Tightening credit conditions will weigh on growth, especially in Europe.

Financial volatility continues to moderate amid settling in the banking sector. Economic data in much of the world has remained positive. But a slowdown is in store. Businesses and households will have a harder time borrowing as credit conditions tighten further. Financial risks have risen. Despite the most aggressive tightening cycle in decades, inflation remains too high for comfort. In sum: interest rates are set to stay higher for longer, while growth will be lower for longer.

Last year’s instability in the U.K.’s gilt market and the recent banking sector turmoil in the U.S. remind us of the substantial vulnerabilities that exist among banks and non-bank financial intermediaries. A stalemate in the Ukraine war continues to threaten the reliability of food and energy supply chains. The downturn of U.S.-China relations will remain another source of uncertainty.

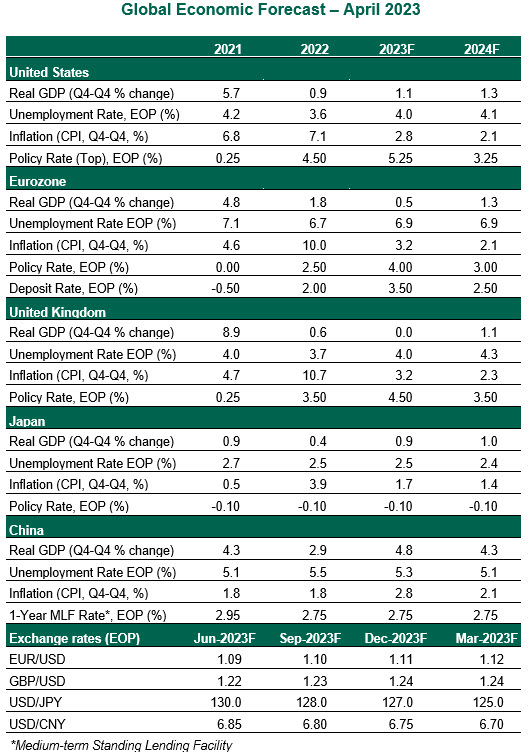

Here are our up-to-date perspectives on how major economies are poised to perform during this year and next.

United States

- Inflation is moderating but remains elevated. The headline consumer price index decelerated to 5.0% year over year in March, driven by lower prices of utilities and food at home. Core inflation was less encouraging, ticking up one-tenth to 5.6%. The price correction in durable goods has run its course, while services inflation persists. The surge in shelter costs has started to slow and should support disinflation in the months to come. Wage growth has fallen from a peak but is higher than past norms.

- With inflation still elevated and labor markets showing little slack, we expect the Fed to issue another 25 basis point rate hike at its May 3 meeting. However, credit conditions have tightened following Silicon Valley Bank’s failure, which will weigh on the economy and reduce the need for further tightening.