In the aftermath of the collapse of Silicon Valley Bank (SVB), Credit Suisse (CS) swiftly became a point of concern last week. A resolution has been put into place, but the situation could reverberate in the coming weeks and months.

While SVB’s failure put a spotlight on the banking sector, CS had few similarities to its American counterpart. The bank’s downfall came swiftly, but the decay was years in the making. Once a stalwart of the financial system that was instrumental in putting Switzerland on the map of international finance, CS had become the problem child of European banking in recent years. Multiple scandals, losses, management shake-ups and unsuccessful restructurings took their toll.

Among other episodes, CS’ chief executive Tidjane Thiam was ousted over corporate espionage in 2020. In June 2022, CS was found guilty of helping a Bulgarian cocaine trafficking gang launder money. The bank reported a loss of nearly $8 billion in the fiscal year 2022 amid a major restructuring process, its biggest since the global financial crisis.

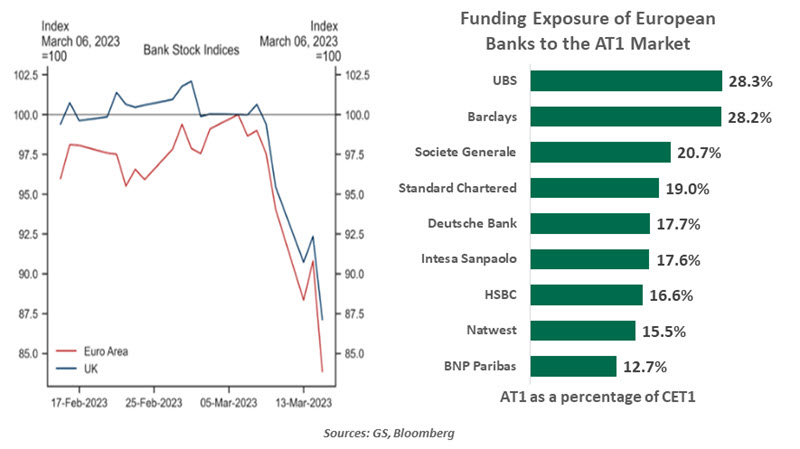

The sell-off in Credit Suisse’s shares, initially triggered by fears over a global banking crisis, only intensified after its largest shareholder refused to invest more in the lender. The circumstances surrounding CS were unique, and it was not covered by the same supervisor as other leading European intermediaries. Nonetheless, broad concern among investors caused bank share prices to plunge and put their bond prices under pressure.

Before the fall, CS became the first major institution to receive an emergency liquidity line since the 2008 financial crisis. But even last week’s $54 billion financing backstop by the Swiss National Bank couldn’t restore confidence in the troubled firm. Ultimately, in a move orchestrated by Swiss authorities to avert a banking crisis, the 167-year-old institution with a $574 billion balance sheet was sold to its bigger domestic rival UBS for $3.2 billion.

The deal appears to have prevented the situation from spiraling out of control, but not without denting investor confidence. In bankruptcies, equity investments are typically repaid secondarily to bonds. In this case, the rudest shock came for the bondholders as stockholders emerged above additional tier 1 (AT1) bondholders in the pecking order. The deal triggered a “complete write-down” of these bonds, making notionally $17 billion of bonds worthless.

This is the largest AT1 loss ever and the first since the 2017 collapse of Spain’s Banco Popular Español SA. Similarly to the current case, the Spanish bank was sold to its domestic rival Santander for the token value of one euro.

The AT1 bonds are also referred to as contingent convertibles or CoCos. AT1s offer higher interest rates than regular bonds, since they can be converted to equity or written down if the institution’s capital levels fall below requirements. These were introduced after the 2008 financial crisis to transfer banking risk away from taxpayers to bondholders.

