Last Friday, after a demanding week tracking a bevy of risks related to the closure of Silicon Valley Bank (SVB), I needed to clear my mind. I waited for markets to close, then set out for a long run. The weather was fine, and tuning into non-financial podcasts was refreshing. Still, I couldn’t help but anxiously check my phone for news alerts.

Fortunately, the weekend brought no further bad news from the U.S. banking system. But even if the acute phase of this crisis is short-lived, uncertainty will persist. The failure of Silicon Valley Bank and Signature Bank could weigh on financial and economic activity for a long time to come.

The business of banking is conceptually simple. Long ago, bankers joked of the “3-6-3” rule: Pay 3% on deposits, charge 6% on loans, and take your clients out for a 3:00 tee time. But if it was ever really that easy, those days are long in the past. Interest rate surges of the late 1970s proved costly; some institutions took on extra risk to offset their rising funding costs, but often found more trouble than relief, spurring the savings and loan crisis. Nearly 3,000 American financial institutions failed between 1980 and 1994.

The decades-long run of falling interest rates that followed, along with greater competition from private investors, reduced bank margins. Some strategies aimed at arresting the decline in profits created kindling for the global financial crisis of 2008.

Given the importance of the sector, banks are subject to a wide range of rules and review by a bevy of regulatory bodies. Many have therefore wondered how a firm the size of SVB could have failed. We have since learned that the Federal Reserve issued the bank serial findings of risk management deficiencies. But the firm apparently did not heed the warnings, and supervisors may not have pressed the issues aggressively enough.

While SVB would have been subject to stricter annual stress testing if not for a 2018 moderation of the Dodd-Frank Act, it is not clear that those tests would have changed SVB’s decisions. Further, existing regulations and disclosures should have been sufficient to detect the potential for trouble. SVB’s demise was not entirely a regulatory failure, but that fact will not head off calls for new regulations on the banking industry in the months ahead.

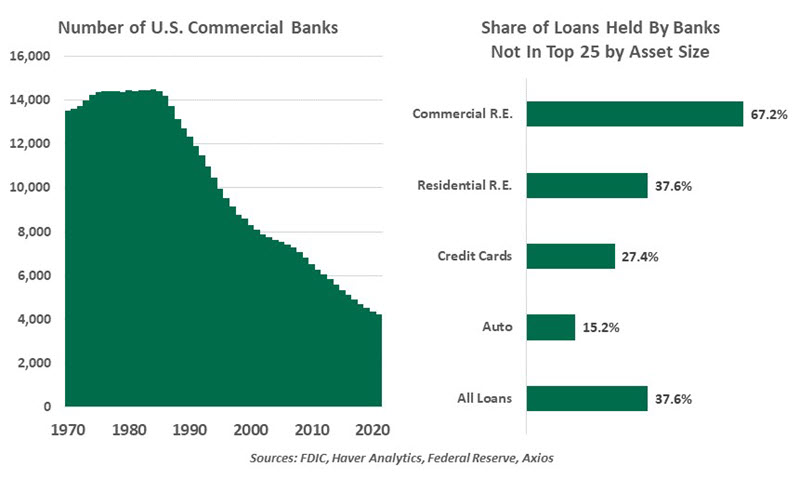

Given the costs of compliance and other profit pressures, the banking industry has undergone a great deal of consolidation. From a peak of over 14,000 FDIC-insured institutions in the early 1980s, the number of U.S. banks has fallen to 4,178 as of 2022. Those four thousand banks are not all major money centers. The majority of them are relatively small by asset size but serve vital roles in their communities and account for large fractions of certain types of credit extension. They are part of the nation’s economic backbone.

Deposit flight from smaller banks increases the risk of another SVB-style panic.

As such, news of deposits shifting away from smaller banks into the larger ones has been unsettling. Clients’ motivation is understandable: SVB showed that less-diversified banks may not be the most secure. Depositors may perceive larger banks are at lower risk of bank runs and crises of confidence. However, small deposit shifts can snowball into panicked evacuations, depriving smaller banks of the liquidity that they (and their borrowing bases) rely on.

SVB also cast light upon the state of insurance for U.S. depositors. Since 2010, all deposit accounts have a $250,000 guarantee from the Federal Deposit Insurance Corporation. This amount is ample for most households but rather small for many business and institutional accounts. In general, businesses keep at least three months of operating expenses in cash, which can reach into the millions even for small businesses. The potential for business disruption when these funds become unavailable fueled high anxiety within the deposit base of SVB.

Deposit insurance is not free. Banks pay a premium to the FDIC of up to 0.42% on their deposits, depending on the bank’s size and condition. There may be some opportunity to enhance the risk-based pricing of deposit insurance, but even the most conservatively-managed institutions would need to absorb a higher insurance cost if coverage is extended to all deposits. Treasury Secretary Janet Yellen’s enthusiasm for this strategy diminished this week, but the issue might certainly resurface.

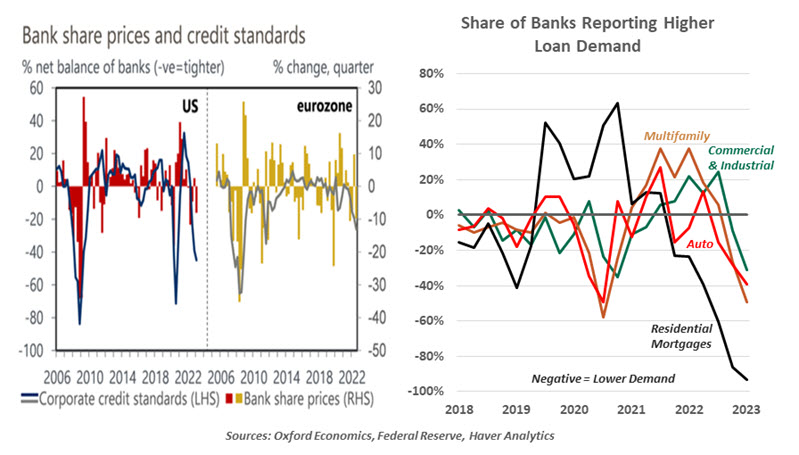

The effects of tighter credit conditions are difficult to measure.

Given all these challenges, the Fed walked into a difficult setup this week. Their “trilemma” of managing stability, inflation and employment requires delicate balance. The Federal Open Market Committee (FOMC) hiked the Fed Funds Rate by another 25 basis points, while emphasizing that “the U.S. banking system is sound and resilient.” The accompanying statement and Summary of Economic Projections (SEP) set expectations for “some additional policy firming;” the median FOMC member forecast just one more hike this year, then holding into 2024.

The FOMC statement and Chair Powell’s press conference repeated an expectation that recent events will tighten credit conditions. A higher cost and lower availability of credit will slow the economy, functioning like an interest rate hike. History shows that risk officers respond to pressure by tightening lending standards; however, the tightening was already underway before SVB. And evidence from the Fed’s Senior Loan Officer Opinion Survey suggests that lending demand was already in decline this year. Tighter bank standards may not have much of a dampening effect on economic activity.

The SEP offered some hope that a soft landing remains possible: most FOMC members foresee positive (but slow) growth with cooling (but still high) inflation, and only a modest rise in unemployment. But the events surrounding SVB show how quickly fortunes can change. Thus far, contagion has been contained, but systemic risk may still be accumulating. Though I am working on distance training, I may find it impossible to run from an incipient financial crisis.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

© Northern Trust

Read more commentaries by Northern Trust