We have been wrestling with our forecasts intensely for the past several months. Some of our peers are projecting a recession for the United States, starting late this year. We aren’t ready to follow them, but the odds on a soft landing are getting longer.

At best, the next four to six quarters are likely to be sluggish. Our forecast of 0.6% full-year growth is far short of the 2% or more we would expect in a typical year. It may not be a recession, but such underperformance will feel like one.

An economy in a fragile state could be knocked into contraction by anything from a new COVID variant to a further energy shortage. Growing global stresses may prove contagious. In a steady world, there is a path for the economy to grow through the current challenges, but stability feels like an optimistic assumption.

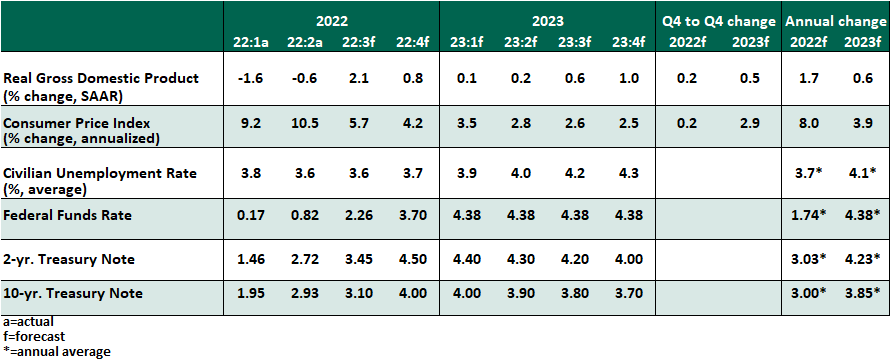

Key Economic Indicators

Influences on the Forecast

-

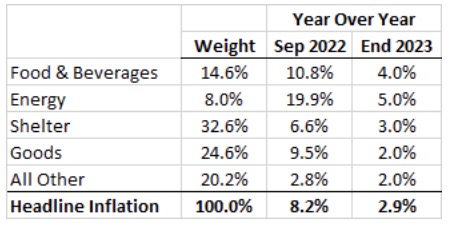

- Inflation remains the central point of concern. The September consumer price index (CPI) gained 8.2% over the past year. The details of the report showed modest relief in some categories of goods, but services inflation was far too high. Services as diverse as shelter, airfare and auto repair were notably hot; the 6.7% gain in core CPI was a 40-year high. Food prices are another persistent challenge.

- Lower energy prices have been a rare disinflationary bright spot in recent months, but the good news has come to an end. OPEC's decision to reduce production will keep upward pressure on the global price of oil. Domestic production remains scarred by recent losses. Gasoline prices are rising again.

- Inflation remains the central point of concern. The September consumer price index (CPI) gained 8.2% over the past year. The details of the report showed modest relief in some categories of goods, but services inflation was far too high. Services as diverse as shelter, airfare and auto repair were notably hot; the 6.7% gain in core CPI was a 40-year high. Food prices are another persistent challenge.