Much has been written about the ever-changing labor force in the last year. What started as a social and professional experiment in remote work out of necessity due to the pandemic morphed into a panoply of perspectives on the future of work. (Spoiler alert: We still need it.) One such narrative paints employers as always looking for ways to take advantage of workers in what might be called “task creep,” or being expected to take on tasks that are outside of the scope of their stated roles. What might have once been a way to get a leg up and impress at the office has become, in some circles, a rallying cry for employees to say no to special projects without appropriate compensation or recognition (potential career advancement notwithstanding). In response, employers have branded such employees who are not willingly “doing whatever it takes” as instead “doing the bare minimum.” Taking this one step further, some managers are engaging in behavior that in the past might have been labeled “constructive dismissal,” a problematic action defined in employment law, but is now being branded as “quiet firing,” much to the delight of poets and wordsmiths everywhere. While this growing antagonism seems perfectly on-brand for today’s society as a whole, we don’t see how it helps the very real economic challenge presented by today’s evolving workforce.

Full Employment: The Fed’s Frenemy

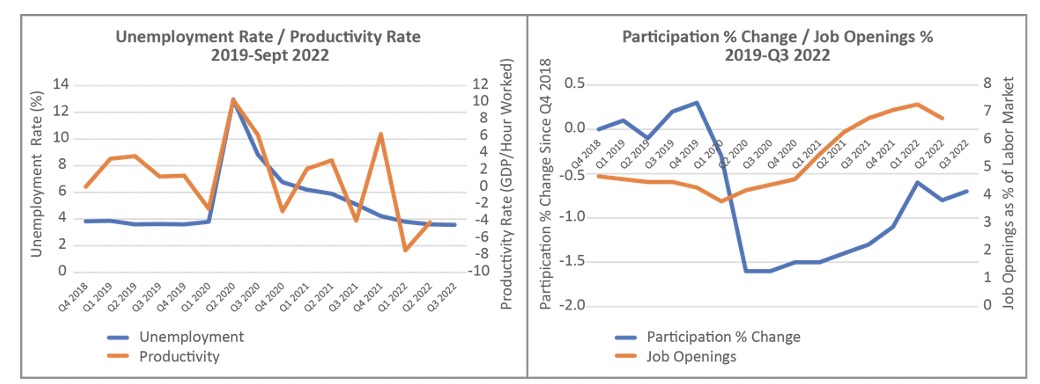

As part of their efforts to predict when the current economic cycle might turn, many economists have cited a variety of workforce metrics, from unemployment rate and productivity to labor force participation and job openings. If we look at these data points since the start of 2019 (Figure 1), we can provide context for much of the analysis we have been reading and hearing.

Of course, the most obvious statistic is the unemployment rate. With the Fed's focus on reducing consumer demand to fight inflation, stubbornly tight labor markets pose a challenge. After all, the lower the unemployment rate, the more people there are who have income to spend. Some have even cast the Fed's battle with inflation and demand as an implicit war on employment, where they must intentionally cause some material number of job losses if they are to tame price increases and succeed in reaching their 2% inflation target.[1] As we can see from the charts in Figure 1, the unemployment rate has returned to lows seen prior to the pandemic. Put another way, the Fed has some support for aggressive tactics to lower inflation, and if the cost is slightly higher unemployment, the economy can withstand an increase from currently low levels.

Figure 1: Historically tight labor markets might be interpreted as suggesting the Fed can remain aggressive with inflation while still keeping an eye on its full employment mandate. (Source: Bloomberg Finance, LP)

Perhaps the current economic cycle can give way to the next one relatively soon and with only the slightest recession while still maintaining sufficiently tight labor markets to satisfy the Fed's full employment mandate. Productivity data, overlayed on the unemployment chart in Figure 1, supports this argument. There is a law of diminishing returns associated with lower unemployment, where at some point, the productivity (defined as domestic GDP output per hour worked) decreases, making each employed person less impactful on economic output. Meanwhile, as we can also see in Figure 1, there is more room to go for labor force participation to return to pre-pandemic levels, and job openings are still elevated.

Once again, the support is there for the Fed to remain aggressive on inflation. One can see both the case for further Fed rate hikes and a potential light at the end of the tunnel: Higher unemployment, fewer job openings, and more normalized levels of participation and productivity could provide a clear roadmap for when the Fed and the markets might believe inflation is under control. As a result, the majority of the analysis we have encountered focuses on whether the Fed will cause a recession and, if so (which seems to be the general consensus), how deep it will go before they get the data points they need to see to relax their hawkish monetary policy. There is some disagreement on how long this cycle will take to play out, with some arguing for several months while others think several quarters.

