Too Much Confusion

There must be some kind of way outta here said the joker to the thief, there's too much confusion I can't get no relief…

Today’s investors are probably feeling a lot like the joker and the thief from Bob Dylan's classic “All Along the Watchtower”: caught in the highly confusing environment of a decelerating economy and rising rates, they can’t get no relief. This rare combination has resulted in a lack of good investment alternatives, as witnessed by the fact that in 2022, even U.S. Treasuries, which are considered risk-free securities and are generally in high demand when the stock market struggles, have produced double-digit losses. As of the end of the third quarter, the ICE BofA 10-Year Treasury Index is down 16.8% year-to-date! Likewise, the Bloomberg U.S. Aggregate Bond Index is down 15% and the S&P 500 is down 24%, marking the first time since 1969 that both equities and fixed income will be on track to deliver negative annual returns in the same year. It is a head spinning change from the salad days of 2020-21 when over $8 trillion of fiscal and monetary stimulus catalyzed untenably low interest rates as well as extraordinary demand for goods, thereby providing a sugar high for both corporate profits and asset valuations. Now investors must deal with the morning after, as spent up consumers, tight labor markets, and snarled supply chains send a myriad of mixed signals about the health of the economy.

These mixed signals lie at the center of the two big questions in financial markets today: 1) is the higher inflation transitory or structural, and 2) is the Fed capable of getting inflation under control without plunging the economy into a deep recession? With respect to transitory versus structural, we think the answer is “a little of both.” There are clearly disinflationary forces that should bring the overall rate of inflation lower. Most commodities are well off their highs – though we would point out that the oil-heavy Commodity Research Bureau Index is still 40% above its pre-Covid levels. We also see strong disinflationary forces in retail sales (thanks to inventory gluts), ocean shipping rates, lumber, used cars, and other categories. All of these markets are being affected by a combination of decreasing demand and increasing supply.

Conversely, we see considerable evidence of structural inflation in labor, housing, and energy. In our view, all three sectors are at risk of long-term supply problems. Labor suffers from low population growth, declining participation rates, an aging population, and anemic immigration, while at the same time reshoring is increasing demand for workers. With respect to housing, the same number of single-family homes were built in 2022 as in 1998, despite today’s first-time home buying cohort being larger than the gen-Xers of the late ‘90s. Finally, global crude production is at the same level as 2014, reducing slack in the system as demand slowly marches higher. Add in geopolitical volatility, and crude oil looks to remain tight.

It should be noted these structural supply constraints do NOT mean disinflation cannot happen. In fact, we believe disinflation is likely, especially in weak economic cycles. But we also think inflation will be lurking close to the surface during economic expansions. In our view, this is why the Fed is acting so aggressively. Powell’s Jackson Hole speech in August contained multiple references to the 1970s, even invoking the determination of Paul Volcker. Fed officials are clearly telling us that they do not want a repeat of the ‘70s when inflation came roaring back to higher highs on the heels of three consecutive economic expansions. To us, this explains the aggressive tightening and why the Fed is likely to stay tighter for longer.

The realization that the Fed is not kidding around this time and a dovish pivot is farther away than hoped has resulted in much hand wringing. Investors fear that the hangover we are feeling in financial markets is not just from the party last night, but possibly from the monetary party that has been going on since the Great Financial Crisis. At the very least, the worry goes, the Fed will create a hard landing for the economy, and in a worst-case scenario something breaks (e.g., pension funds in the U.K., Credit Suisse liquidity), creating this generation’s financial crisis. Risks are certainly elevated, and equity valuations are likely to go lower, ergo prudence would suggest investors should have higher cash levels. However, we cannot ignore the idea that if the deeper fears are realized, this will perhaps be the most anticipated recession and financial crisis ever, making us wonder how much of the bad news is already priced into the stock market.

