The FOMC Won’t Blink

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsFebruary 1, 2023

Inflation May Not Be Dead Yet

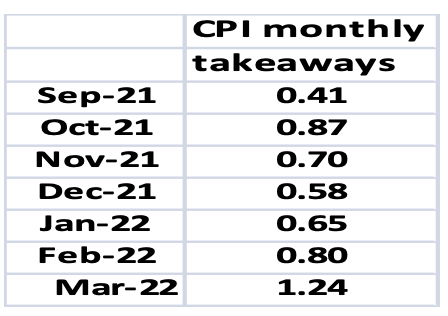

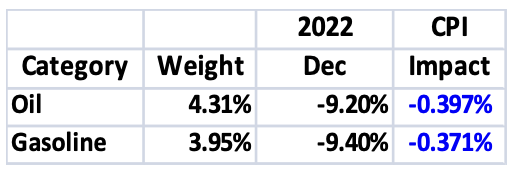

As expected and discussed in the January Macro Tides the December Consumer Price Index (CPI) dropped below 7.0% falling to 6.5% from 7.1% in November. The takeaway value from December 2021 was -0.58% and the month over month change was -0.1%. As you can see the largest contributor to the decline in annual inflation was the subtraction of -0.58%. The -0.1% decline from November in December was eye catching since it was the first monthly decline since May 2020. The primary reason for the dip was a huge decline in oil and gas prices during December. Oil was down -9.2% and Gas fell -9.4%, and based on their weights in the CPI (oil 4.05% - Gas 3.95%), contributed -.768% to the -0.1% drop. If it weren’t for the outsized declines in energy, the monthly change for the CPI would have been 0.6%, and the annual change would have risen to 7.2% instead falling to 6.5%. The large unexpected drop in the headline CPI reinforced the bullish Wall Street narrative that the FOMC will be able to stop increasing the Funds rate sooner and begin lowering it the second half of 2023.

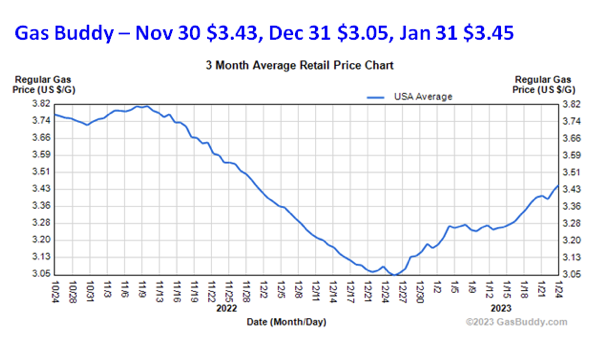

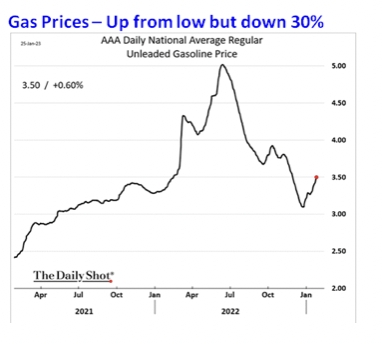

This bullish narrative may encounter a speed bump in January since energy prices have ticked higher with Gas prices leading the charge. The correlation between Gas Buddy’s national gas prices and the CPI’s measurement of gas prices is not perfect but helpful. In December the price of a gallon of regular gas decline by -9.0% according to Gas Buddy (3.43-3.05), which is a bit less than the CPI’s fall of -9.4%. Since the end of December Regular Gas is up 13.7% as of January 31. WTI crude oil futures are up slightly in January, so it’s unlikely they will be lower in the January CPI report due out on February 14. Rather than declining by -0.1% as in December, the monthly change for January could easily be 0.3% or higher based on the increase from gas. Wall Street probably won’t like that since it would show that inflation isn’t continuing to drop in a straight line manner. An increase of 0.3% won’t however prevent the annual headline CPI from falling more, since the takeaway value for January 2022 is -0.65%.The sharp decline in the CPI in the last few months surprised Wall Street. The speculation that the FOMC has already won the battle against inflation was fueled by the absolute -0.1% decline in the monthly CPI. A modest increase in monthly inflation in January will weaken the ‘inflation battle is over’ narrative and support the FOMC’s plan to increase the Funds rate to 5.0% - 5.25%.

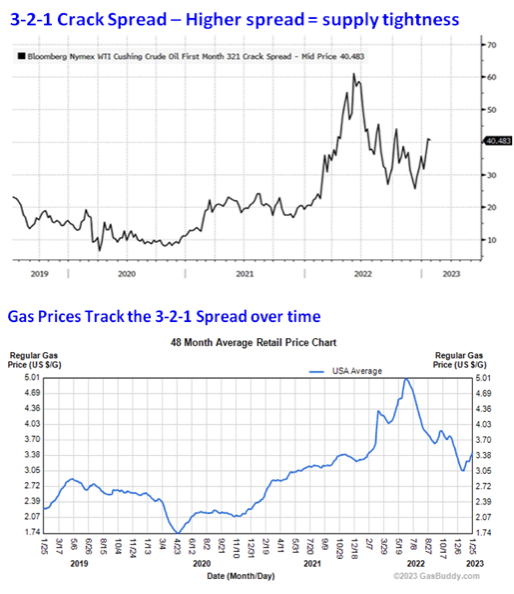

There is a good chance that the increase in gas prices may persist in coming months based on the 3-2-1 Crack Spread. The 3:2:1 crack spread is a very helpful indicator of how tight the oil market is. Higher spreads mean the market doesn’t have enough fuel, while low spreads indicate an abundance of supply. Since late December the Spread has increased from less than $30.00 to $44.00, which indicates that the oil market is tightening up for refined products like gasoline. If the refinery capacity to produce gasoline is reduced, the Spread will increase further and lift gas prices. According to refining intelligence firm IIR Energy, at least 15 oil refineries plan on closing in coming months from 2 to 11 weeks for maintenance. When the Spread soared to $60 in June 2022, many refineries postponed maintenance in order to capture profits due to the level of the Spread. That option is less attractive now and refineries need to close for maintenance or risk damage to expensive equipment. By mid-February closures will lower output by 1.4 million barrels a day, which is double the 5 year average. Nine more refineries plan to closing during the spring, so the upward pressure on the Spread and on gas prices is likely to intensify going into the summer driving season. With refinery capacity expected to drop in the next few months, gas prices will likely move higher, even if oil prices decline as economic growth stumbles. And if oil prices move up, the impact on gas prices will be magnified due to lower refining production. It’s possible that energy prices may pose more than just a one month speed bump for inflation.