Ladies and Gentlemen, the Boomers Have Left the (Office) Building

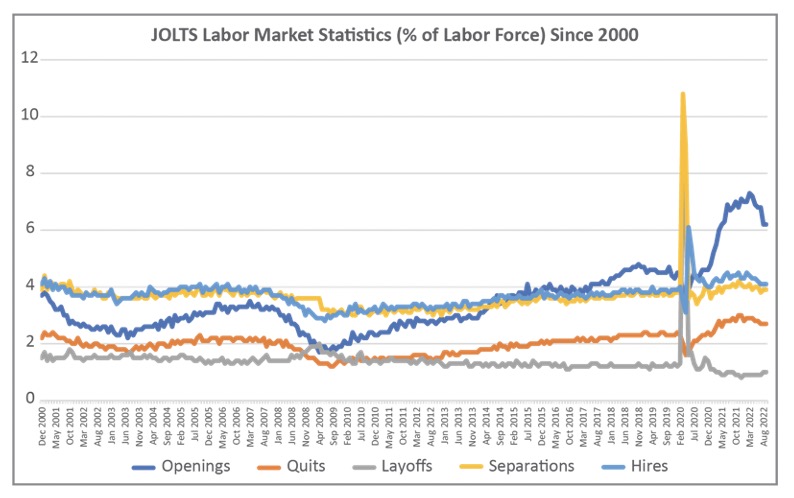

Not so fast. In our view, looking at the data over a more expanded timeframe and in more granular depth tells a much more interesting story. Figure 2 shows not only the job openings data since 2000 but also the associated hire rate, quit rate (voluntary), layoff rate (involuntary), and total separation rate (both voluntary and involuntary). What we see is that the higher-than-usual job openings level is at a historic high, though recent data show a decline. However, notably, separations and hires are both slightly elevated but generally consistent with historical levels.

Each of these observations makes sense on its own: job openings are higher to accommodate higher consumer demand; hires are up as a result; and separations are higher because there is a strong demand for labor, encouraging workers to look for better jobs or higher pay. This is further supported by the observation that layoffs are down and quits are up, once again showing that employees are leaving jobs at elevated rates, presumably for new jobs. But not always.

Figure 2: JOLTS data might indicate the labor market is healthy today, but the magnitude of job openings stands out. (Source: Bloomberg Finance, LP)

For us, the canary in the coal mine is that job openings are so high relative to the other measures. We understand consumer demand is high, and therefore companies are looking to serve that demand through hiring, but why does it seem that there is such a historically disproportionate deviation in job openings right now? There would appear to be some secular shift in the labor market that is creating an unprecedented supply/demand imbalance.

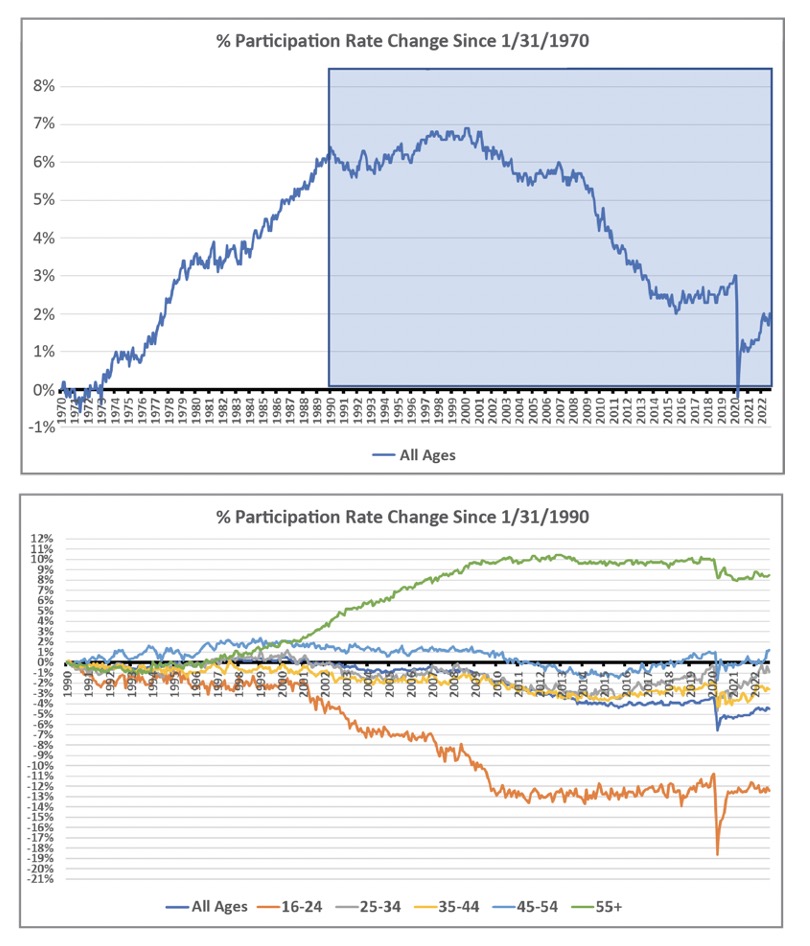

The answer lies in participation data. Figure 3 shows the change in labor force participation since 1970. As we can see, the participation rate increased dramatically from 1973 until it peaked right around the turn of the millennium. The rates began to decline not because of a cyclical story related to the pandemic, supply chains and inflation over the last few years but for a multitude of reasons dating back to the early 2000s. That is, this is a longer-term phenomenon that started well before the Fed's current free money era after the 2008 financial crisis.

