State governments tend to boast strong creditworthiness. They have a multitude of revenue streams, the ability to adjust budgets on the fly, and tend to have broad economies. These factors contribute to the sector’s generally high credit quality, with only seven states rated below AA. However, we expect the slowing economy to reveal imbalances that could affect credit quality and lead to diverging performance within the sector. We’re watching three factors in particular: income tax exposure, cash cushions relative to historical volatility, and the level of aggregate long-term liabilities.

1. Exposure to income tax revenues

Income tax revenues tend to be more volatile than other types of tax revenues. California and New York often are cited as especially exposed to income taxes because of their reliance on income tax (as measured by income tax’s percentage of total state revenues). However, tax rates are also part of the equation. States that have a high reliance on income tax and high top marginal tax rates, such as California, New Jersey and New York, are generally the most susceptible to the income volatility inherent in high earners’ bonuses and capital gains. For this reason, we think those states are at greater risk in a downturn.

2. Liquidity cushions

We believe cash and reserves, which typically provide a cushion throughout an economic cycle, become even more important in a downturn when revenues tend to fall short of expectations and expenditures can exceed expectations. In aggregate, states began fiscal year 2023[i] with cash cushions well above pre-Great Recession levels (see graph).

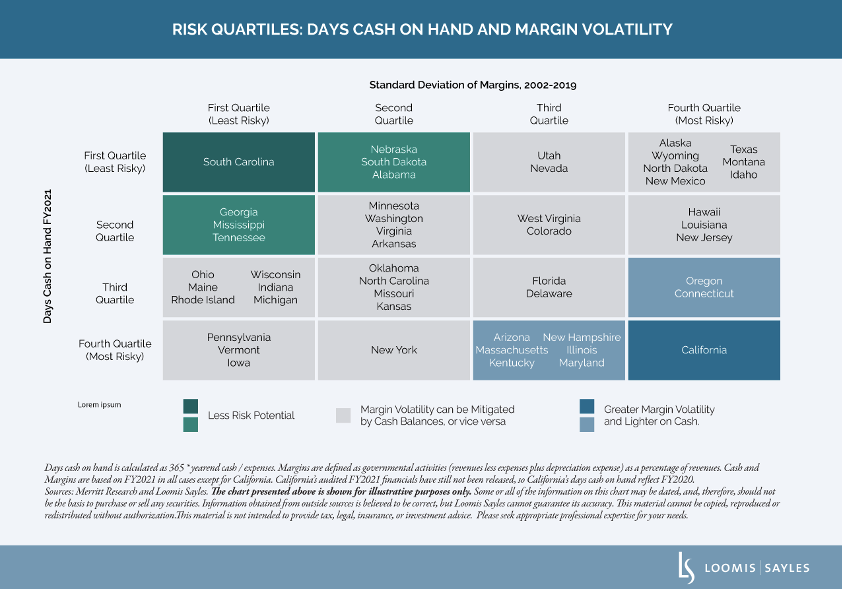

Although a liquidity cushion alone can be informative, overlaying margin volatility (changes in net revenue as a percentage of total revenue) can give us a sense of how important cash balances may be to a particular state. We consider net revenues because states have some flexibility on expenditures when revenues fluctuate. States with higher margin volatility may need a larger cash cushion to dampen the effects of large revenue swings. Conversely, states with more stable margins may have less of a reason to carry a big cash cushion.

The table below illustrates which states tend to maintain balanced margins and how their cash levels stack up against their peers.

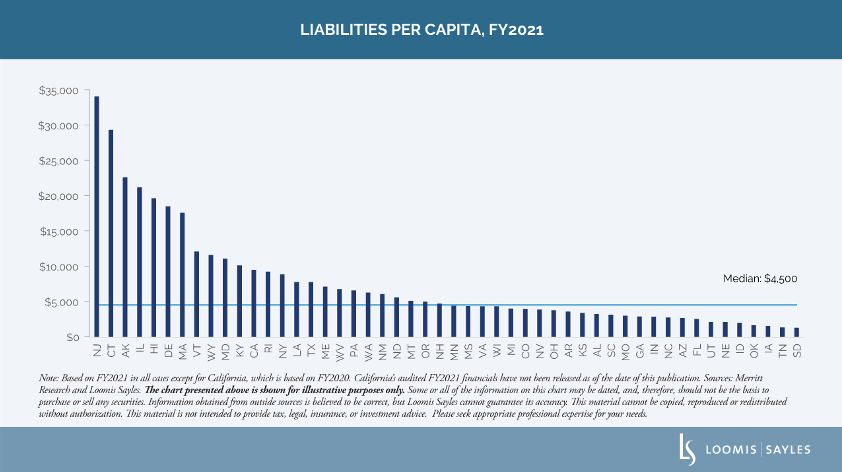

3. Long-term liability burden

Leverage tends to come to the forefront when the economy slows. In a growing economy, highly levered states generally have the capacity to handle their obligations. But they may have difficulty meeting their obligations in a slowing or shrinking economy. New Jersey, Connecticut, and Illinois are among the most highly levered states.

States may be in peak condition, but risks loom ahead

In our view, states generally entered the current slowdown in peak condition on the back of surging revenues, strong reserves, federal stimulus, and outsized returns on pension assets in FY2021.[ii] However, this is not a time to be complacent about the state government sector. We believe a slowing economy will apply downward pressure on revenues at a time when states have widespread plans for increased spending. Given the factors discussed above, we believe some states will weather the pressure better than others. In our view, careful credit research will be critical for investors in the months ahead.

MALR030645

Markets are extremely fluid and change frequently.

This material is not intended to provide tax, legal, insurance, or investment advice. Please seek appropriate professional expertise for your needs.

This blog post is provided for informational purposes only and should not be construed as investment advice. Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors only and do not necessarily reflect the views of Loomis, Sayles & Company, L.P. This information is subject to change at any time without notice. Information obtained from outside sources is believed to be correct, but Loomis Sayles cannot guarantee its accuracy.

[i] Most states’ fiscal year 2022 ended on June 30, 2022.

[ii] https://crr.bc.edu/wp-content/uploads/2022/11/IB_22-20.pdf).

© Loomis, Sayles & Co.

Read more commentaries by Loomis, Sayles & Co.