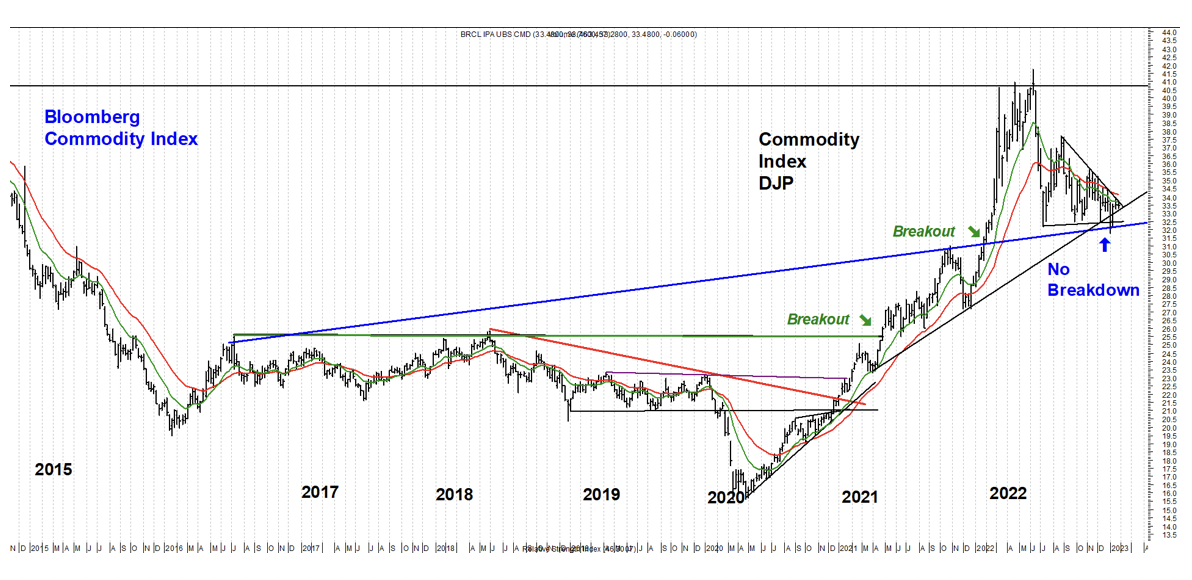

In the August 1 2022 Macro Tides I reviewed the Bloomberg Commodity Index since it had just undergone a steep correction in less a month after peaking in June. (DJP is the ETF that tracks the Bloomberg Commodity Index – Chart below) DJP peaked at 41.78 on June 8, and closed at 39.06 on June 15. By July 6 the Index recorded an intra-day low of 32.17 DJP was off -23.0% less than a month after the June 8 high. Wall Street looked at the quickness and steepness of the decline and concluded that commodities were delivering two loud and clear messages – Inflation had peaked and the economy might already be in a recession. This view was reinforced when GDP for the second quarter was reported on July 27 and showed a second quarter of contraction. As I noted back then, many commodities broke out of long term downtrends or sideways patterns in May 2021. This breakout was followed by some choppy trading for a few months and then another surge into October 2021. That surge was followed by a quick decline of -12.2% that ended in December 2021. A second breakout developed above the October high in late January 2022 in the lead up to Russia’s invasion of Ukraine on February 24, 2022.

In the August 1 2022 Macro Tides I reviewed the Bloomberg Commodity Index since it had just undergone a steep correction in less a month after peaking in June. (DJP is the ETF that tracks the Bloomberg Commodity Index – Chart below) DJP peaked at 41.78 on June 8, and closed at 39.06 on June 15. By July 6 the Index recorded an intra-day low of 32.17 DJP was off -23.0% less than a month after the June 8 high. Wall Street looked at the quickness and steepness of the decline and concluded that commodities were delivering two loud and clear messages – Inflation had peaked and the economy might already be in a recession. This view was reinforced when GDP for the second quarter was reported on July 27 and showed a second quarter of contraction. As I noted back then, many commodities broke out of long term downtrends or sideways patterns in May 2021. This breakout was followed by some choppy trading for a few months and then another surge into October 2021. That surge was followed by a quick decline of -12.2% that ended in December 2021. A second breakout developed above the October high in late January 2022 in the lead up to Russia’s invasion of Ukraine on February 24, 2022.

Although DJP had fallen by -23.0% from its peak in June, the decline stopped right at the important blue breakout trend line, as discussed last August. By not falling below the blue trend line, DJP indicated that the broad uptrend in many of the 23 commodities in the Index was still intact. After bottoming in July 2022, DJP rallied 17.1% before topping on August 23. In the last 6 months, various commodities have rallied and declined, but through it all DJP has continued to hold above the blue trend line. The low on July 6, 2022 was $32.17 and on January 5, 2023 DJP traded down to $31.78 and closed at $31.89. On January 6 DJP closed at $32.19 and above its June intra-day low of $32.17. The quick reversal off that low is a good sign.

As long as DJP doesn’t close below $31.89, it should move up to $35.50 and has the potential to rally back to the August high of $37.68, if it is tracing out an A-B-C rally from the July low. This chart analysis suggests that commodities in general are likely to rally in the next few months and keep the FOMC focused on increasing the Funds rate to 5.1%.

Federal Reserve

Chair Powell used his Brookings speech to pivot away from inflation being the dominant driver for monetary policy to the labor market. The majority of Wall Street strategists continue to over emphasize inflation, and as a result, conclude that the decline in inflation allows the FOMC to alter the course of monetary policy away from the higher for longer that every FOMC member has provided for months. The title of Powell’s speech was “Inflation and the Labor Market”, which implies that additional and lasting improvement in inflation is dependent of the labor market.

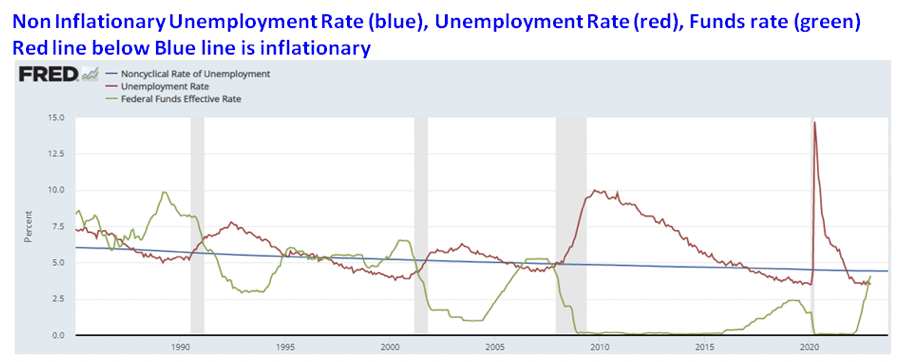

One measure of labor market slack that the FOMC uses is the Non-Accelerating Inflation Rate of Unemployment (NAIRU), which is the lowest level of unemployment that can occur in the economy before inflation starts to inch higher. In the last 40 years the FOMC has lifted the Funds rate (green), whenever the current Unemployment Rate (red) was below the NAIRU rate (blue), as calculated by the FOMC. The Unemployment Rate in December was 3.5% which is well below the current NAIRU rate of 4.6%. Chair Powell has repeatedly cited tightness in the labor market as why it’s appropriate for the FOMC to increase the Funds rate enough to moderate demand and create slack in the labor market. The projections provided at the December meeting call for the Unemployment Rate to rise to 4.6% in 2023 and 2024. This wasn’t a coincidence since that would lift the Unemployment Rate above the NAIRU rate of 4.6% and indicate that slack in the labor market was starting to develop.

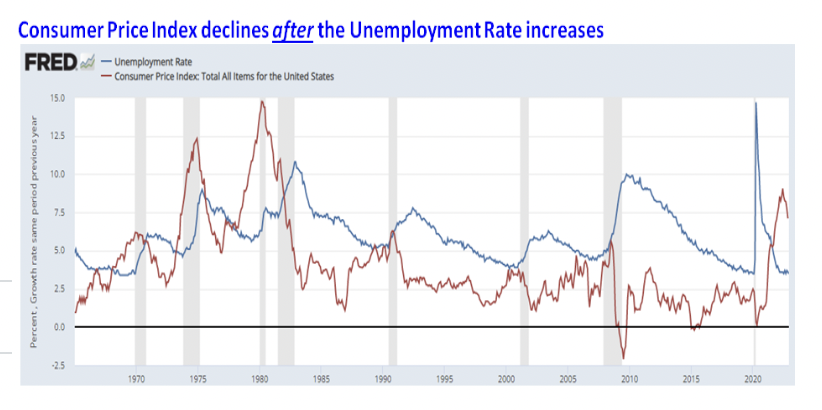

In the last 50 years the largest declines in inflation occurred after a large increase in the Unemployment Rate and after the economy entered a recession (shaded areas on charts). Chair Powell and many other members of the FOMC have said that they will get inflation down to 2.0% and will stay at it until they do. Chair Powell has said the greater risk is doing too little than too much, even if that increases the risk of recession. Wall Street believes the FOMC will blink once the Unemployment Rate starts to climb, or reverse course even if inflation isn’t near the FOMC’s 2.0% target. During the press conference after the December 14 FOMC meeting, Chair Powell was asked if the FOMC would increase the inflation target from 2.0% to 3.0%. “We're not considering that. We're not going to consider that. Under any circumstances, we're going to keep our inflation target at 2%. We're going to use our tools to get inflation back to 2%." History suggests the FOMC will need a recession to get inflation down to 2.0% over the next two or three years or longer.