Over the years, European authorities have encouraged financial institutions to issue these debt instruments and are considered part of banks’ regulatory capital. Higher yields over the past decade, when benchmark interest rates were low, contributed to the popularity of AT1 bonds, now a $275 billion market. On average across the 16 biggest European banks, AT1 bonds account for about 16% of their highest quality regulatory capital.

Credit conditions could tighten notably in the aftermath of this turmoil, weighing on activity

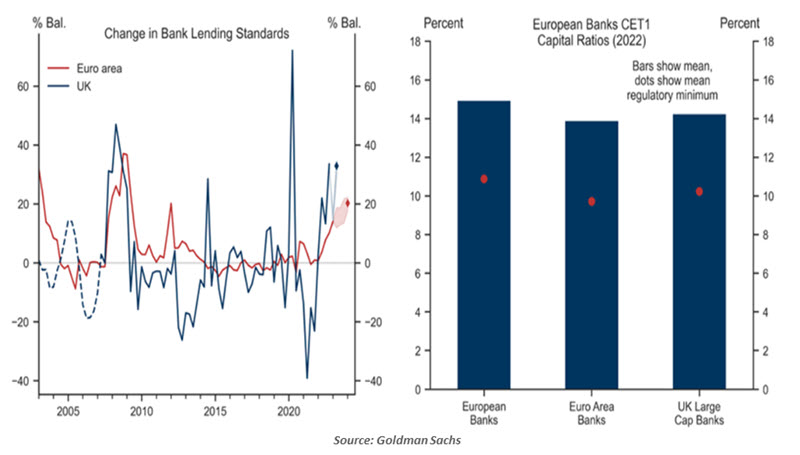

Euro area authorities were quick to note that contingent convertible debt might be handled differently in the resolution of a bank under its authority, but investors may not appreciate the nuance. The complete write-off of AT1s by Swiss authorities is likely to hurt investor appetite and make the bonds more expensive to issue. This, along with the pressure that all European bank stocks have been under, may squeeze banks’ ability to make new loans.

The European economy is more sensitive to bank lending than is the case in the U.S., as European businesses still rely mostly on bank loans to fund their growth. Lending standards were already tightening in response to restrictive monetary policy and now could tighten further. Banks could face higher funding costs along with additional regulation. All of this will reduce the flow of credit and add to the risk of a recession.

Despite fears of contagion, both the European Central Bank (ECB) and the Bank of England (BoE) continued their fight against inflation by hiking their benchmark interest rates. Inflation in Europe is stubbornly high, and its banking sector is more resilient than in the previous crisis. European banks have strong capital and liquidity positions with improving profitability. Non-performing loans, long the weak spot of European banks, have fallen steadily to below 2% of total loans in the last eight years.

But the turmoil has led traders to scale back expectations for further rate hikes from the ECB and the BoE. Higher interest rates boost the interest income of financial institutions but also adversely impact the value of banks’ holdings of government bonds, mortgages and other debt instruments. The ECB’s head of supervision Andrea Enria cautioned last November that “banks should not disregard the impact that rising rates typically have on the present value of their net worth.”

As one of 30 global systemically important banks, the risk of Credit Suisse's collapse sending ripples through the broader financial system and having implications to the broader economy cannot be ignored. Banking or financial crises not only lead to tightening credit conditions or negative wealth effects, but also impair long-term growth prospects. According to various academic studies, past banking crises on average lowered the long-term level of gross domestic product by 5%-10%.

Under stress, trust and confidence are as important as capital and liquidity ratios for banks.

Banking is about confidence and trust; any crack can trigger a run and a potentially a collapse of institutions. Credit Suisse had healthy capital and liquidity ratios, both only slightly below the eurozone average in 2022. In a bank run, depositors do not apply clear-headed analysis of ratios or technical measures.

The current banking turmoil is unlikely to snowball into a full blown financial crisis. Nevertheless, the episode should serve as a wake-up call to all banks, including those with strong capital and liquidity. Mahatma Gandhi once said: “It is weakness which breeds fear, and fear breeds distrust.”

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.