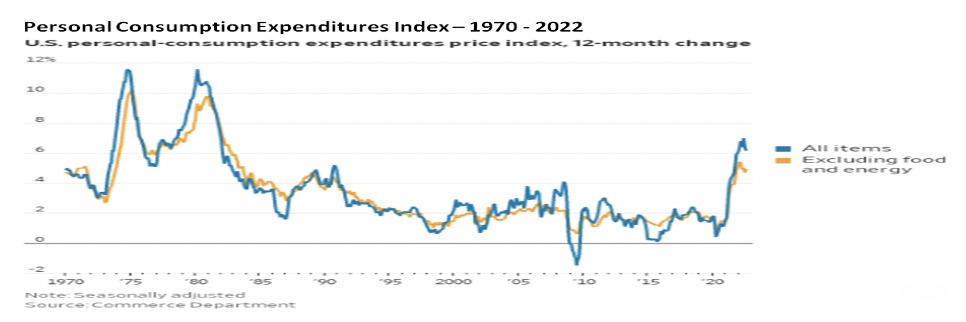

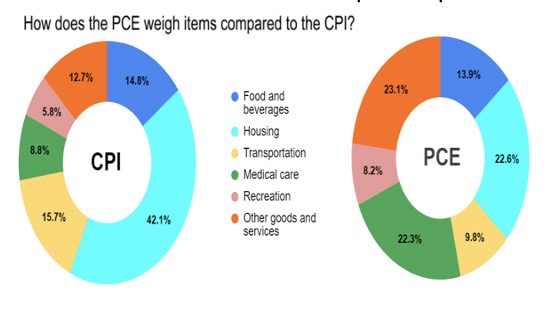

The Federal Reserve’s preferred inflation measure is the Personal Consumption Expenditures Index (PCE). In coming months the increase in Shelter inflation will be less in the PCE compared to the CPI, because the PCE allocates a much smaller weight to Shelter. When every cost associated with owning a home (insurance, utilities, etc) is included, Shelter represents 42.1% of the CPI, but only 22.8% of the PCE. In contrast, the PCE gives Medical Care a weight of 22.5% compared to 8.8% in the CPI.

In the August CPI the monthly increase in Medical Care was 0.77% due to a 1.31% increase in Dental Services, +0.78% for Hospital Services (wages), and a 2.4% increase in health insurance. The annualized increase for Medical Care was 5.65%. These increases are why the headline monthly PCE increased to 0.3% in August after a dip of -0.1% in July, and a jump to 0.6% in the Core PCE from 0.0% in July. The annual Core PCE rose to 4.9% from 4.7%, even as the headline PCE fell to 6.2% from 6.4% in July. Shelter in the CPI outweighs the PCE by 19.5%, but Medical Care in the PCE only outweighs the CPI by 13.5%. My expectation is that the core CPI may not fall as fast as the headline CPI due to Rents and OER, but the Core CPI may fall more than the Core PCE, as long as Medical Care costs don’t accelerate. The Shelter category in the CPI and Medical Care category in the PCE are the categories to pay attention to in coming months. Since the CPI comes out two weeks before the PCE each month, we’ll have an indication to whether Shelter is falling faster than Medical Care before the PCE is released.

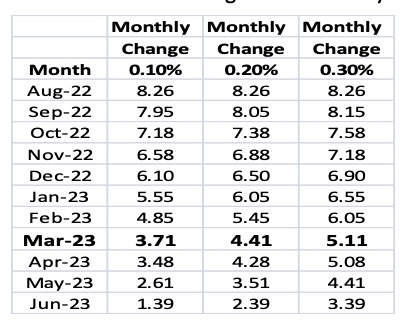

The CPI and the PCE indexes are largely a function of a 12 month rate of change. The monthly increase from September 2021 is subtracted from the annual increase, and the monthly change for September 2022 CPI is added. The math makes it possible to know how much will be subtracted from the CPI in the next 7 months with certainty. The take away value for the next 7 months (September-March) is -5.25%. The table estimates what level the headline CPI will be if the coming monthly increase is 0.1%, 0.2%, or 0.3%. If the monthly increase averages 0.2%, the November CPI would be 6.5% when it’s announced the day before the FOMC meets on December 14. The March 2022 CPI could be 4.41% when it’s announced in mid April.

As CPI inflation comes down many on Wall Street will jump to the conclusion that the FOMC will pivot and begin lowering interest rates. It will prove to be another example of Wall Street and investors failing to listen to the messaging from just about every FOMC member in recent weeks.

Federal Reserve

Chair Powell and the majority of FOMC members have said they expect to increase the Funds rate to a modestly restrictive level and then hold it at that level for a long time. The Dot Plot made this abundantly clear. Once the inflation data shows that inflation is trending lower, Wall Street will assume that the FOMC will relent. That seems unlikely. The coming decline in inflation will give the FOMC the cover it needs to stop hiking rates aggressively, but not pivot and lower rates. As discussed previously, the FOMC wants to avoid a recession if possible, the policy mistakes of the 1970’s, and to create enough slack in the labor market so that wage inflation doesn’t return early in the next expansion. In the 1970’s the Fed increased the Funds rate aggressively only to reverse when a recession developed. The FOMC doesn’t want to hike until they break something or crush demand as some have glibly suggested.

The Dot Plot indicates the FOMC will increase the Funds rate to 4.4% in December and 4.6% by next March. I don’t think the FOMC will be as aggressive as the Dot Plot suggests for a number of reasons.