Headline CPI Inflation was above 8.0% for seven consecutive months in 2022 and has been above 6% for fifteen months since October 2021. Research Affiliates studied 14 OECD developed economies from 1970 through September 2022 and found 52 instances in which inflation exceeded 4.0%. According to their research, the median number of years to bring inflation down to 3.0% after being above 8.0% is 10 years. If a recession develops in 2023 and 2024 it probably won’t take that long for inflation to come down to near 2.0%. But Research Affiliates analysis indicates it may not fall as quickly as Wall Street expects.

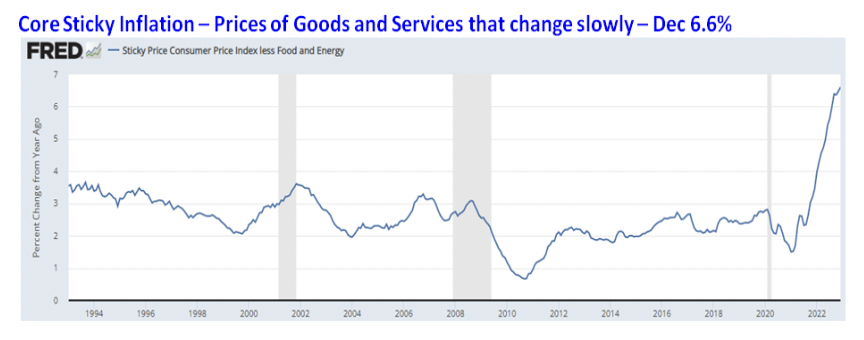

The Atlanta Federal Reserve developed an alternative measure of inflation that includes goods and services within the CPI that are relatively slow to change over time. Their ‘Sticky’ inflation Index reacts more slowly than the CPI, which means it takes more time for it to play catch up with changes in the CPI. The CPI has dropped from 9.1% in June to 6.5% in December, but the Atlanta Fed’s Sticky Inflation Index hit the high for this cycle in December at 6.6%. This suggests a broad based decline in inflation is likely to take time.

The Atlanta Federal Reserve developed an alternative measure of inflation that includes goods and services within the CPI that are relatively slow to change over time. Their ‘Sticky’ inflation Index reacts more slowly than the CPI, which means it takes more time for it to play catch up with changes in the CPI. The CPI has dropped from 9.1% in June to 6.5% in December, but the Atlanta Fed’s Sticky Inflation Index hit the high for this cycle in December at 6.6%. This suggests a broad based decline in inflation is likely to take time.

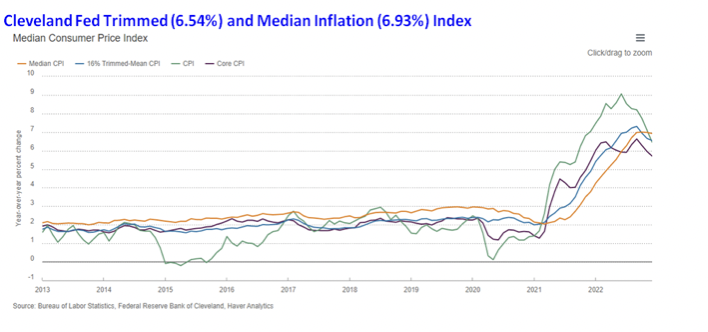

Wall Street likes to focus on the CPI, but members of the FOMC put more emphasis on the Personal Consumption Expenditures Index (PCE), but pay attention to the Sticky Inflation Index from the Atlanta Fed and the Trimmed Mean Inflation Index from the Cleveland Fed. The Trimmed Mean Inflation Index from the Cleveland Fed excludes the 8% of categories that have the largest and smallest contributions. It also provides the Median inflation level (orange) for the half of the categories that are above and half that are below, which is different than an average. The Trimmed Mean in December was 6.54% and the Median was 6.93%. Between 2012 and mid 2021 Median inflation was never above 3.0%, so the December level should temper some of the inflation has been vanquished sentiment. A review of a broad array of inflation metrics suggest inflation will continue to fall, but not enough to dissuade the FOMC from increasing the Funds rate to 5.1%.

Labor Market

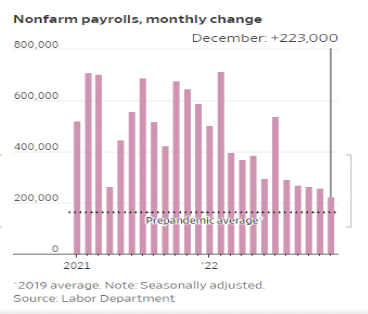

In December employers added 223,000 jobs a modest drop from the 256,000 added in November. Other than a big jump in July job growth slowed throughout 2022. In his Brookings speech, Chair Powell said that the economy needs to create 100,000 jobs each month to accommodate population growth. At a minimum monthly job growth will have to drop below 100,000 to begin to add any slack into the labor market slack. Given the level of labor market tightness there will need to be many months where job growth is below 100,000 to make a difference, or a number of months below 0. Even if the ‘soft landing’ is achieved, there will be a number of months in which job growth is negative.

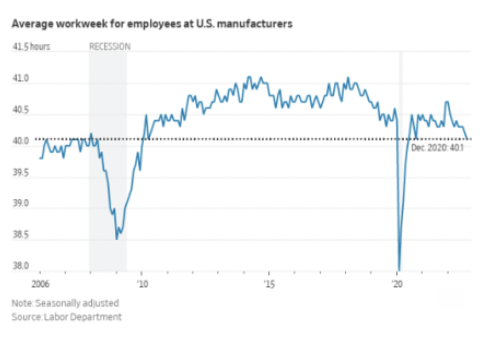

Wage growth also moderated in December as Average Hourly Earnings (AHE) increased 0.3% versus 0.4% in November, and the annual increase dipped from 4.8% in November to 4.6% in December. The Average Workweek fell to 40.1 hours which is the lowest since 2010 as was factory overtime at 2.9 hours. Although the number of Temporary workers has declined 110,000 since peaking in August, a small portion of the decline is likely from employers offering the temp worker a job in a still tight labor market. In aggregate the early warning signs that the labor market is cooling discussed in detail in the January Macro Tides continues. However, none of these factors directly addresses the problem of easing labor market tightness.

