Municipal market participants are still recovering from the municipal market beatdown of 2022, which saw the worst performance (-8.53%) of the Bloomberg Municipal Bond Index since 1981.

Rising interest rates driven by the Fed’s inflation-fighting tightening strategy drove individual investors out of open-end mutual funds as outflows totaled $148 billion for the year. These redemptions created heavy selling pressure for fund managers. Average daily “Municipal Bid Wanted” activity reported by Bloomberg for 2022 was $1.358 billion. This was nearly two-and-one-half times the average daily amount of $556 million for 2021 and nearly twice the daily average for 2017-2021 of $708 million.

The extreme selling pressure required municipal market broker-dealers to adjust bid/offer spreads as they tried to match sellers with buyers and provide liquidity in a volatile Treasury market environment that made hedging risk positions more challenging.

While there were some brief periods of positive performance in May, July and November, the net result of the 2022 municipal bond market sell-off is that tax-exempt bond yields have started the new year at significantly higher levels than a year earlier. On January 3, 2023, AAA tax-exempt yields in five years were at 2.53% - 195 basis points (bps) higher than a year ago, in 10 years at 2.62% - 157 bps higher and in 30 years at 3.56% - 206 bps higher.

More Attractive Yields

Higher absolute yield levels provide an attractive “re-entry” point for municipal market investors. Many individual investors that were year-end tax management sellers have turned into buyers to start the year. Selling pressure has subsided and along with a limited municipal new issue calendar, demand for municipal bonds has been strong for the first two trading weeks of 2023. AAA tax-exempt yields have declined 30 bps in 5-year bonds, 29 bps in 10-year bonds and 28 bps in 30-year bonds from January 3rd to 13th.

While the market acknowledges the Fed will continue to tighten in February and March, there is also wide expectation that it will pause and be on hold for some time before reversing course and beginning to ease. With this consideration, how should a municipal investor think about the risks of re-entering the tax-exempt bond market at this time?

An investor should make municipal bond investment decisions based on several factors, including paying attention to expected Fed policy actions and the overall economic environment, characteristics of municipal credit, as well as the specific technical supply/demand factors that impact tax-exempt bond yields and prices.

Let’s look at the economics of tax-exempt bond ownership through several examples:

Investment Grade Tax-Exempt Bond

$100,000 4.00% bond due 1/01/2033 – 10-year maturity/non-callable/rated AAA

Purchase Price: $114.821

Purchase Yield: 2.33%

Current Yield: 3.48%

Tax-equivalent yield: 3.93%*

Annual income: $4,000

* Federal tax rate of 40.8%

High Yield Tax-Exempt Bond

$100,000 5.00% bond due 1/1/2058 – 35-year maturity/callable in 6 years/rated BBB

Purchase Price: $101.095

Purchase Yield: 4.80%

Current Yield: 4.946%

Tax-equivalent yield: 8.108%*

Annual income: $5,000

* Federal tax rate of 40.8%

The Investment Grade bond offers tax-free income of $4,000 over the next year. If the investor intends to hold the bond to maturity, changes in prices and yields over the holding period do not matter. But if the investor has a more active, total return focus, the direction of yields and prices are important. Tax-exempt interest rates would need to go up 42 bps over the next year for the $4,000 income to be offset by an increase yield of the Investment Grade bond to 2.75% and corresponding price decrease to $110.821.

In the case of the High Yield bond, which generates $5,000 of annual income, tax-exempt interest rates would need to rise by 44 basis points, increasing the yield on the example bond to 5.243% which corresponds to a decline in price to $96.095.

Note that when the Fed ultimately eases interest rate policy, municipal interest rates should decline. Bond prices will rise, and investors can expect capital appreciation, in addition to the tax-exempt income they have been receiving.