Terminal Rate for the Federal Funds Rate

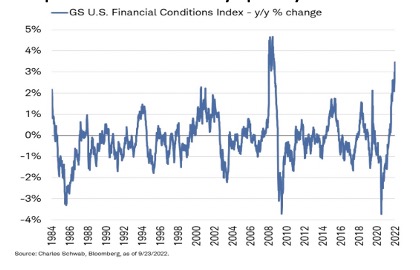

The FOMC uses changes in Financial Conditions to implement monetary policy. Financial Conditions have tightened significantly since mid August. Treasury yields have increased by almost 1.00%, the S&P 500 has fallen by -17.0%, the Dollar has jumped 7.1%, and the Bank of England was forced to intervene in the British bond market after yields soared by 1.20% in 4 trading days. The annual change in the Goldman Sachs’ Financial Conditions Index is the largest in 40 years, excluding the financial crisis in 2008. (Who wants a replay of that?)

The global economy will be weak in 2023 as many countries in the European Union and Great Britain experience a recession. China won’t have a recession since they fudge the numbers, but growth will be the weakest of the past 20 years in 2023. And many Emerging Market economies will struggle with higher food and energy inflation, weaker currencies, and higher interest rates.

In coming months more signs will emerge that the US economy is slowing as consumer spending weakens (irrespective of Q3 GDP) and inflation will ease, even if the labor market holds up for awhile. If correct, the FOMC will increase the Funds rate by 0.50% at the November 2 meeting, and not the 0.75% expected. Prior to that meeting FOMC members will continue to talk tough as they press the advantage generated by the DOT Plot in convincing Wall Street they mean business. The FOMC will push back hard on the notion that a slowdown in the economy and softer inflation will result in a quick pivot. Expect the FOMC to remind Wall Street of the need to keep growth subdued by holding the Funds rate at a restrictive level for the foreseeable future, so wage pressures subside. I think a recession is coming in 2023 and if it is mild, the FOMC will be able to resist the calls to pivot for a number of months if not longer.

Dot Plot Misses

The FOMC has a terrible track record when it comes to forecasting GDP, the Unemployment Rate, Core Inflation, and the Federal Funds rate. They fortified their track record in 2022 and in 2023 are likely to add to their reputation. The FOMC thinks GDP will grow by 1.2% in 2023 but a recession next year will make that projection too optimistic. The FOMC thinks the Unemployment Rate will only rise to 4.4% in 2023 and 2024, but it is likely to hit 5.0% or higher. The FOMC says the Funds rate will increase to 4.6% in 2023 and I suspect it will top between 3.75% and 4.25%. The FOMC says PCE inflation will drop to 2.3% in 2024. Inflation is set to come down in coming months but the longer term outlook could be problematic as discussed in the September Macro Tides. Wage inflation may prove stubborn due the decline in the Labor Participation Rate, oil prices may plateau at a higher level because supply is hindered due to the decline in exploration and investment since 2010, and the retreat in Globalization will lead to higher global production costs. At some point the FOMC will face a tough choice. Is it worth a deeper recession and much higher Unemployment to get inflation down to 2.3%, or do they declare victory and accept an inflation rate that’s closer to 3.0%?

S&P 500

Markets often retrace a percentage of a large advance which is why various retracement levels can be helpful in identifying a price ‘target’ for a decline. The S&P 500 rallied from a low of 2192 in March 2020 to 4818 in January 2022. The 38.2% Fibonacci retracement level of that 2,626 point move was 3815. With the FOMC hiking rates quickly to get to ‘neutral’, a decline in 3850 seemed likely in early April, as I noted in the April 4 Weekly Technical Review (WTR). The 50% retracement level is 3505 which is likely to be reached as the prospect of a recession leads to more selling. The 61.8% retracement level is 3195 that could be approached if a recession becomes a reality, and earnings are marked down to reflect it.

December 2021 Macro Tides - “The stock market could be vulnerable to a correction of -10% or more in the first quarter if markets expect the FOMC to move more aggressively in the first half of 2022.” The S&P 500 dropped from 4818 on January 4 to 4115 on February 24 a drop of -14.6%, and down -13.6% from December 31, 2021.

April 4 Weekly Technical Review - Investors were advised to lower equity exposure as the S&P 500 was trading near 4600. “From a risk reward and risk management perspective, raising cash as the S&P 500 trades near 4600 is a good idea. If this has been nothing but an impressive bear market rally, the S&P 500 will likely test 4115, or trade down to 3850 if 4115 doesn’t hold.” The S&P 500 dropped to 3850 on May 20.

September 19 Weekly Technical Review - A decline to the June low was expected after any bounce in response to Chair Powell comments after the September 21 FOMC meeting. “Unless Chair Powell throws the market a glimmer of hope, the FOMC projections and Dot Plot could hurt, as the FOMC lowers the estimate for GDP growth, increases its estimate for Unemployment and inflation, and indicates that the Fed Funds rate is going higher for longer.” The S&P 500 could rally to 4150 – 4200 in the next few weeks. Once this rally is complete, a decline to the June low of 3637 is expected.” The S&P 500 fell to 3584 on September 30.

The Daily Shot

Every month I include dozens of charts and the majority of them come from The Daily Shot. I highly recommend those who like charts of economic data to subscribe to The Daily shot.

Jim Welsh

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All