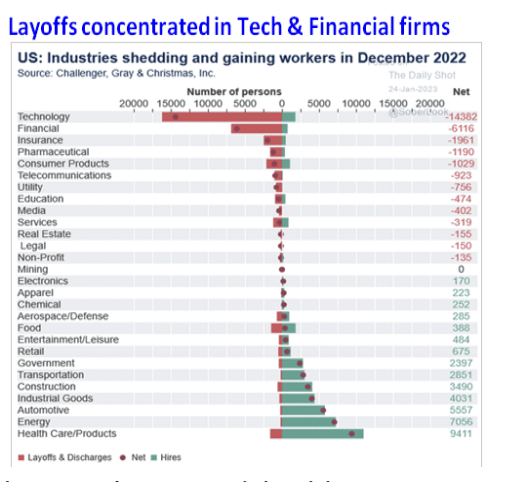

The Unemployment Rate dropped to 3.5% tying a 53 year low in December and Unemployment Claims are hovering near their lowest level in decades. There have been high profile layoffs by technology firms (Meta, Google, Amazon, Microsoft), which gives the impression that things must be bad if the giants are being forced to let workers go. Business is slowing but the layoffs are also a function of the aggressive hiring many tech firms did when the Pandemic boosted business significantly. Financial firms with exposure to the plunge in the housing market, mortgage lending, dearth of Initial Public Offerings, and M&A activity have also cut staff. The key point is that the majority of industries are not letting workers go, so the weakness has been limited. Some tech workers are finding employment quickly and those that aren’t received healthy severance packages, which may explain why Unemployment Claims haven’t increased.

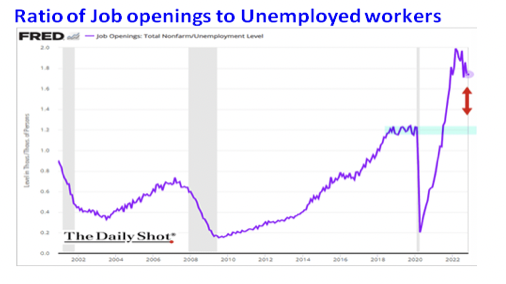

While a few large companies have been letting workers go, small businesses have more than picked up the slack. Since February 2020 businesses with less than 250 employees have hired 3.67 million people compared to large firms (more than 250) that have cut 800,000 jobs. According to the November Job Openings and Labor Turnover Survey (JOLTs) survey, 78% of open jobs were by small businesses. The number of job openings in the JOLTs survey in November held steady at 10.5 million. The Ratio of job openings to the number of unemployed workers was 1.7. Chair Powell has referenced this ratio often and it shows that the demand for labor is still high.

There are early signs that strength in the labor market is moderating, but actual weakness that would increase the amount of slack in the labor is lacking. The ongoing growth of jobs and overall tightness in the labor market gives members of the FOMC confidence that additional rate hikes are warranted.

Economy

GDP increased 2.9% in the fourth quarter a slight dip from the third quarter’s growth of 3.2%. Even after GDP dropped in the first and second quarter of 2022, I explained in the August Macro Tides why the economy wasn’t in a recession and that a recession wouldn’t begin in 2022. GDP in 2022 was up 1.0% from December 2021. The FOMC has increased the Funds rate by 4.25% since March, but a recession may hold off until after mid 2023.

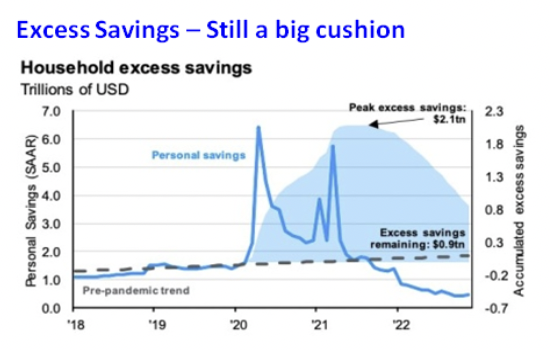

Consumer spending represents almost 70% of GDP and is being sustained by the lowest Unemployment Rate in 53 years and gains in wages. Although Average Hourly Earnings were up 4.6%, that number understates the actual increase. According to the Labor Department, Median weekly earnings for all workers were up 7.4% in 2022. The bottom 10% of wage earners experienced a 10% increase, so they benefitted more than any other group. The increase in wages is helping consumers stretch the Excess Savings they accumulated during the Pandemic.

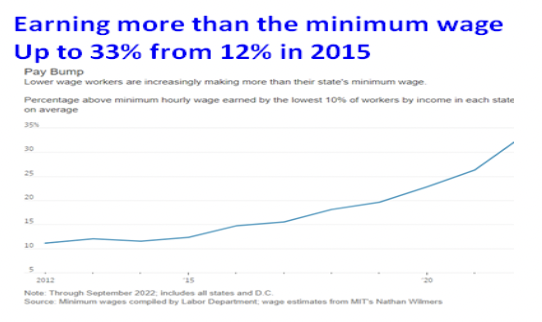

A record number of employees are quitting their job each month (4.2 million in December) because they can get an immediate increase in pay by switching. According to the Atlanta Fed, job switchers earned 7.7% compared to 5.5% for those who didn’t leave an existing job. In order to cut down on turnover, many companies are increasing wages to prevent good workers from going to a greener pasture. Walmart announced that it was increasing pay from $12 an hour to $14 (16.6%), for 340,000 of Walmart’s 1.6 million workers starting in March. On January 1, the minimum wage was increased in 26 states, which will result in income creep for workers earning just above the minimum. Since 2015 the percentage of workers earning more than the minimum wage has climbed from 12% to 33%.

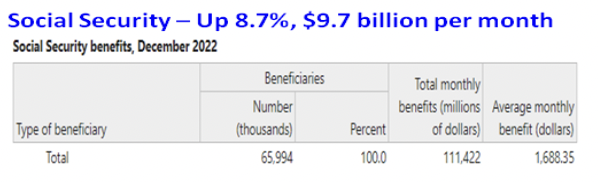

On January 1 66 million Social Security recipients received a pay increase of 8.7%, which amounts to an increase $9.7 billion in monthly income. In 2023 Social Security will disburse $116 billion more than in 2022 that will help seniors sustain their spending.

Most Consumers are in good shape. They still have a healthy cushion of Pandemic savings, wage growth is solid, the labor market is resilient, and the Unemployment Rate is historically low. The bottom 25% of wage earners have likely run through most if not all of their Pandemic savings, but higher than average wage growth is helping. While gas prices are up 11% from the low, they are down 30% from the June high. A year ago the return on savings was 0%, but consumers can now earn 4% or more and actually generate real income. The increase in credit card balances is an indication of stress for some consumers, but overall consumers have the wherewithal to keep spending. That will change once the Unemployment Rate begins to rise in the second half of 2023, and more Pandemic savings have been spent.

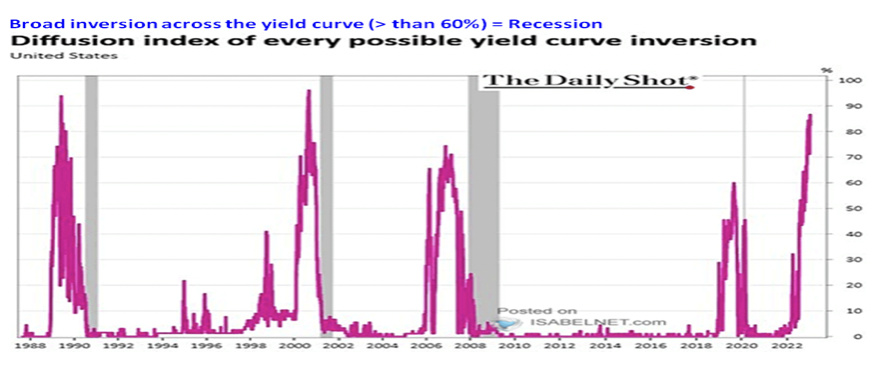

Despite the factors that are likely to sustain consumer spending in the near term, the odds of a recession beginning after mid-year are high based on the signals from 3 reliable recession indicators.