Figure 3: Labor force participation rates (normalized to show change since January 1970 in the top chart and change since January 1990 in the bottom chart) show long-term secular trends which began well before the current economic cycle. (Source: Bloomberg Finance, LP)

If we drill down further into the period since peak participation and look at the rates by age demographic, also in Figure 3, we see a stark trend. Note that the chart shows changes in participation since the base year, in this case 1990. The participation rates among 55+ workers surged from their levels in 1990 in an almost direct offset to a drop in participation rates among the youngest workers between the ages of 16 and 24. While participation is down overall from that early 1990s peak, the primary driver of that decline is a transfer of jobs from young to old, plus even more decline among younger workers. Labor force participation rates among the other demographics were relatively flat over the past 30 years.

Speculating about the many reasons why we see this trend is beyond the scope of this letter. However, the baby boomer generation, the oldest of which reached the age of 55 around 2003, is the subject of our next observation. What we also see in Figure 3 is that the pandemic resulted in a step down in participation among the 55+ demographic. In our view, this is not just a cyclical story of layoffs. It's a secular story of the baby boomers retiring.[2]

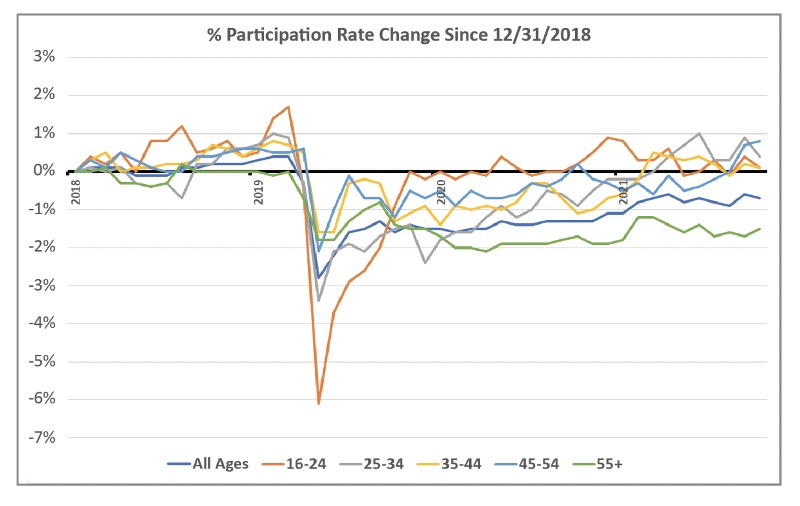

Figure 4: Changes in labor force participation rate since December 2018 show declines to be primarily due to participation declines among 55+ workers. (Source: Bloomberg Finance, LP)

Figure 4 brings this into clearer focus, as we look at changes in participation rates by age group since the end of 2018. Yes, overall participation is down. But actual participation among younger demographics is generally higher. The only group who has a lower participation rate and is bringing down the overall average are those who are age 55 and higher. While recent data shows that the trend is not entirely downward (probably in part due to the loss in 401k balances that have taken place in 2022), the takeaway is unmistakable. Those expecting labor force participation rates to increase may be in for a disappointment. We believe these rates have declined as the baby boomer generation has aged. What we may be seeing is a reversion to levels not seen in half a century.

The Kids are Alright (and So Are Their Parents)

That said, before readers see this as a sign that consumer demand will soften as we lose workers who will not come back, we refer you to the very low participation rates among the 16-24 demographic. Even if the decline in young worker participation does not reverse enough to offset a retirement wave in the same timeframe, the income of the 55+ worker is substantially higher than that of the 16- to 24-year-old worker. We believe that this demographic shift could have a stabilizing effect on consumer demand at a permanently higher level.

First, a worker leaving the workforce due to retirement does not have nearly the negative impact on demand aggregate spending as a younger worker who gets laid off. Rather, that spending is serviced not from earned income but from passive income, investments, and retirement savings. Second, the retirement of an experienced and higher-earning employee enables a company to fill multiple job openings with younger, lower-cost workers. While this would reduce the number of available job openings, it would also keep unemployment at a historically low level while further bolstering consumer demand. For each retiree, we could have two newly employed workers whose age demographic is more likely one of spenders than savers.[3] Third, this potential for a long-term reset to higher consumer demand levels drives inflation, which, as we learned earlier, puts upward pressure on wages, feeding into the ongoing cycle of demand and prices, making the Fed’s job that much more difficult.