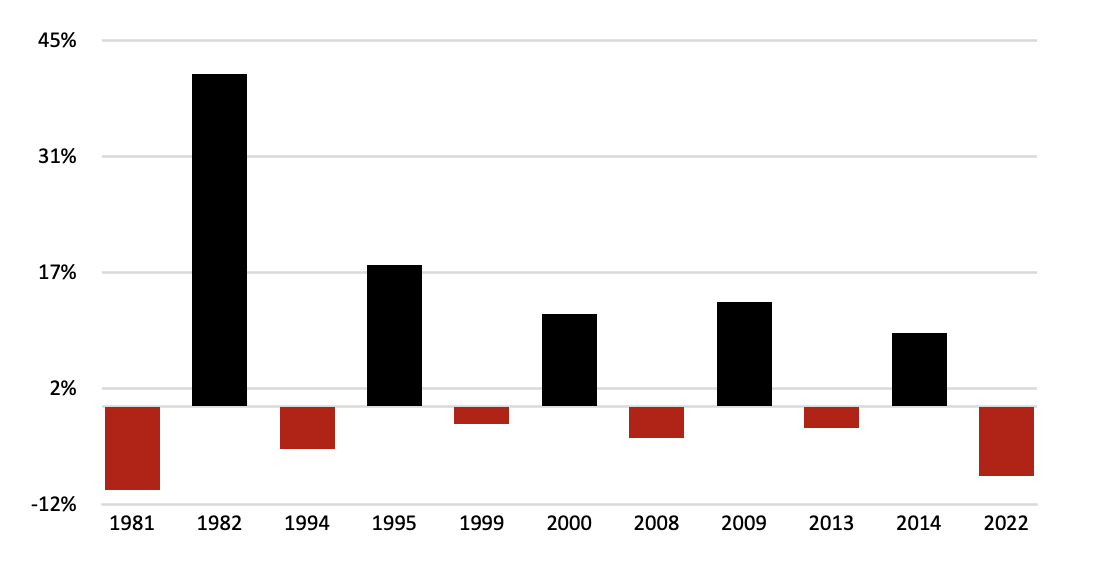

Will History Repeat Itself?

Investors considering re-entry into the municipal market after the pain of 2022 can find some comfort in a review of historical data. The chart below shows the significant positive performance of investment grade municipal bonds in the year following five prior periods of negative performance.

Investment Grade Municipal Bond Performance After Negative Return Years

Source: Bloomberg Municipal Bond Index

Relative Credit Quality of Municipal Bonds

As concerns over an economic downturn or recession continue it is important that municipal market investors understand how the unique characteristics of municipal borrowers enhance their ability to pay during stressful periods relative to some corporate bond. Moody’s Investors Service’s most recent default study reports that the average five-year municipal default rate since 2012 is 0.1%, compared to an average five-year global corporate default rate of 7.2% since 2012.

Municipal bond default rates are lower than corporate bond default rates for several reasons, including:

- Many municipal bond issuers have strong security features, including the power to raise taxes and fees which provide reliable and steady cash flow.

- Municipal bond issuers finance essential public services including, roads, mass transit, power, water and sewer, education, airports, and hospitals.

- Many general obligation issues – especially states that have attempted to maintain rainy day reserves – have built up revenues in times of surplus to help in leaner times. Most revenue bond issues are structured with debt service reserve funds sized at 6- or 12-month’s maximum principal and interest to provide liquidity in the event of unforeseen revenue interruptions.

- Last, municipal bonds are generally structured on a pay-as-you-go basis with amortization. Maturity structures are based on the expected useful life of the related facilities or program purpose. Therefore, large bullet principal payments are avoided – unlike many parts of the corporate bond market.

- In addition, municipal issuers, together with the public finance community, are extremely focused on debt management and actively take opportunities to refinance and lower borrowing costs.

Timing and Relative Value Analysis Considerations.

Entry and exit points for municipal bond investors matter – especially for a total return focused investor. Given the large retail investor component in the tax-exempt market, price and yield movements are especially driven by technical supply and demand factors – the size of the primary market calendar for new issuances of municipal bonds, open-end mutual fund and ETF flows as well as reinvestment cash flow from interest payments and bond redemptions.

In addition, the relative richness or cheapness of tax-exempt bonds to taxable alternatives is also important to watch. Crossover investors – banks, insurance companies and hedge funds –step in and out of the tax-exempt market based on real-time relative value analysis. These marginal investors can drive prices in either direction based on their level of activity. Paying attention to timing and relative value is just as important as following the overall economy and rates markets.

Separately Managed Accounts

Net asset values were adversely affected when investors fled open-end mutual funds in 2022. One way to protect yourself from the “herd mentality” is to consider a separately managed account (SMA). Whether you prefer a buy-and-hold laddered income-oriented strategy or a more actively managed total return strategy focused on income and capital appreciation, a professional manager with credit and trading expertise can help you navigate the municipal bond waters and achieve your objectives.

David Falk is a portfolio manager at Shelton Capital Management.

Important Information

Investors should consider a fund’s investment objectives, risks, charges and expenses carefully before investing. The prospectus contains this and other information about a fund. To obtain a prospectus, visit www.sheltoncap.com or call (800) 955-9988. A prospectus should be read carefully before investing.

It is possible to lose money by investing in a fund. Past performance does not guarantee future results. Any projections or other forward-looking statements regarding future events or performance of markets, companies, or otherwise are not necessarily indicative or differ from, actual events or results.

INVESTMENTS ARE NOT FDIC INSURED OR BANK GUARANTEED AND MAY LOSE VALUE.

© Shelton Capital Management

Read more commentaries by Shelton Capital Management