Inverted Yield Curve

The yield curve is considered inverted when the 2-year yield is above the 10-year Treasury yield. A stronger signal is provided when more than 60% of the yield curve is inverted, which is the case now.

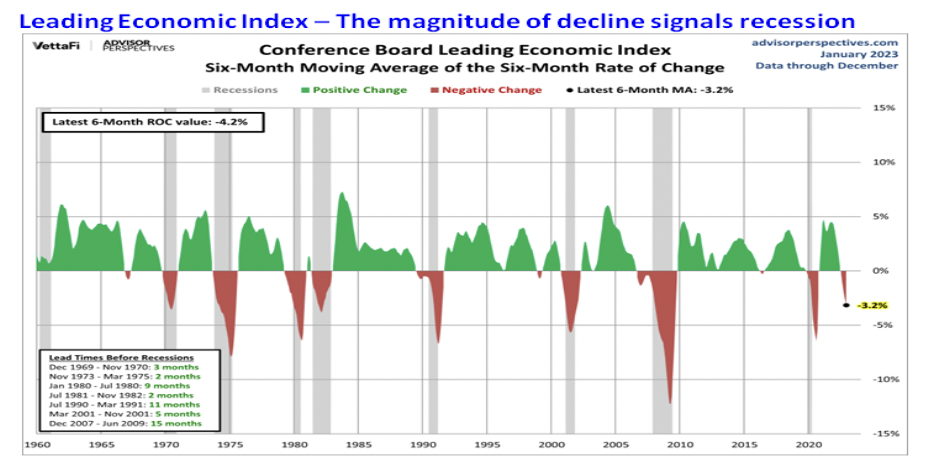

Leading Economic Index

The Leading Economic Index (LEI) is comprised of 10 separate economic data points including the yield curve. The LEI has declined for 10 consecutive months, and the magnitude of the drop has always presaged a recession in the last the 60 years (shaded areas).

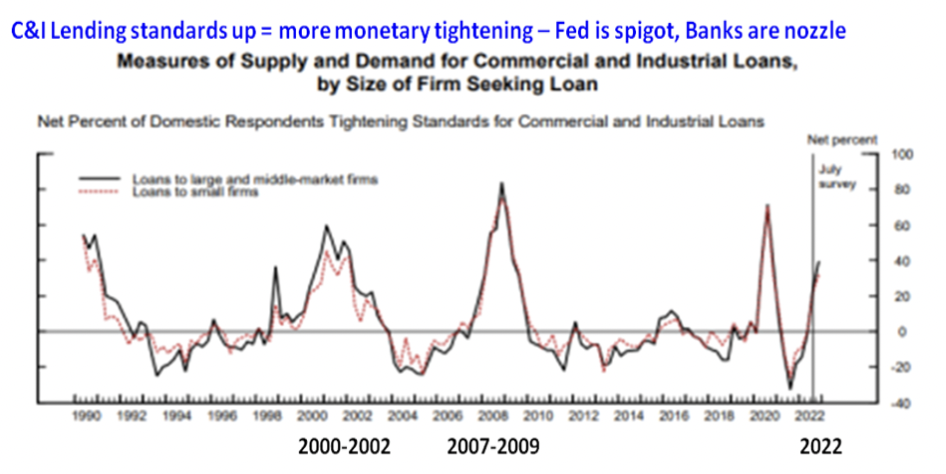

Lending Standards

In the third quarter banks aggressively tightened lending standards, which represents another form of tightening of monetary policy. The FOMC has increased the cost of borrowing, and now banks are curbing the availability of credit. The Federal Reserve is the liquidity spigot for the financial system, and banks are the nozzle at the end of the liquidity hose that governs the amount of liquidity flowing into the economy. As banks increase lending standards, the amount of liquidity flowing into the economy is less so economic activity slows. As the economy exhibits more signs of slowing in coming months, banks will increase lending standards further. This is what banks did in 2001, 2008, and in the early stages of the Pandemic. Given the rising concerns about a recession in 2023, banks likely increased lending standards further in the fourth quarter.

There has been a lot of talk regarding the inverted Yield Curve, some discussion of the decline in the LEI, but virtually no one has focused on the increase in Lending standards. This Who’s Who of recession signals have provided accurate and reliable forewarnings of a recession in the past, and are likely correct in signaling that a recession is coming in 2023. The economy will hold up until it doesn’t, which reminds me of one of Hemingway’s character’s description in the ‘The Sun Also Rises’ about bankruptcy: “Gradually and then suddenly.”

FOMC Meeting on February 1

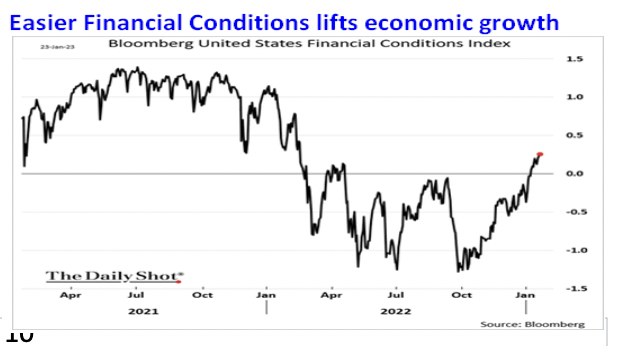

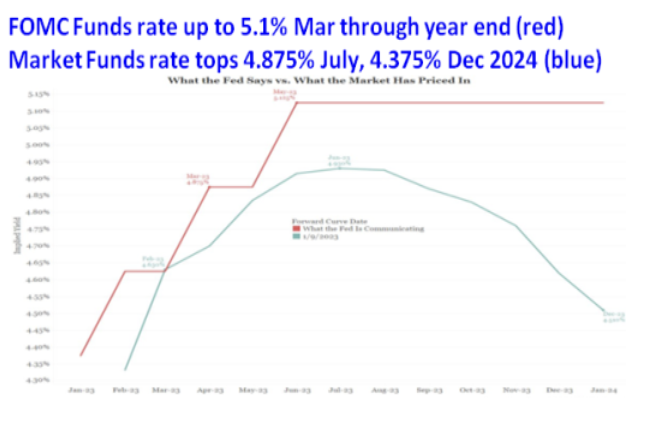

Financial Conditions have eased significantly since October due to the decline in Treasury yields, rally in the stock market, 11% fall in the Dollar, and the narrowing of credit spreads. The FOMC slows economic growth by tightening Financial Conditions, so the easing of Financial Conditions since October is counter to what the FOMC is trying to achieve. This has not gone unnoticed by the FOMC, and the minutes of the December meeting show this was discussed. “Participants noted that, because monetary policy worked importantly through financial markets, an unwarranted easing in financial conditions, especially if driven by a misperception by the public of the Committee’s reaction function, would complicate the Committee’s effort to restore price stability. Several participants commented that the medians of participants’ assessments for the appropriate path of the federal funds rate in the Summary of Economic Projections, which tracked notably above market-based measures of policy rate expectations, underscored the Committee’s strong commitment to returning inflation to its 2 percent goal.” These comments are blunt and unusual. The FOMC is basically saying Wall Street perceptions of monetary policy are wrong, since market based estimates for the Funds rate remain below what the FOMC’s projects.

