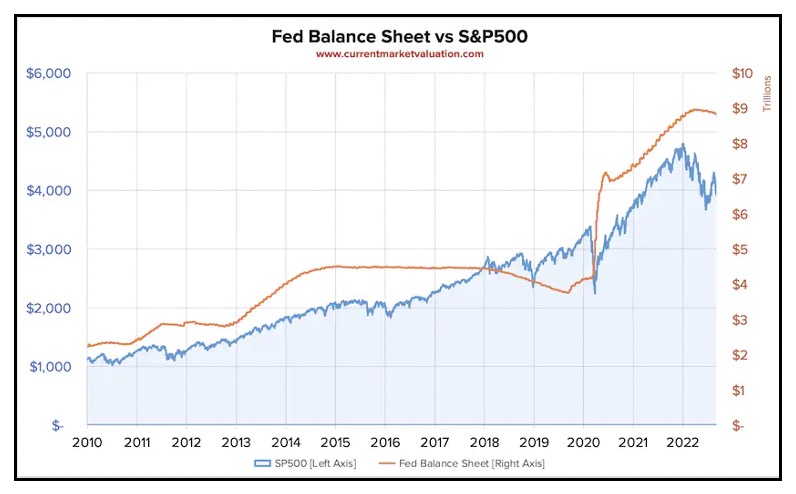

After years of easy money policy from the Federal Reserve and a years long bull market that set record after record, the era of double-digit equity returns seems to be coming to a close. The chart below shows how correlated increases in the Fed’s balance sheet have been with equity performance over the last couple years.

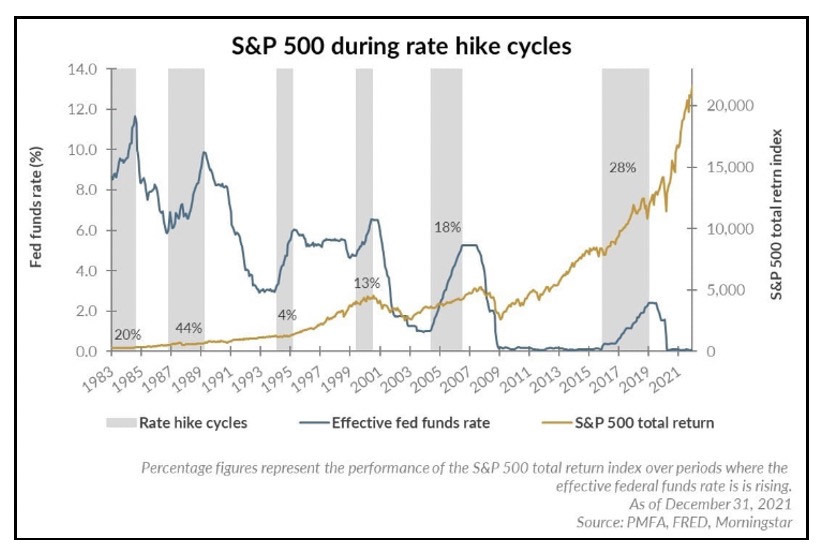

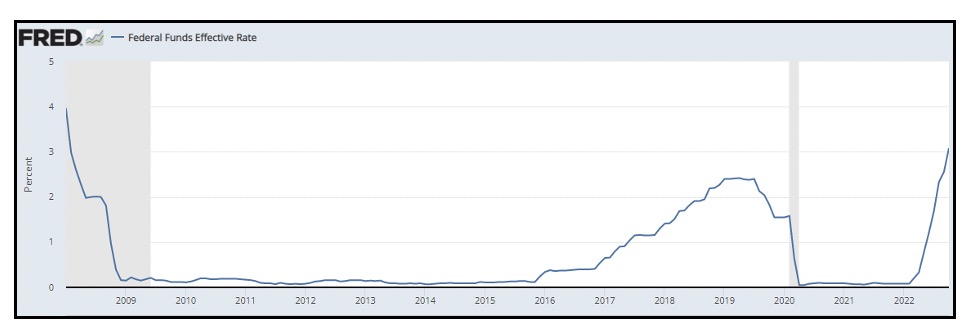

The next two charts paint an even more glaring picture. We have enjoyed many years of historically low interest rates, and during that time the equity markets experienced truly explosive performance. The effective Federal Funds rate dropped below 1% near the end of 2008 and didn’t make it back above 1% until the middle of 2017. Between the start of 2009 and end of May 2017, the S&P 500 appreciated over 160%. After the short and violent drop driven by the onset of Covid in Q1 2020, the Fed stomped on the gas pedal and began rapidly expanding their balance sheet, driving the S&P up nearly 100% above May 2017 levels. When we came into 2022, the S&P was up over 400% from early 2009.

