The Case for Low-Volatility, High-Dividend Equities

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsGiven market uncertainty and the risk of a US recession, is now the time for defensive stocks? Making a case for low-volatility, high-dividend equities with Franklin Templeton Investment Solutions’ Vaneet Chadha and Michael LaBella.

After a horrendous 2022, equity markets had a rocky—but positive—first quarter, even though inflation has proven to be sticky, central banks are still raising interest rates, and lending standards have tightened. This has many investors questioning: “Is now the time to be taking risk?” Economic uncertainty is likely to continue driving volatility in 2023, with risk skewed toward the downside. We think that reducing exposure to risk assets while increasing exposure to defensive equities with lower volatility and higher potential dividends may help weather continued market turbulence.

The 2023 market narrative

We expect this year’s market narrative to focus on earnings as investors look for directional insights. As our team has written about previously, bank lending has tightened—and is tightening—across sectors. In our view, recession risk is therefore increasing. Of particular concern is the potential for a negative feedback loop—tighter credit conditions, characterized by an inability to get loans or a higher cost of financing, could lead to less cash on hand for companies and consumers, which could then lead to lower deposits (assets) at the banks, contributing to even tighter credit conditions.

Meanwhile, earnings growth has slowed to the point where last quarter, they declined as profit margins were getting squeezed.

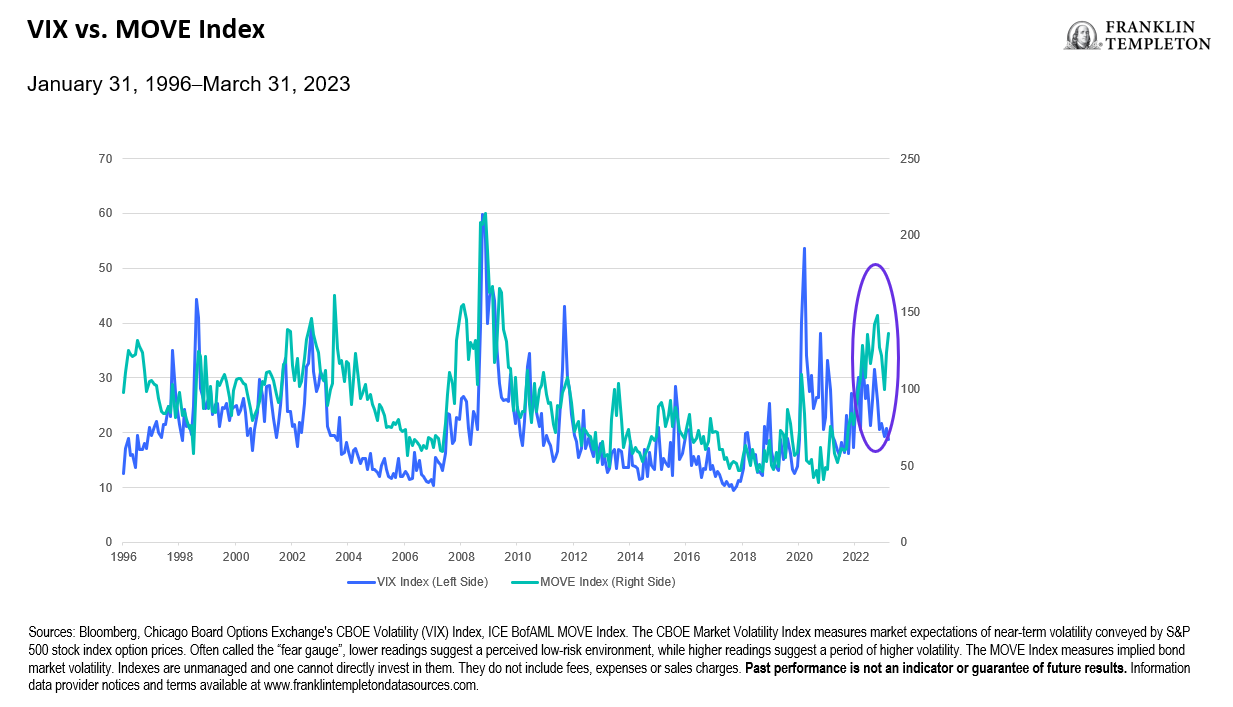

Equities have been significantly more volatile in the past few years than in the past decade. However, in recent months, equity volatility has subsided, while fixed income volatility has increased. We believe this is noteworthy, as these two measures have historically tracked each other relatively closely (see Exhibit 1). This divergence has us wondering what one market is seeing or expecting that the other is not. If volatility is a measure of uncertainty, the recent spike seen in the bond market more closely aligns with our outlook on market risk. We expect volatility to remain high for the foreseeable future, with meaningful recession risk; we see the odds of a US recession as more likely than not in the next 12 months as our base case.1 Though the market is pricing in an interest rate cut from the Federal Reserve (Fed) by the end of 2023,2 which is supportive for equities, the stickiness of inflation may limit the Fed’s ability ease monetary conditions as significantly as in the past. This increases the risks for 2023. Time will tell whether earnings lead stocks in 2023, or if a Fed “pivot” will dominate the narrative.

Exhibit 1: Volatility in Treasuries and Equities Has Diverged (right click to enlarge chart)

Why low volatility and high dividends

Successfully timing markets is difficult, and maintaining prudent equity exposure is important. It might be difficult for investors to maintain their equity allocations when facing the unknowns discussed above. But those with a strategic allocation to equities are usually looking to grow their assets over the long term, and we believe stocks are instrumental for most in achieving that goal.

