Municipal Outlook: Fresh Opportunities After the Pressures of 2022

1. 2022 was a challenging year for the municipal bond market. What were the dynamics that drove the selloff and what is your outlook for the sector going forward?

Last year’s sharp rise in rates manifested in several ways across the state and local market. To begin with, it severely curtailed supply. Issuance fell more than 20% from the previous year as refinancing issuance quickly became uneconomic. In addition, the combination of higher rates and higher construction and labor costs lifted the bar for capital investment, making it more difficult for issuers to meet the hurdle rate. The deceleration of issuance resulted in a shortage of paper in the intermediate portion of the yield curve. And with rates rising sharply, investors demonstrated an aversion to longer-duration exposure and a strong preference to reinvest in shorter-duration, higher-quality paper in the intermediate portion of the yield curve. Paradoxically, in a period where short rates were rising more than long rates, intermediate municipal bonds were in very strong demand.

Looking ahead, our outlook for the municipal bond sector is relatively sanguine. We expect carry to provide a good cushion and supply conditions should remain thin. Credit fundamentals appear sound, and we expect positive relative performance compared to other high-quality alternatives, even in a downturn scenario.

2. Municipal mutual funds experienced the largest outflow cycle on record in 2022, with more than $143 billion in fund outflows. What drove those outflows and how do you expect flows to trend in 2023?

The record outflows for municipal mutual funds were a symptom of rising rates. Fund flows tend to reflect marginal demand in the municipal market, which dropped as fund investors saw the impact of higher rates on their mutual fund holdings. Tax-loss selling also contributed to outflows as investors realized losses to offset future gains and sought to reinvest at higher tax-exempt yields.

We think the pressure from fund liquidations and tax-loss selling will likely begin to dissipate as the cycle runs its course and sellers leave the market.

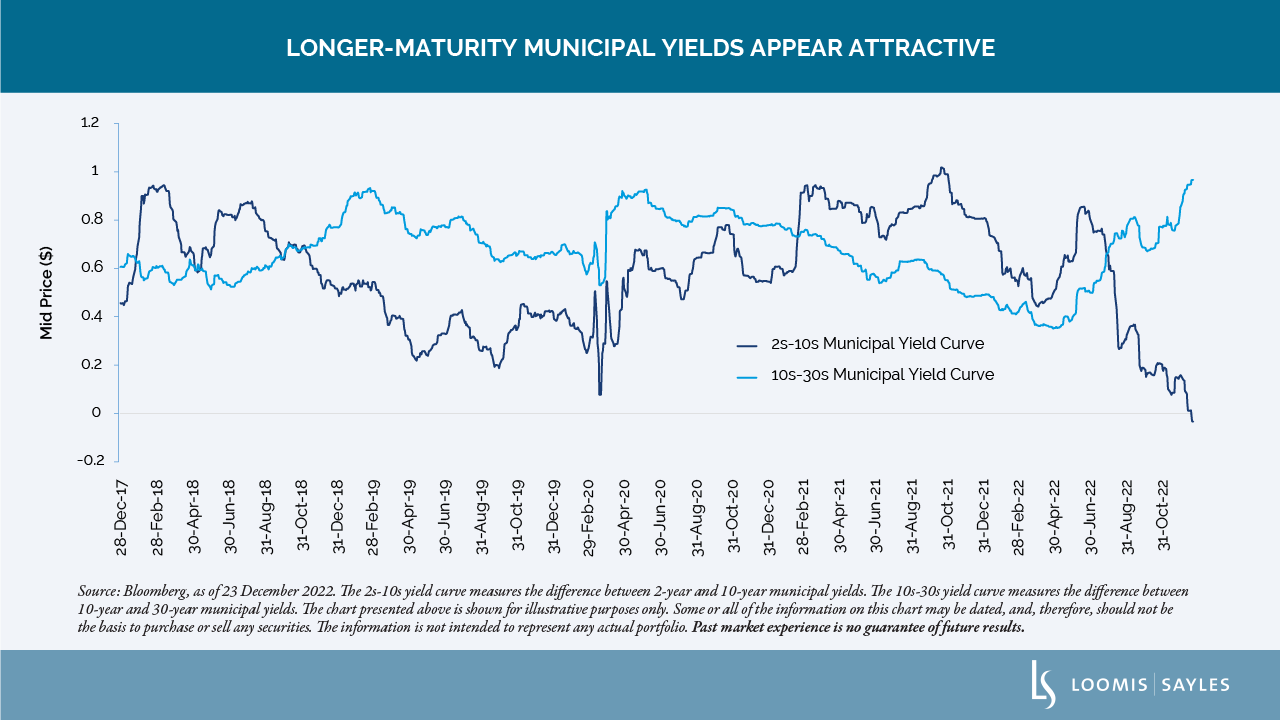

3. How did the municipal yield curve respond to the changes in the market? What does the yield curve tell us about relative value?