The age-old adage, “prevention is better than cure,” remains a valuable guide to decision making. But the pandemic has forced us to ask: how much does prevention cost? This is an especially important question as China continues its fight against the COVID-19 virus.

Chinese policymakers have stubbornly persisted with a zero-COVID strategy that focuses on containment of the virus. The stringent approach was the best prevention tool in the earlier lethal waves of the pandemic, but both mortality and infection rates have fallen across the globe. As a result, the world has chosen to live with the virus. However, China is the last major nation that continues to rely on lockdowns, mass testing, contact-tracing and quarantines to prevent the virus from spreading. The low efficacy of China’s domestically-produced vaccines have contributed to this orientation.

In a tacit acknowledgment that the costs of containment measures are now outweighing the benefits, Chinese authorities relaxed some restrictions last week, even as infections climbed to their highest levels in months. Quarantine requirements were eased for close contacts and international travelers from seven to five days, while maintaining three further days of home isolation.

The move spurred a rally in financial and commodity markets. Hong Kong’s Hang Seng Index rose 12% in just a week, and the mainland’s benchmark Shanghai Composite Index improved by about 3% over the same time period. Commodities from oil to soybeans to precious metals rebounded on hopes of a demand recovery in the world’s second-biggest economy. Though a welcome development for investors, Beijing’s move has also re-ignited inflation fears in some quarters.

We think that this reaction is substantially overdone. Beijing has only watered down strict COVID rules, not waived them entirely. Millions of people are still under lockdown in the western and southern parts of China. Lockdowns, and the economic impairment they cause, will continue to hold consumers and the economy back, as opposed to firing up demand for commodities and tourism-related services. Though eased somewhat, travel rules remain onerous, with inbound and outbound group tours suspended.

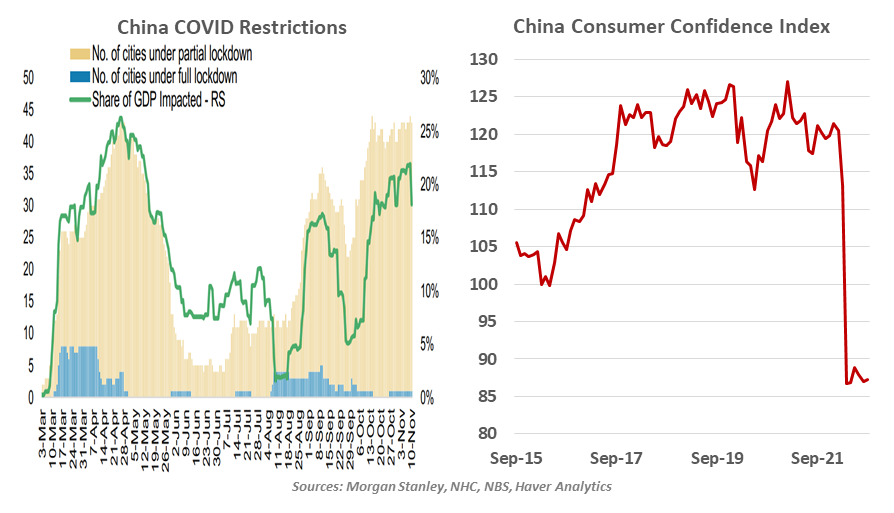

China’s lockdown strategy has not only struggled against highly transmissible variants, but it has also taken a heavy economic and social toll. The strategy continues to disrupt manufacturing and is weighing on consumer confidence. Both have been a major drag on economic growth. Zero-COVID is set to cost China $384 billion in lost gross domestic product this year.

|

China is still far from open for business as usual.

|

Beijing’s plans to boost the economy have often relied on big investments by local governments. However, the finances of heavily indebted local governments are also under stress from plunging land sale revenues. This was partly due to lockdowns, which dented households’ incomes and their willingness to invest in real estate.

Lockdowns in China have added to ongoing supply chain disruptions at home and abroad, weighing on global growth and adding to inflationary pressures. An unrestricted reopening will ensure a steady flow of goods, thereby reducing the supply-demand imbalances. Conversations about “reshoring” are growing in volume around the world, partly because Chinese supplies are seen as less reliable. Relaxing COVID restrictions could help allay those concerns.

The limited set of easing measures announced by China provides some hope. But the withdrawal of quarantine requirements is what will mark the end of the zero-COVID policy, nothing less. In our view, zero-COVID is no longer a policy that serves the best interests of China or the world.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2022 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

© Northern Trust

Read more commentaries by Northern Trust