The Bottom Line: Tight Labor Markets Bode Well for Fixed Income Investors

In our view, labor markets may be structurally tight for a long time to come, which could force the Fed to keep rates elevated. With persistently low unemployment, the Fed may not be able to loosen policy as consumer demand will already be strong. This means bond yields will likely stay higher for longer and the fed funds rate may remain anchored somewhere near (or above) its current level, creating what we believe is the most favorable fixed income investment environment in decades. This is very good news for investors who want actual income from their fixed income.

Venk Reddy is the Chief Investment Officer of Sustainable Credit Strategies at Osterweis Capital Management. Established in 1983, Osterweis Capital Management is an independent asset manager with $6.3 billion under management as of September 30, 2022. The firm provides investment management services to institutions and individuals through mutual funds and separate accounts, offering both equity and fixed income investment strategies.

Important Disclosure Information

Past performance is no guarantee of future results. This commentary contains the current opinions of the authors as of the date above and are subject to change at any time. These opinions are not intended to be a forecast of future events, a guarantee of future results, or investment advice. This commentary has been distributed for informational purposes only and is not a recommendation or offer of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but is not guaranteed.

No part of this article may be reproduced in any form, or referred to in any other publication, without the express written permission of Osterweis Capital Management.

Please Note: If you are an investor, please advise us if you have not been receiving account statements (at least

quarterly) from your account custodian.

The fed funds rate is the rate at which depository institutions (banks) lend their reserve balances to other banks on

an overnight basis.

JOLTS is the Job Openings and Labor Turnover Survey conducted by the Bureau of Labor Statistics of the U.S. Department of Labor. The program involves the monthly collection, processing, and dissemination of job openings and labor turnover data. The data, collected from sampled establishments on a voluntary basis, include employment, job openings, hires, quits, layoffs and discharges, and other separations.

The Osterweis Funds are available by prospectus only. The Funds' investment objectives, risks, charges and expenses must be considered carefully before investing. The summary and statutory prospectuses contain this and other important information about the Funds. You may obtain a summary or statutory prospectus by calling toll free at (866) 236-0050, or by visiting the literature page. Please read the prospectus carefully before investing to ensure the Fund is appropriate for your goals and risk tolerance.

Mutual fund investing involves risk. Principal loss is possible.

The Osterweis Sustainable Credit Fund may invest in debt securities that are un-rated or rated below investment grade. Lower-rated securities may present an increased possibility of default, price volatility, or illiquidity compared to higher-rated securities. Investments in debt securities typically decrease in value when interest rates rise. This risk is usually greater for longer-term debt securities. The Fund is non-diversified, meaning it concentrates its assets in fewer individual holdings than a diversified fund. The Fund may invest more than 5% of its total assets in the securities of one or more issuers. Fundamental investing that integrates sustainability factors will entail deviations from the benchmark, potentially without resulting in favorable Environmental, Social, or Governance (ESG) outcomes.

While the fund is no-load, management fees and other expenses still apply. Please refer to the prospectus for more information.

Osterweis Capital Management is the adviser to the Osterweis Funds, which are distributed by Quasar Distributors, LLC. [OSTE-20221209-0710]

[1] It is worth pointing out that, in our view, Chairman Powell takes seriously the fact that his mandate comes from Congress and the American people. While “full employment” (along with inflation, the Fed’s dual mandate) does not mean 0% unemployment, we believe he is head and shoulders above his predecessors in understanding the impact of traditional economic theories and the Fed’s actions on the most vulnerable workers in the economy. Where some see the last three years as a series of obvious and avoidable monetary policy blunders, we believe the factors the Fed was aiming to balance make for a more nuanced debate on merits and tradeoffs.

[2] It seems the Federal Reserve agrees with our assessment. In his speech at the Brookings Institute on November 30, Fed Chair Jay Powell said this: “Recent research by Fed economists finds that the participation gap is now mostly due to excess retirements—that is, retirements in excess of what would have been expected from population aging alone….” In this case, Powell was citing the data to support the case for continued restrictive monetary policy addressing the current economic cycle. We believe it is only a matter of time before the Fed starts talking about widespread retirements auguring in a paradigm shift with much longer-term implications for the economy and monetary policy.

[3] This is often true for a variety of reasons. Younger workers tend to be lower income, making it more difficult for them to save. Furthermore, the save vs. spend decision becomes more present for those in the next two demographic tiers as higher incomes and life decisions regarding housing, families and other priorities demand a focus on long-term planning. And when workers get close to retirement (or after), they turn back into spenders again as they use the savings they accumulated during their prime working and saving years.

© Osterweis Capital Management

More Sustainable Investing Topics >