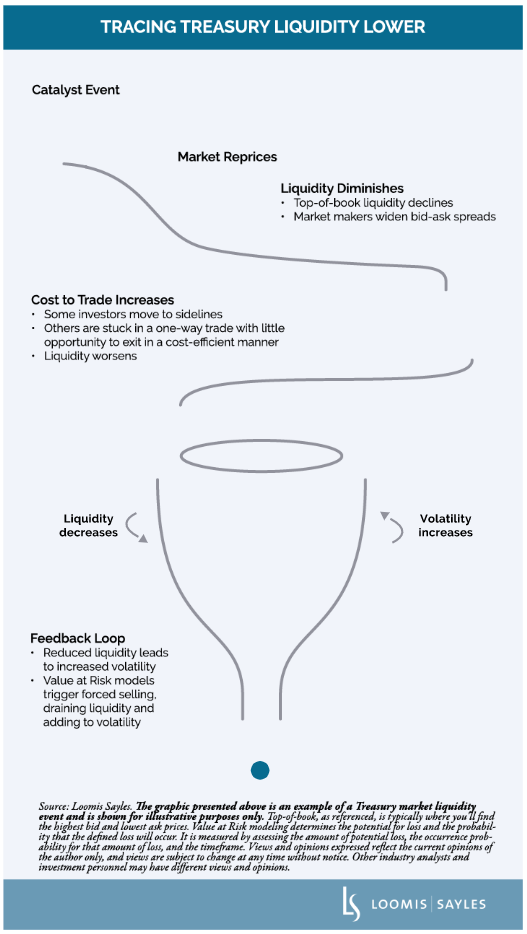

Tracing Treasury Liquidity Lower: Once the Ball Starts Rolling, It’s Hard To Stop

It’s been—to put it mildly—an interesting week in the US Treasury market. The front end of the curve whipsawed dramatically, with the two-year yield plunging 109 basis points in three days of trading (a move not seen since 1987)[i] as markets questioned the stability of the banking system. Many leveraged players had been positioned for higher fed funds rates. When the market shifted and began to price in rate cuts later this year, many of those participants rushed for the door at the same time, triggering the huge moves.

Volatility and liquidity tend to be inversely correlated, so these market vacillations have impaired Treasury liquidity. It’s an important dynamic to understand, as we expect outsized moves in Treasurys and challenging liquidity conditions to persist until markets are confident the banking system is stable. Here, we’ll break down an example of how volatility spikes can drain liquidity from the system and why once the ball starts rolling, it can be hard to stop.