The pandemic prompted a government spending spree on a scale rarely seen outside of wartime. Unfortunately, stimulus programs created demand that outstripped supply, contributing to today’s inflationary excesses. Rising interest rates have resulted, making it more difficult to service new peaks of national debt.

For these reasons, fiscal policy is now in retreat. The exact pace and design of achieving this end varies considerably across countries, but the direction is clear. One interesting case study in the series will come from Europe, which has approached debt and deficits more formulaically. It will be interesting to see if the European Union (EU) can solve this difficult equation.

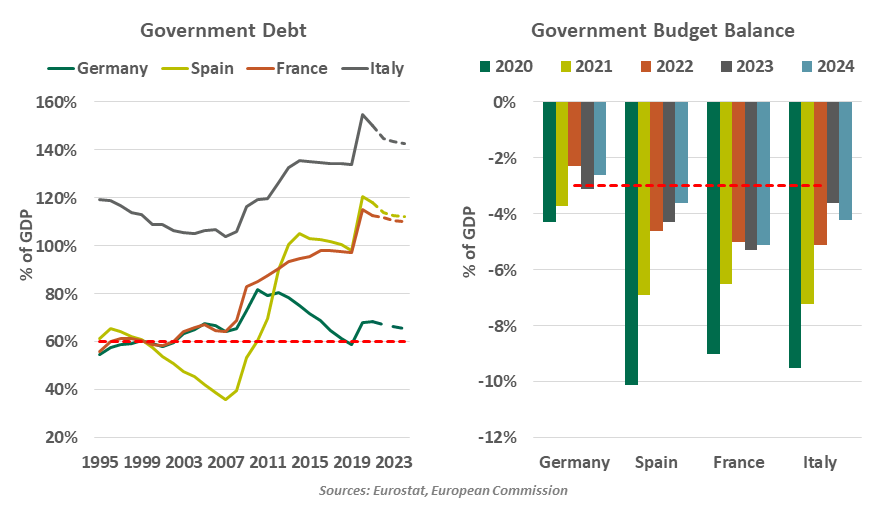

The European Commission (EC) is seeking to restore and reform its long-standing fiscal rules. The Maastricht Treaty of 1992, which laid the foundation for the euro, requires member states to keep their public deficits below 3% of gross domestic product (GDP) and their debt below 60% of GDP. These standards were intended to enforce budgetary discipline and avoid the debasement of the common currency.

Violation of the deficit or debt criteria and failure to initiate corrective measures will trigger the excessive deficit procedure (EDP). The EDP entails steps ranging from a fine of up to 0.5% of GDP to suspension of commitments or disbursements from EU programs. A nation whose debt or deficit is above the targets is still considered compliant if it is making progress toward reducing excess debt by at least 5% of GDP each year and its deficit by 0.5% of GDP per year.

But a rule without enforcement is hardly a rule at all. Almost all of the bloc’s economies have breached the thresholds at one point or another. Yet no EU member state has ever been fined, including those which had ended up in an EDP. Germany and France both breached the 3% deficit limit almost two decades ago but never faced the threat of penalties. Portugal and Greece were threatened but never penalized.

The patchwork of rules and exceptions has made the EU’s current framework the world’s most complex rules-based fiscal policy; its handbook runs over 100 pages. Supporters assert that the framework has helped to facilitate economic growth and financial stability in Europe. Critics point out that the pact failed to prevent the debt crisis experienced by the continent in the last decade, and the strict rules have limited public investment by many member states. The austerity required of violators has often been painful, and has contributed to the rise of nationalist and populist forces.

|

The current European fiscal framework has not been rigidly enforced.

|

Europe’s fiscal rules have been suspended since the onset of the pandemic and will remain so until the end of next year. But the debate over how to reinstate the framework is heating up now. With so many countries so far above the old ceilings, retaining the same limits would require amounts of austerity that would be exceptionally severe. Further, Europe is on the brink of a recession, and has committed to providing needed relief for high energy costs.

Recognizing this, the EC has proposed a new, more flexible approach that focuses on improving public finances in a simple and gradual manner. The core objectives remain the same: ensuring debts and deficit levels remain sustainable. The break in the rules offers a natural opportunity to make these objectives more feasible.

The Commission seeks to scrap the existing debt and deficit reduction rules. Going forward, nations will be allowed to establish fiscal trajectories over a four year period, instead of adhering to an annual target. When accompanied by pro-growth structural reforms and investments, the projection can be extended to seven years. This implies that governments with different starting points will have dissimilar paths of adjustment. Highly indebted countries will benefit from the additional time to shore up their finances without resorting to severe and abrupt cuts.

This approach sounds sensible on the surface, but what it adds in flexibility introduces immense amounts of subjectivity. What, exactly, will qualify as pro-growth reforms and investments? How will these be scored, and who will be the scorekeepers? Countries subject to fiscal adjustments have a nasty habit of back-loading discipline, which leaves plans vulnerable to last-minute disappointment; Europe has some serial violators on this front. And lenience provided to some borrowers could generate antipathy among countries who adhere more closely to stated standards.

The EDP would still be maintained and activated when a member state with debt above 60% of GDP deviates from the agreed expenditure path. Non-compliant nations would lose access to EU financing if they fail to correct fiscal imbalances. Breaking reform and investment pledges will result in a more restrictive adjustment path and, for eurozone nations, the imposition of financial sanctions. That said, the penalty for violators would be lowered to only 0.1% of GDP, which may not be a sufficient deterrent.

|

Europe needs higher investments, which will only possible with an overhaul of its fiscal rules.

|

Though the proposal is the outcome of long negotiations and public consultation, it is uncertain whether it will secure the backing of all EU countries. The measures are likely to see support of free-spending countries like France and Italy, as the existing rules are more focused on fiscal discipline than growth. It stands at odds with the objectives of more frugal economies like Germany and the Netherlands, who are against uncontrolled spending.

The EC’s proposal is a step in the right direction. But the EU needs greater fiscal coordination and investments to fight the varied challenges of an energy crisis, a war in close proximity, a technological rivalry with China, a fight against climate change and income inequality. Joint debt issuance is one answer and was used during the pandemic, but is not favored by all member states as a lasting or long-term solution.

The window for reaching a compromise is short: the EC will assess medium-term budgetary plans in March 2023. Regaining sobriety after a binge is never easy, but delaying the transition can risk an even larger hangover.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2022 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

© Northern Trust

Read more commentaries by Northern Trust