Wall Street thinks the FOMC will hike the Funds rate to 4.75% - 5.0% by May, and then begin lowering it in the second half of 2023 and in 2024 by -1.50%. Wall Street also expects a soft landing which doesn’t jibe with why the FOMC will cut rates so aggressively, if there isn’t a recession. And if there is no recession, how will the tightness in the labor market disappear and service inflation come down enough to justify rate cuts? These are logical questions and Wall Street ignores them since it doesn’t have an answer for them. The FOMC lost a lot of credibility in 2021 after sticking to the ‘inflation will be transitory’ theme, which I might add Wall Street liked since it was bullish for stocks and bonds. Wall Street now thinks the FOMC will be wrong about the economy, Unemployment, inflation, and the Funds rate. Wall Street is playing a Game of Chicken with the FOMC, by dismissing the FOMC’s resolve to bring inflation down after being so wrong about inflation in 2021.

Neel Kashkari is President of the Minneapolis Federal Reserve and was considered the most Dovish member on the FOMC after joining in November 2015. In 2022 that changed and Kashkari emerged as one of the more Hawkish members. In an interview in December, he said he supported increasing the Funds rate to 5.4% comfortably above the FOMC’s median of 5.1%. Kashkari reflected on why Chairman Paul Volker’s aggressive inflation policy was worth the short-term pain it caused. “While what Volcker did was painful in the moment, it paid dividends for decades.” In other words, a recession in the next year would be worth the pain it caused, if it led to stable growth that lasts a long time. During the interview Kashkari was asked about the discrepancy between the FOMC’s projection of maintaining the Funds rate at 5.1% through the end of 2023, and Wall Street’s expectation that the FOMC will cut the Funds rate in the second half of 2023. The interviewer commented that it almost seemed as if the markets were playing chicken with the Fed. After chuckling, Kashkari said, ““I’ve spent enough time around Wall Street to know that they are culturally, institutionally, optimistic. They are going to lose the game of chicken, I can tell you that.”

After bottoming in July, Financial Conditions eased a lot in August. On August 25 Chair Powell used his brief 8 minute Jackson Hole speech to deliver a gut punch to Wall Street’s expectation that the FOMC would not increase the Funds rate since the economy was already in a recession. In response to his speech, the S&P 500 dropped from 4202 to 3600 in the following 6 weeks. The 10-year Treasury yield jumped from 3.1% to 4.33% in mid October. As a result Financial Conditions tightened significantly.

Wall Street expects the FOMC to increase the Funds rate by 0.25% at the February 1 meeting and assigns a probability of 99%. Whether the FOMC does or not, Chair Powell may use the post meeting press conference to dampen Wall Street’s enthusiasm. The FOMC has moved quickly over the past year to play catch up after being so wrong about inflation being transitory. After Chair Powell said that inflation represented a ‘severe threat’ on January 12, 2022, the FOMC increased the Funds rate at three consecutive meetings. In March the FOMC said it would increase the Funds rate to neutral as ‘expeditiously as possible’. Chair Powell pegged the neutral rate at 2.5% and the FOMC used four 0.75% hikes to get to and beyond the neutral rate. The FOMC has said it now wants to increase the Funds rate to 5.1% from 4.25%. Given how the FOMC has behaved, it isn’t unreasonable to think the FOMC might increase the Funds rate by 0.50% rather than the 0.25% expected. If the FOMC wants to have Financial Conditions unwind some of the easing since October, a larger increase might get the ball rolling. Irrespective of the size of the next increase, the key discrepancy is the FOMC’s plan to key the Funds rate at a restrictive level for all of 2023. When the economy shows more signs of slowing in the second quarter, the FOMC is likely to keep the Funds rate steady and provide no indication that it plans to lower it. That resolve can be expected to impact financial markets in coming months.

Dollar

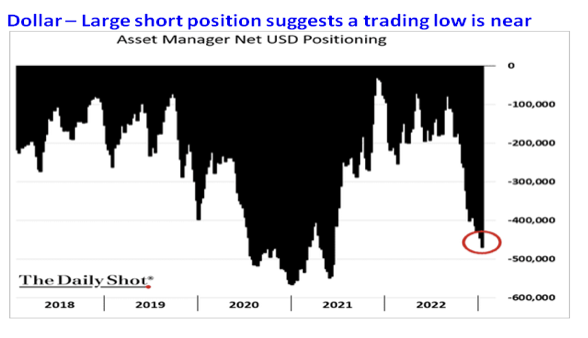

The Dollar is likely to provide a guide to how financial markets perform in 2023. As the Dollar topped in October, other major markets bottomed and rallied as the Dollar declined. From the high in October, the Dollar has declined more than 11%, which provide a big lift for Gold, and strong support for the stock market and Treasury bonds. A reversal higher in the Dollar would cause a retracement of the rallies other markets have experienced since October.

Sentiment toward the Dollar has become negative with traders establishing a large short position in the Dollar and long positions in the other major currencies. Extreme positioning in any market often leads to a counter move as traders are forced to reverse their positions. For instance, a large short position in the first half of 2021 indicated that sentiment toward the Dollar had become quite negative, and the chart pattern helped identify the low.

In 2021 the expected bottom in the Dollar was discussed repeatedly in the Weekly Technical Review in May and June. This excerpt is from the June 7 WTR. “The big news is that the coming low may be the end of the correction that began after the Dollar peaked in January 2017 at 103.82. Wave A of the correction lasted from January 2017 until the Dollar bottomed at 88.25 in February 2018. Wave B of the correction carried the Dollar up to its high in March 2020, with Wave C now near completion. The price pattern suggests the Dollar has the potential to rally above 100.00 in the next 12 months.” After bottoming near 90.00 in June 2021, the Dollar rallied above 100.00 in April 2022.

Currently, the size of the short position currently isn’t as large as in 2021, but it is the second largest in the last 5 years. The Dollar rallied from the low of 89.50 in 2021 to 114.77 in October 2022. The 50% retracement of that rally is 102.10, which is where the Dollar has been trading in the last three weeks. The chart pattern suggests the Dollar is near a trading low as noted in recent WTR’s. “After topping in late September at 114.78, the Dollar appears to be completing Wave 5 down.” Once a market completes a 5 wave move up or down, a counter trend becomes probable. The Dollar is expected to rally to 106.50 – 108.00 in coming months.

Treasury Yields

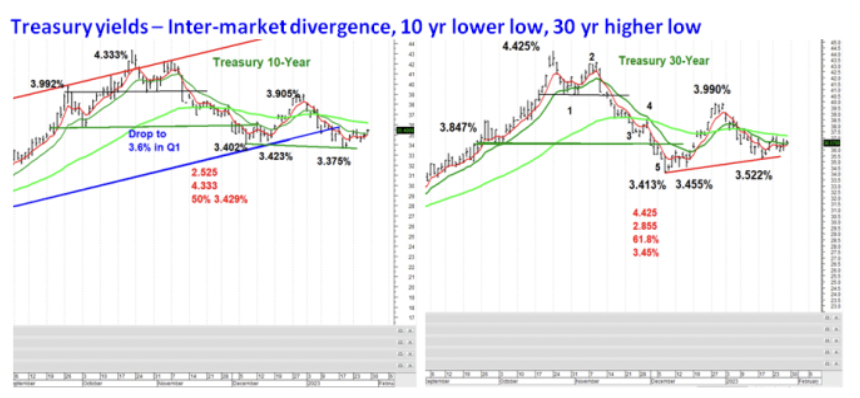

In the November 1 Macro Tides I discussed why I thought Treasury yields were likely to decline based on a decline in inflation. “As I have discussed for months, the take away values for the headline CPI from Q4 in 2021 and Q1 in 2022 are so large that inflation is virtually guaranteed to fall in the next six months. The takeaway values for the headline CPI from October through March are -4.84%. If the monthly increase for is +0.4% in October, the headline CPI could fall from 8.2% to 7.8% (-.87 from October 2021 + 0.4% October 2022), when it is reported on November 10. A 7 handle headline will be attention grabbing. If the CPI drops from 8.2% in September to 7.5% in November, the FOMC will increase the Funds rate by 0.50% at the December 14 meeting, after hiking by 0.75% at the November 2 meeting.” The bond market was deeply oversold which provided a technical reason to expect Treasury yields to fall. “As of October 21, Treasury bond prices had just declined for 12 consecutive weeks for the first time since 1977. If the Dollar stops going up, or better yet falls, Central Banks won’t have to continue to sell Treasury debt. The expectation is that the 10-year Treasury yield could fall to 3.50% at a minimum, and possibly to near 3.0% in the first quarter of 2023.” The 10-year Treasury yield dropped to 3.402% in early December and 3.373% in January.