To us the bull case from here lies in the idea that flush balance sheets, economic momentum, and the incremental demand from reshoring, infrastructure, and alternative energy may be just enough to carry the economy to the other side. In this scenario, the U.S. slowly becomes accustomed to both modestly higher rates and inflation, resembling the late 1990s economy when the yield on the 10-year Treasury bounced between 5% and 7%. We think this kind of world argues for lower valuation ceilings and a greater reliance on dividend income to drive returns for individual investors.

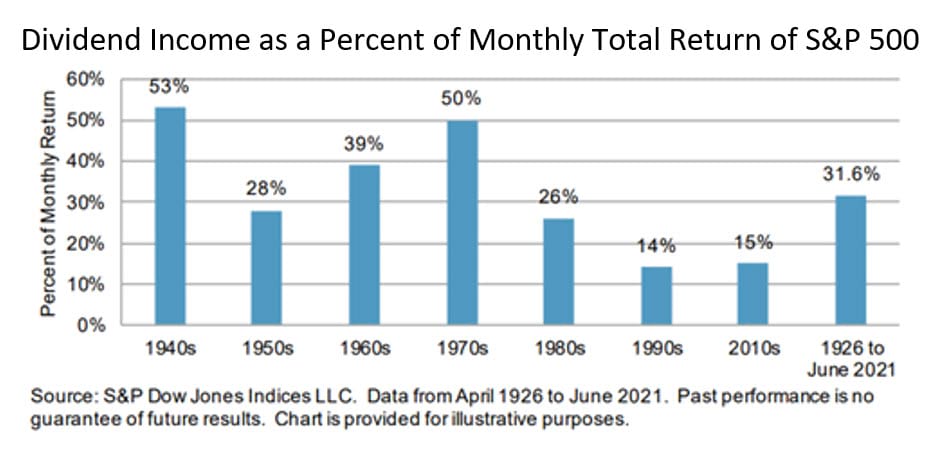

Historically, dividends have played an important role in overall investor return. This is especially true in higher interest rate environments. In fact, a recent study from S&P Global demonstrates that 32% of investor returns in the S&P 500 were generated by dividends from 1926 through June 2021. In some periods, when markets swoon, dividends account for 50% or more of overall S&P 500 returns, as was the case in the 1940s and 1970s.

Our own view on dividends places a high emphasis on dividend growth, which is only achievable through growth in underlying cash flow per share. Companies that can sustainably grow their dividends tend to be those that benefit from secular industry tailwinds, pricing power, and/or recurring demand growth. These are exactly the types of businesses we have always sought to invest in, particularly when we catch them at an attractive valuation and/or an inflection point.

By selecting companies that have long histories of both paying dividends and growing them annually, we seek to capture the best of both “value” and “growth” investing. These companies tend to have sustainable and enduring growth and generate cash flow in excess of their reinvestment opportunities. Over time, this combination can be extraordinarily powerful and significantly benefit our portfolios. Companies with these characteristics populate nearly every industry.

Perhaps the most compelling attribute of companies with long histories of growing dividends is the fact that these businesses tend to exhibit attractive returns with less volatility over time. In fact, from January 1990 to June 2021, a basket of companies, known as the S&P Dividend Aristocrats1, which have the longest sustained histories of dividend growth, both outperformed the broader S&P 500 index and experienced less price volatility, resulting in a higher Sharpe ratio for the dividend paying basket. Specifically, the dividend paying basket outperformed significantly during drawdowns while performing roughly in line with the market during periods of broad advances in equities. This lower volatility and outperformance is not a coincidence — we believe it results directly from the better underlying business performance and better balance sheets characterizing these companies.

As always, we continue to seek investment opportunities in great or improving businesses at attractive valuations and inflection points. Emphasizing companies that pay growing dividends and have a long history of doing so is just another aspect of that approach, and we view the current market environment as ripe with opportunities in this area.