Exhibit 2: The Effect of Not Being Invested When the Market Had its Best Days (right click to enlarge chart)

Over time, stocks exhibiting low volatility provide equity-like returns with less volatility and lower drawdowns than market capitalization-weighted equity benchmarks. Furthermore, income is an important component of total return; should stock prices fall, but dividends stay consistent, those higher yields could provide meaningful defense. Lastly, when borrowing rates are high, current income becomes appealing to those who cannot wait for a stock to potentially appreciate.

Exhibit 3: Low-Volatility/High-Dividend Stocks Have Outperformed in Down Markets (right click to enlarge chart)

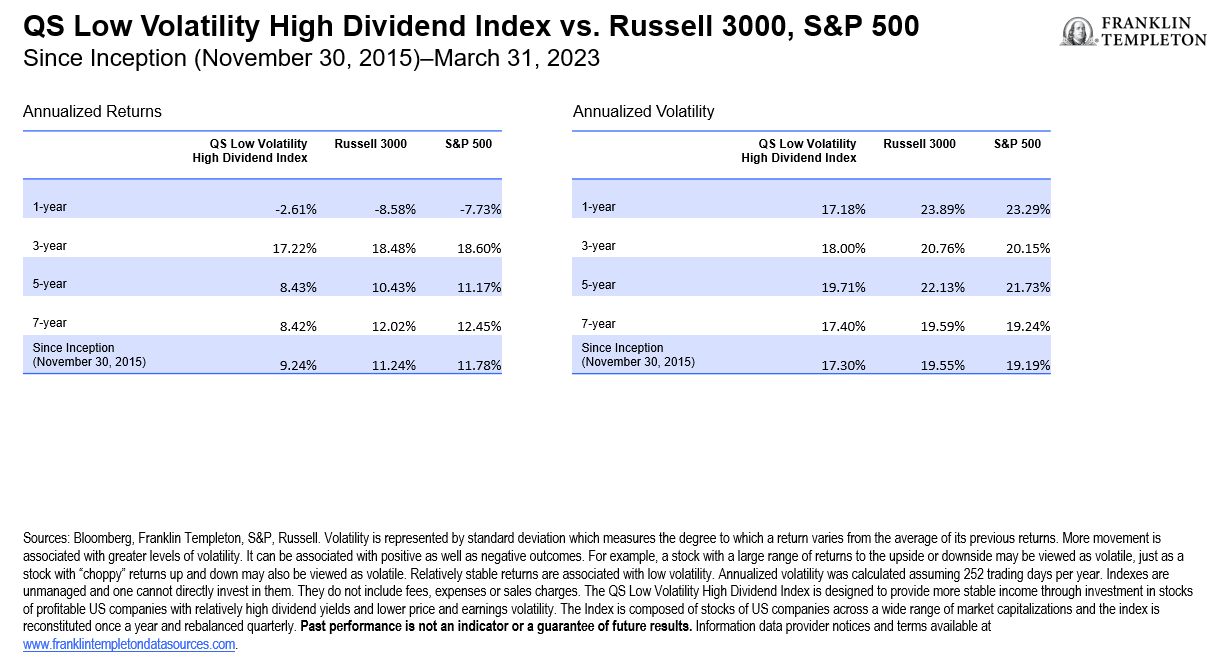

Exhibit 4: Annualized Return and Volatility Profile (right click to enlarge chart)

There are a few leading theories that explain how this investment factor works. We believe that part of the reason is behavioral; investors may chase returns when times are good by overweighting high-risk stocks in the hopes that they are big winners for their portfolios, leaving defensive stocks underappreciated. Over time, this leads to strong returns of the defensive stocks as prices revert to a more accurate portrayal of company fundamentals.

While the low-volatility factor is a helpful screen in finding stocks that have a “smoother ride,” it does not offer a direct fundamental view of the underlying company. However, the high-dividend factor does provide some insight. We have found that companies with a history of sustainable dividend payments tend to be well managed and financially sound.

In today’s economy, we think tighter lending standards and compressed margins will cause equity investors to be even more discerning about their potential equity investments. We believe that combining companies with high dividends—and the earnings to back them up—with those that have exhibited low volatility over time can be a useful way to lower the risk of an investor’s equity sleeve. At the same time, this approach maintains equity exposure and can provide the additional benefit of income potential.

WHAT ARE THE RISKS?

All investments involve risks, including the possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. The positioning of a specific portfolio may differ from the information presented herein due to various factors, including, but not limited to, allocations from the core portfolio and specific investment objectives, guidelines, strategy and restrictions of a portfolio.

Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions.

Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline. Investments in lower-rated bonds include higher risk of default and loss of principal. Changes in the credit rating of a bond, or in the credit rating or financial strength of a bond’s issuer, insurer or guarantor, may affect the bond’s value. In general, an investor is paid a higher yield to assume a greater degree of credit risk. The risks associated with higher-yielding, lower-rated debt securities include higher risk of default and loss of principal. Investments in foreign securities involve special risks including currency fluctuations, economic instability and political developments.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.’

1. There is no assurance that any estimate, forecast or projection will be realized.

2. Source: Bloomberg. The market is pricing in a 61 basis-point cut to the federal funds rate by the end of this year. As of April 10, 2023.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All