The dollar's strengths still outweigh its weaknesses.

Last week, Carl reminded us of his disdain for discussions of alternative currencies. I share his skepticism of that subject, but have found I’m developing a broader pet peeve: questions about the end of the dollar’s status as a reserve currency.

Recent anxiety has been kindled by short term arrangements in which countries seek to exchange more directly with one another in their own currencies. China has established quite a few of these agreements over the past year. But broader concerns about the U.S. dollar center on the high level of U.S. debt and the seeming inability of the Congress to do anything about it. The risk that the currency will be debased to make that debt manageable comes up often in conversations.

Is the end of the dollar’s reign is upon us? The prospect is worrisome to Americans. The dollar’s leading status has conferred “exorbitant privilege” to the U.S. in all matters of international trade. U.S. businesses and consumers have benefitted from cheap imports and ease of transacting when the world caters to our currency; reliable demand for U.S. Treasuries has allowed the nation to run deficits at little cost.

The dollar’s primacy was an outcome of the United States’ economic dominance and international power in the wake of World War II. Previously, the U.K.’s mercantile fleet led the world, while Germany was also ascending, but the war left both nations in shambles. The transition illustrates an important point: changes in reserve status often occur as the result of geopolitical upheaval, as opposed to a slow accumulation of contributing factors.

For a currency to be used globally, it requires a stable underlying government and a trustworthy central bank. The currency needs a high degree of liquidity and must trade freely. It should serve as the basis of international benchmark investments, which U.S. Treasuries represent. Markets in a reserve currency’s home country should be transparent and protect investors with appropriate securities law.

And in the case of the dollar, accepting the currency allows international exporters to sell to the world’s richest and most eager base of consumers. The nation is a major net importer of goods and therefore an exporter of dollars.

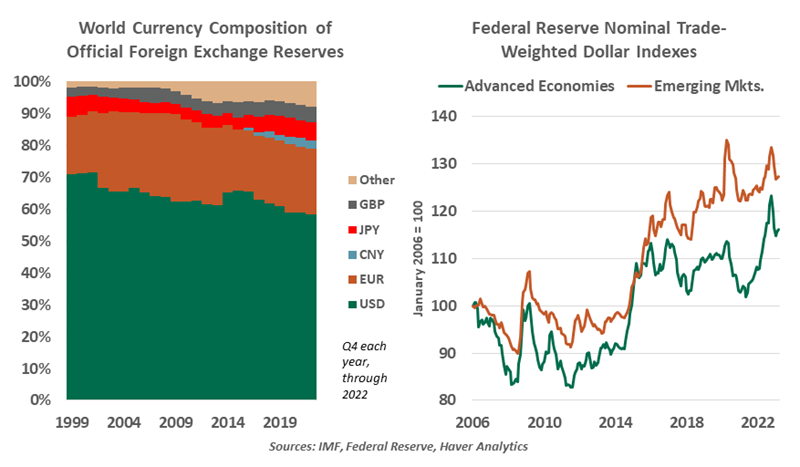

By those standards, no currency stands ready to unseat the dollar. Recent news reveals China’s ambition, but trade in yuan exposes counterparties to China’s capital controls and restrictions on foreign trade. The nation has not earned the confidence of the global financial system. When the U.S. shows domestic vulnerability, China will seize the opportunity to raise its profile. From the debt ceiling to election disputes, the U.S. has shown this is a good time to strike.

The dollar ascended from the strength and openness of the U.S. economy.

The market of most interest and some consequence is petroleum, which is traded in U.S. dollars. This system has supported demand for dollars, but at the price of higher volatility in foreign exchange (FX) rates. Unpredictable movements in oil prices have caused massive swings in FX values, imperiling nations that depend on oil exports. Countries have sought for decades to reduce the use of dollars, to little avail.

To be sure, the dollar has been losing some ground over the past thirty years. According to the International Monetary Fund, demand for dollars in official foreign exchange reserves peaked in 2001, but it still represents the majority of foreign holdings today.

As the world shifts toward near- and friend-shoring, nations will become more balanced in their roles as producers and consumers. The volume of international transactions could moderate, reducing the demand for currency conversion. This is certainly something that bears watching.

Ultimately, however, shifts away from the dollar would have to go to some other currency. And while the U.S. is not handling its fiscal position very well, other countries are much worse off. Further, a weaker dollar would reduce U.S. capacity to purchase exports from other countries, an outcome that would be unwelcome around the world.

Being called the cleanest shirt in the laundry is not exactly a ringing endorsement. But for the foreseeable future, it should be enough for the dollar to retain its dominance.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A.

© Northern Trust

Read more commentaries by Northern Trust