Since mid October the headline CPI has fallen from 8.2% to 6.5% in December. The sharp decline in inflation led to a big drop in the 10-year Treasury yield, which has plunged from 4.33% on October 21 to 3.402% on December 2. After the larger than expected fall in the CPI for December, the 10-year Treasury yield dipped to 3.373% on January 18. With such good inflation news, one would have expected the 30-year Treasury yield to follow the same pattern. However, the 30-year Treasury yield only fell to 3.522% on January 18, comfortably above the lows in December of 3.413% and 3.455%. The inability of the 30-year yield to confirm the lower low in the 10-year created a negative inter market divergence. Inter market divergences often develop right before a change in trend, and has helped me identify trend changes in the past. In this case, the negative divergence suggests that Treasury yields are likely to rise in coming months. Since the 30-year is weaker, the 30-year yield is expected to rise to 3.99%. The 10-year may only increase to 3.80% - 3.85%.

Stocks

Wall Street wants to believe that the economy will experience a soft landing, the fast and furious decline in inflation will continue, and the FOMC will lower the Funds rate in the second half of 2023, even though the Unemployment Rate is near a 50 year low. There are problems with these assumptions. Three reliable indicators have signaled that a recession is likely in the second half of 2023, and the Unemployment Rate will increase before the end of 2023. If the FOMC increases the Funds rate to 5.0% as indicated, the impact on the economy from all of the rate increases will be more significant.

Although the headline CPI for January is going to drop from 6.5%, the month to month change for January will increase from a decline of -.1% in November to an increase of 0.3% or more due to higher energy prices. If correct it will take away some of Wall Street’s conviction that inflation will continue to drop like a stone in a pool.After June the takeaway values from 2022 are much lower than they were from October 2021 through March 2022 (-4.84%). In the first quarter the take away values from 2022 are -2.69% and -2.62% in the second quarter. This is why the headline CPI is likely to drop below 3.2% in June, and why the easing of labor market tightness is so important. In the third quarter the take away values from 2022 are only -0.51% and -0.40% in the fourth quarter. After June 2023, additional declines in the headline CPI will be dependent on the change in the monthly CPI. If the monthly change in the CPI from July through December is 0.2%, the headline CPI will rise by 0.3%. This analysis suggests that inflation may prove sticky in the second half of 2023, which could bolster the FOMC’s resolve to hold the Funds rate at a restrictive level to the end of 2023 until labor market tightness declines.

Wall Street may be wrong on what is expected in 2023, but in the near term the ‘soft landing’ narrative could hold the stock market up for awhile. The S&P 500 declined from January 4 to October 13, 2022 or 281 days. A rally that consumes 50% of the time of the initial decline from the low on October 12 would last until March 3. The S&P 500 has the potential to rally to 4130 – 4175 by late February or early March.

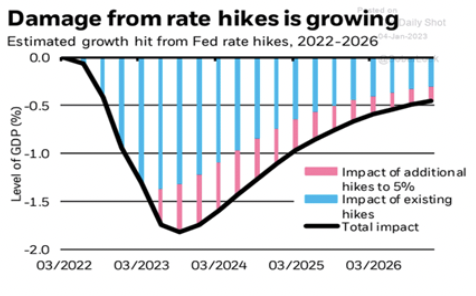

The peak drag from the FOMC rate hikes in 2022 will develop in the second half of 2023 and first half of 2024. If the FOMC increases the Funds rate to 5.1%, the intensity of the slowing will increase too. The S&P 500 is expected to retest the October low of 3491 around mid-year, as the economy slows and the FOMC doesn’t indicate that a quick pivot is coming in response to economic weakness.

Gold

Longer term the odds have increased that Gold recorded an important low in September and completed a 2 year (A down, B up, C down) correction, after topping at $2070 in August 2020. This pattern suggests the rally from $1616 is Wave 1 of a 5 Wave rally that will lift Gold to an all time high before the end of 2024. The nature of the upcoming pullback could provide additional support, if the correction is choppy and corrective. (i.e. a-b-c versus a 5 wave decline)

The rally in Gold has mirrored the decline in the Dollar. Gold is now overbought, sentiment which was universally negative in October, has become much more positive. The shift in sentiment has been driven by the rally in Gold and the belief that the FOMC is pretty much done with tightening monetary policy. That assumption is incorrect. There will be a Wave 2 correction within the 5 wave rally to new highs that should cause a decent pullback in Gold.

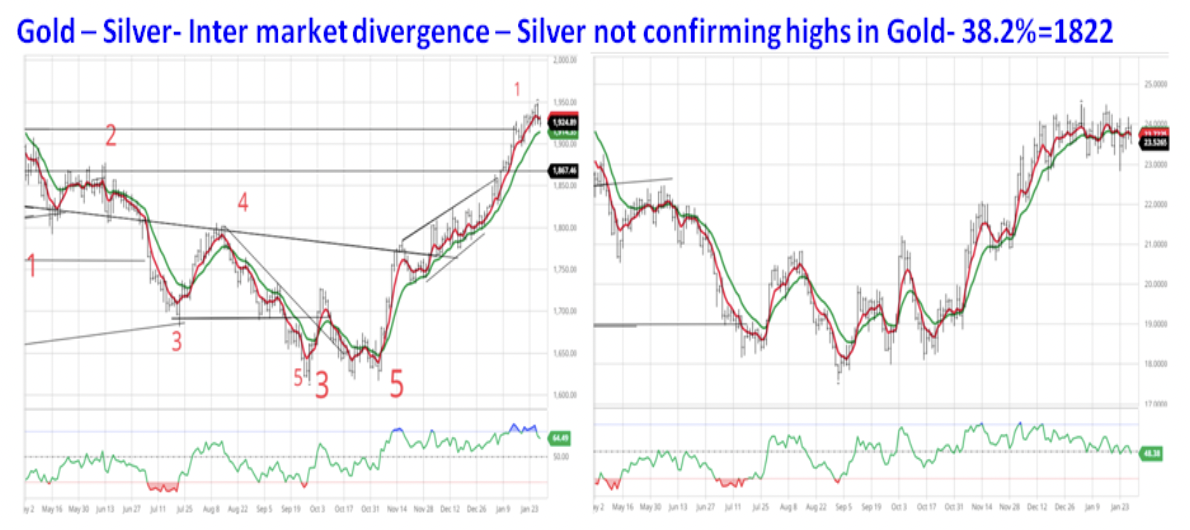

An inter market divergence has also developed between Gold and Silver in recent weeks. Gold has rallied from $1833 on January 5 (5.7%), while Silver is up less than 1%. This suggests the strength in Gold is nearing an end, unless Silver explodes higher soon. Gold has rallied $333 since the low of $1616 in September, and a 38.2% retracement of the rally would target a pullback to $1822, and target of $1782, if Gold retraces 50% of the move. Since a rally to a new all time high is not guaranteed, reducing exposure makes sense.

