Last week, the International Monetary Fund (IMF) lowered its outlook for the global economy, painting a gloomy picture of subdued growth, with advanced economies lagging. The Fund expects emerging markets (EMs) to outperform their developed counterparts in the next two years, largely driven by major hubs like China and India.

In fact, the outlook for smaller and low-income countries is quite bleak. Smaller developing countries are dealing with a host of challenges from rising borrowing costs, food insecurity and weaker external demand caused by de-globalization.

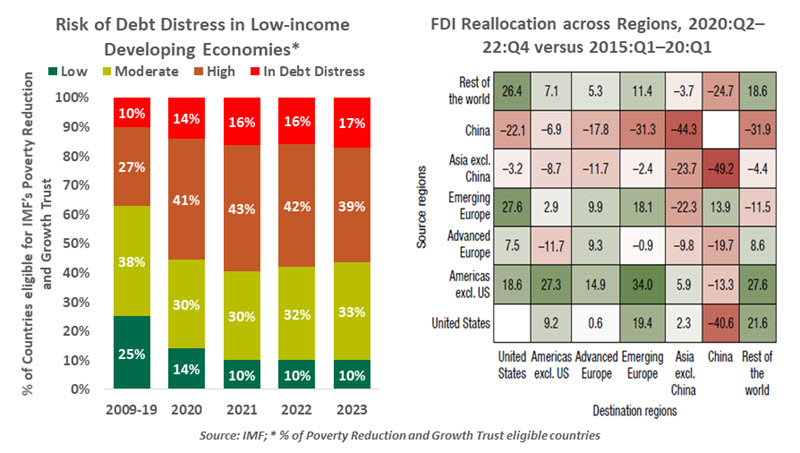

The combination of rising debt servicing costs, low reserves and softer growth could lead to a systemic debt crisis in the developing world. Several developing economies are facing sovereign credit spreads above 1,000 basis points, a sign of distress. According to the IMF, 17% of low-income economies are already in debt distress and 39% are estimated to be at high risk.

With pandemic-era support programs such as the Debt Service Suspension Initiative now sunset, we could see a new wave of debt-restructuring requests. Handling these will potentially be more difficult than in the past, owing to the evolving creditor landscape.

Many developing markets are facing a high risk of systemic sovereign debt distress.

The current banking turbulence in the U.S. and Europe has had limited impact on financial conditions in the developing world thus far. But the IMF predicts that a sharp tightening in global financial conditions or a “risk-off” shock could prove contagious to EMs by causing large capital outflows, a stronger dollar, surges in risk premia and declines in broader global activity.

Rising geopolitical tensions will exacerbate the risks for EMs. Foreign direct investment (FDI) has already been a casualty of increased fragmentation; FDI is vital to EMs, who need technology transfers. This trend will be especially consequential for EMs that are geopolitically misaligned with advanced economies, which are major sources of FDI.

With major central banks likely to stay higher for longer and geopolitical fragmentation accelerating rapidly, more and more EMs are likely to knock on the IMF’s door. Multilateral institutions like the IMF might be losing relevance in the eyes of major players of the global economy, but they will keep growing in importance to developing economies.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

© Northern Trust

Read more commentaries by Northern Trust