Eventually, the fog looming over the economy will recede, and clarity will prevail – we will find our way “outta” here. When that happens, markets will recover, likely in roaring fashion, as has always been the case after similar periods of uncertainty. Thus, it is critically important to remain invested in equities, as we believe the overall global economy will continue growing once inflation dies down and rates flatten and potentially decline. However, selecting the right equities is critical, and we remain committed to owning attractively valued businesses that exhibit durable and often accelerating growth backed by sound balance sheets.

Please reach out if you have any questions. We genuinely appreciate the trust you have placed in us, and we look forward to serving you for many years to come.

1The Dividend Aristocrat Index is a subset of the S&P 500 that is made up of companies that have increased their dividend every year for at least 25 consecutive years.

John Osterweis

Founder, Chairman & Co-Chief Investment Officer – Core Equity

Larry Cordisco

Co-Chief Investment Officer – Core Equity & Portfolio Manager

The Osterweis Funds are available by prospectus only. The Funds’ investment objectives, risks, charges and expenses must be considered carefully before investing. The summary and statutory prospectuses contain this and other important information about the Funds. You may obtain a summary or statutory prospectus by calling toll free at (866) 236-0050, or by visiting www.osterweis.com/statpro. Please read the prospectus carefully before investing to ensure the Fund is appropriate for your goals and risk tolerance.

Mutual fund investing involves risk. Principal loss is possible.

Index performance is not indicative of fund performance. To obtain fund performance, click here.

Past performance does not guarantee future results. This commentary contains the current opinions of the author as of the date above, which are subject to change at any time. This commentary has been distributed for informational purposes only and is not a recommendation or offer of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable but is not guaranteed.

There is no guarantee that a company will pay or continue to increase dividends.

No part of this article may be reproduced in any form, or referred to in any other publication, without the express written permission of Osterweis Capital Management.

Holdings and sector allocations may change at any time due to ongoing portfolio management. References to specific investments should not be construed as a recommendation to buy or sell the securities by the Osterweis Fund or Osterweis Capital Management.

The chart “Dividend Income as a Percent of Monthly Total Return of S&P 500” has been reprinted with permission from Standard & Poor’s and may not be redistributed without their prior authorization.

The Bloomberg U.S. Aggregate Bond Index is widely regarded as the standard for measuring U.S. investment grade bond market performance.

The S&P 500 Index is an unmanaged index that is widely regarded as the standard for measuring large-cap U.S. stock market performance.

ICE BofA Current 10-Year U.S. Treasury Index is a one-security index comprised of the most recently issued 10-year U.S. Treasury note. The index is rebalanced monthly.

The Commodity Research Bureau Index measures the aggregated price direction of various commodity sectors, and is designed to isolate and reveal the directional movement of prices in overall commodity trades.

Source for any Bloomberg index is Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg owns all proprietary rights in the Bloomberg Indices. Bloomberg does not approve or endorse this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

Effective 6/30/22, the ICE index reflects transactions costs. Any ICE index data referenced herein is the property of ICE Data Indices, LLC, its affiliates (“ICE Data”) and/or its Third Party Suppliers and has been licensed for use by OCM. ICE Data and its Third Party Suppliers accept no liability in connection with its use. See www.osterweis.com/glossary for a full copy of the Disclaimer.

These indices do not incur expenses (unless otherwise noted) and are not available for investment.

Treasuries (including bonds, notes, and bills) are securities sold by the federal government to consumers and investors to fund its operations. They are all backed by “the full faith and credit of the United States government” and thus are considered free of default risk.

Cash flow measures the cash generating capability of a company by adding non-cash charges (e.g., depreciation) and interest expense to pretax income.

Free cash flow represents the cash that a company is able to generate after laying out the money required to maintain and expand the company’s asset base. Free cash flow is important because it allows a company to pursue opportunities that enhance shareholder value.

The Sharpe Ratio represents the added value over the risk-free rate per unit of volatility risk.

Osterweis Capital Management is the adviser to the Osterweis Funds, which are distributed by Quasar Distributors, LLC. [OSTE-20221018-0642]

© Osterweis Capital Management

Read more commentaries by Osterweis Capital Management