December is a natural time to look back and see how the year compared with our expectations. But a year like 2022 can throw off even the best forecasters.

We came into the year expecting the Fed to end asset purchases and raise rates; we did not anticipate such an aggressive pace of hikes. We expected inflation to calm; it is only healing now, after a painful surge through much of the year. We certainly did not expect the Russia-Ukraine war and the ensuing distortion to energy and food markets that drove so much uncertainty this year.

While it is incumbent on us to expect the unexpected and plan for worst-case scenarios, we should all take some pride in the resiliency seen throughout the economy in recent years. In the face of high inflation, ongoing health concerns and lingering supply shortages, businesses kept hiring and consumers kept spending. That resilience gives us hope that the economy can escape contraction in the year ahead: growth will be slower, but falling inflation and steady employment can keep us out of contraction.

Key Economic Indicators

Influences on the Forecast

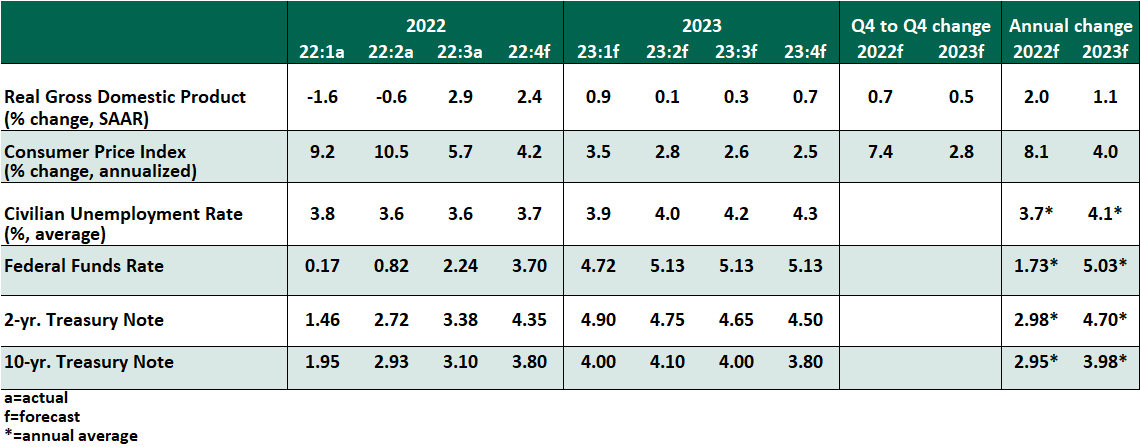

- The November reading of the consumer price index (CPI) offered a second consecutive month of cooling inflation. The index rose by 7.1% over the past year; core inflation, excluding the volatile energy and food components, fell to a 6.0% gain. Shelter – both rent of residences and owners’ equivalent rent – continued to add to overall inflation, and will take several more months to reflect the cooling of the housing market.

Aside from food and shelter, most categories showed a deceleration or deflation of prices. The Fed has emphasized a need to see sustained progress toward lower inflation before rate cuts will be considered; while the index has a great deal of ground to recover, the journey has begun.

- Early evidence of softer inflation has not softened the Federal Reserve’s resolve to fight it. The Federal Open Market Committee (FOMC) unanimously raised the Fed Funds Rate by 50 basis points to a range of 4.25-4.50% at its December meeting. The quarterly Summary of Economic Projections showed a median expectation of 75 more basis points to come next year, and no reductions until 2024. Despite an outlook of higher unemployment and risk of a recession, no FOMC members are yet ready to signal a pivot. On this basis, we have revised our Fed forecast to include 75 basis points of hikes in the first quarter, then a pause.

- The Employment Situation Summary for November showed yet another month of job creation, with 263,000 jobs added and the unemployment rate holding at 3.7%. However, the underlying data was not entirely encouraging. The household survey indicates two months of net job losses, and labor force participation rates remain below their pandemic levels. Average hourly earnings grew 5.1%, an unwelcome acceleration following seven months of gradual decline.

- Debates about the recession outlook are ongoing, but in the U.S., they are entirely in the future tense. High-frequency readings of consumer spending and business investment are still showing growth, and the current risk of a downturn is low. We have revised up our outlook for fourth quarter growth. Looking to the year ahead, the window to a soft landing remains open, but it will be a close call.

- Consumer spending has kept the U.S. economy afloat, but household budgets are stretched. Bank deposits have declined by $500 billion from their April peak, reflecting a shrinking savings cushion. As of October, the U.S. personal saving rate fell to a 15-year low of 2.3%, and consumer credit card balances show steady growth. Credit bureau statistics show only a modest increase of delinquencies thus far, following an abnormally low rate of late payments due to pandemic stimulus.

- When discussing next steps, Federal Reserve officials often refer to “financial conditions,” a broad measure of the availability of funding in an economy. This umbrella term incorporates equity market returns, interest rates, credit spreads, and foreign exchange conditions. This volatile year is concluding with easier conditions, especially in fixed income markets. Though supportive for market participants, any asset rally complicates the Fed’s objective of a managed deflationary slowdown.

© Northern Trust

Read more commentaries by Northern Trust