China

Since China’s vaccine was not effective, China used a zero tolerance policy to limit the spread of COVID. This has resulted in repeated shutdowns in many parts of China and a loss of economic activity. After almost 3 years of isolation and autocratic government, public support for lockdowns evaporated and public demonstrations against the zero tolerance policy became widespread. With the economic impact depressing the economy, President Xi decided the continuation of the zero tolerance policy was untenable. In October, Dr. Liang Wannian, the architect of zero-COVID policy, said China "cannot tolerate" a wave of mass infections. In December he said, "The virus is much more mild now." China has admitted to just 5,273 deaths from COVID in a population of 1.4 billion. After ending the zero tolerance policy on December 7, China says the 7 day average of deaths is less than 5. Reports and satellite imagery suggests a different story. Crematoriums are running 24 hours a day every day of the week. The wait times can stretch up to 2 weeks.

The impact from lifting the zero COVID policy is having an outsized spread because the zero COVID policy limited the development of natural immunity on top of a weak vaccine. The policy was changed to improve the economy and end widespread demonstrations. But from President Xi’s perspective, allowing COVID to spread and cause a significant increase in illness and death is another way for him to show the people of China that his way was best. This is a less than subtle way of reasserting Xi’s authority but effective.

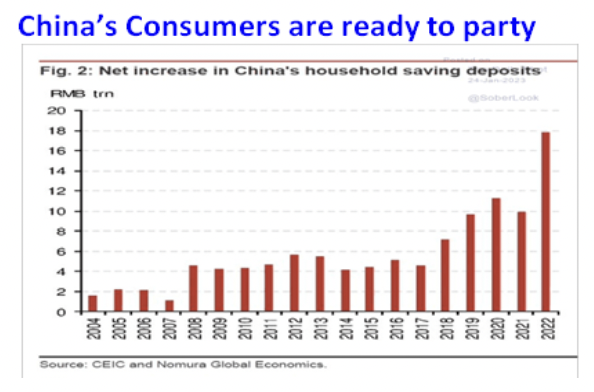

Household savings soared in 2022 as consumers weren’t allowed to go outside and spend. Just as Americans celebrated their freedom after the lockdowns ended in the US by spending up a storm, Chinese consumers will do the same after the current wave of COVID runs its course. It may not happen overnight, but economic growth will be stronger as 2023 progresses. This will give the global economy a lift and also boost global demand for commodities. This may be why the Bloomberg Commodity Index is setting up for a rally as discussed.

European Union

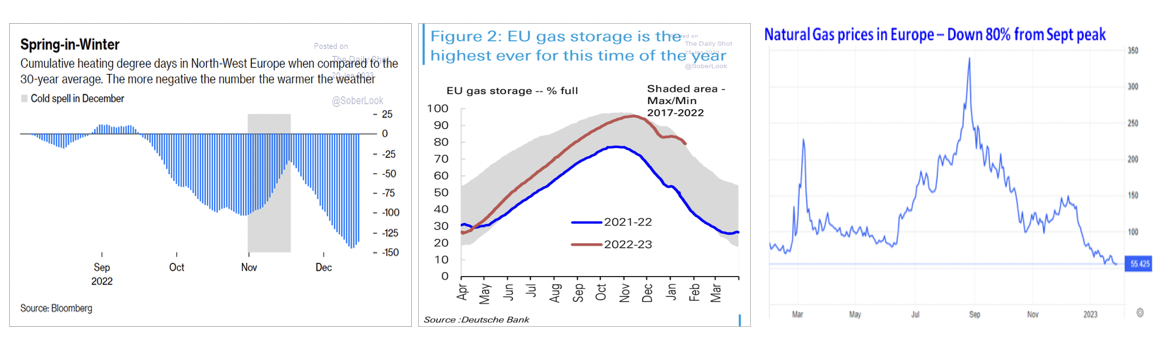

Mother Nature has been kind to Europe. Winter has been unusually warmer than normal, so the amount of Natural Gas in storage is the highest in history. Surplus supply has led to an 80% decline in the cost of natural gas since it peaked in September. This has been a boon for industries that use Nat Gas and for consumers who were bracing for high prices and the risk of shortages. Consumer confidence has improved and business activity has picked up.

On December 21 the ECB increased it policy rate by 0.50% to 2.50% and indicated that additional hikes would follow. EU banks increased their lending standards in the third quarter just as US banks did. Although the economic outlook is less dire for the EU, a recession is still likely. The modest improvement in EU growth from bad to less bad will depress global growth less than it may have if energy prices hadn’t fallen so much.

Global Economy

The rebound in China and a smaller contraction in the European Union will moderate the slowdown in the global economy. On January 30 the International Monetary Fund (IMP) increased its estimate for global GDP growth to 2.9% from 2.7% in October. That improvement will still mark a slowdown from 2022’s growth rate of 3.4% and 6.0% in 2021. The World Bank is less optimistic and only expects the global economy to grow by 1.7%. The sharp slowdown will be broad with 95% of advanced economies growing slower in 2023 than in 2022, and slowing growth in 70% of Emerging Market and Developing countries.

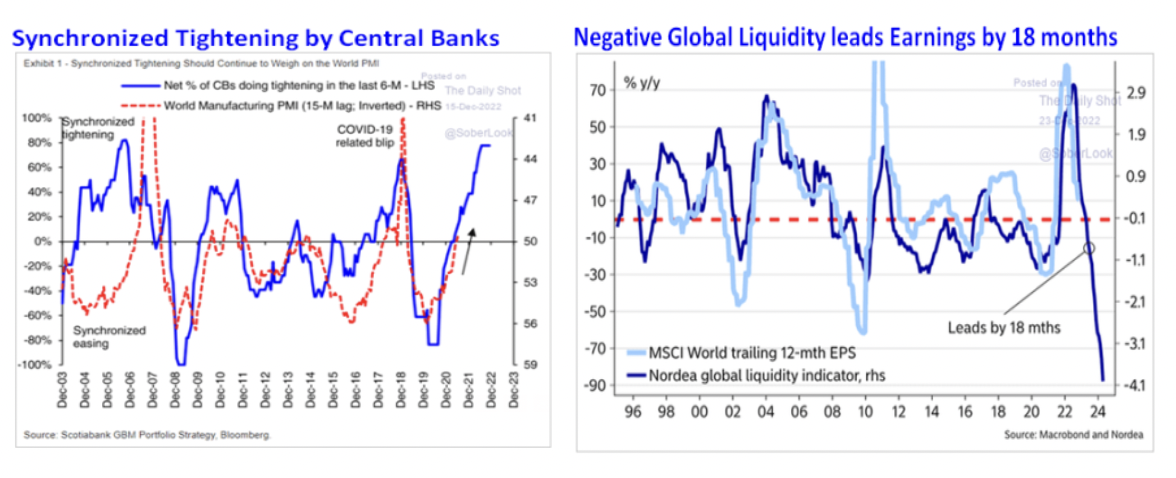

The World PMI Index shows that changes in global central bank monetary policy impacts economic activity for the following 15 months. The synchronized tightening of monetary policy by more than 80% of central banks in 2022 will continue to slow global growth progressively in 2023 and in early 2024. The synchronized tightening of monetary policy has caused Global liquidity to become more negative than at any time in the last 26 years. Some of the decline is due to annual rate of change calculations, so the magnitude of the drop is likely exaggerated. Nonetheless, the overall message is clear. The global economy will slow more in the next 18 months and cause a decline in corporate earnings. The 500 companies in the S&P derive 40% of their revenue from international sales. According to Global X, technology firms get more than 50% of their revenue from international sales, so the global slowing will hurt them more.

Jim Welsh

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Live Virtual Event: Join Now

Upcoming Virtual Events View All