The Return of the Sleeping Bear

This year has brought the market down from the clouds and should drive sidelined investors who had been waiting for a dip to buy back into the game. Long-term investors know they need to maintain equity exposure and know too that most market dips, like the one we are currently experiencing, look like buying opportunities when viewed 10 years after the fact. Of course, it can be particularly difficult to buy into a troubled market when you’ve been sitting on the sidelines waiting for a chance to get in. Not to mention how tough it can be to throw more money into equities when you’ve seen your portfolio shrink by roughly 20% this year. While there is no doubt the market could potentially head lower still before it starts a long-term recovery, there are ways to start increasing equity exposure while buffering against potential downside.

Why Stocks and Bonds are in Lockstep

Traditionally, investors could reduce the volatility of a portion of their assets by parking capital in fixed income. The idea is that having part of their portfolio in bonds, an investor can buffer against the potential downside of equities. However, inflation, rising rates, and slowing growth are causing stocks and bonds to move in the same direction. This has not happened in decades and has forced investors to look elsewhere for reduced downside risk.

Volatility, A Hawkish Fed, and Covered Calls

Consider all this in the context of resurgent volatility by looking at the Chicago Board Options Exchange’s CBOE Volatility Index (VIX), a popular measure of the stock market’s expectation of volatility based on S&P 500 index options. From 2012 through 2019, the VIX averaged just over 15. So far this year, it has averaged over 26. This elevated volatility translates to higher option prices in general, and a wider distribution of premium across strike prices.

The current environment is an attractive one for a covered call strategy. A covered call strategy is when an investor owns 100 shares of stock and writes a call against those shares with a specific expiration date and strike price. In doing so the investor is essentially selling away the upside beyond the strike price in exchange for being paid a premium. If the stock stays below the strike price through the expiration of the call, the investor keeps that premium and has the opportunity to sell another call. The amount of premium and upside potential the investor has depends on the specific call they sold, but higher levels of volatility should allow for more of both if all else held equal.

Bottom Line

Buying into equities and writing covered calls against them in this challenging investing environment allows an investor to get paid for the market’s volatility, adds a slight downside buffer in case the market continues to slide, and with volatility at current levels you can still retain substantial upside potential in case the market sees a bounce. In general, a covered call strategy is expected to underperform the market when you have years with the S&P up 25%+ and volatility is low, but with volatility back and a more hawkish Fed we find ourselves in a far different scenario. Therefore, as we head into an uncertain new year, covered calls can offer sophisticated investors and advisors a strategy that can potentially provide growth, income, and risk mitigation.

Nick Griebenow, CFA, is a Portfolio Manager for Shelton Capital Management’s Option Overlay Strategies.

Important Information

Options involve risk and are not suitable for everyone. Prior to buying or selling an option, your client must receive a copy of CHARACTERISTICS AND RISKS OF STANDARDIZED OPTIONS. Copies of this document may be obtained from your Investment Advisor, from any exchange on which options are traded, or by contacting The Options Clearing Corporation, One North Wacker Dr., Suite 500, Chicago, IL 60606 (1-800-678-4667).

Any strategies discussed, including examples using actual securities’ price data, are strictly for illustrative and educational purposes only and are not to be construed as an endorsement or recommendation to buy or sell securities. You and your client should review transaction costs, margin requirements and tax considerations with a tax advisor before entering into any options strategy.

Sources

Chart 1: https://www.currentmarketvaluation.com/posts/fed-balance-sheet-vs-sp500.php (Sept 14, 2022)

Chart 2: https://topforeignstocks.com/2022/01/26/performance-of-sp-500-index-when-interest-rate-rises-chart/?utm_source=rss&utm_medium=rss&utm_campaign=performance-of-sp-500-index-when-interest-rate-rises-chart (Jan 26, 2022)

Chart 3: https://fred.stlouisfed.org/series/FEDFUNDS (Nov 29, 2022)

Historical VIX data: https://www.cboe.com/tradable_products/vix/vix_historical_data/ (Nov 29, 2022)

© Shelton Capital Management

Read more commentaries by Shelton Capital Management