Economic Carbon Monoxide

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsTighter Lending Standards Smother Growth

Carbon monoxide can be deadly and on average more than 430 Americans perish annually with more than 50,000 people receiving treatment in an emergency department from carbon monoxide poisoning. Carbon dioxide is dangerous because it has no odor, color or taste, so it sneaks up on people. The most common symptoms of CO poisoning are headache, dizziness, weakness, nausea, vomiting, chest pain, and confusion. Poisonings occur more often in the winter, particularly from the use of portable generators during power outages. People can protect themselves from carbon monoxide poisoning by using monitors that cost less than $50.

Most investors focus on monetary policy and changes in interest rates. When the FOMC increases the Funds rate the majority of banks increase the Prime Rate on the same day. Many business and personal loans are tied to the Prime Rate. Home and auto loans are all based on an interest rate, so everyone has been trained to monitor the cost of money. Lending standards are a lot like carbon monoxide since they operate in the back ground. When the Senior Loan Officer Opinion Survey (SLOOOS) showed that banks significantly increased lending standards in the third quarter, no one on Wall Street noticed. I referenced this oversight in the January Macro Tides. “A large increase in lending standards is a really good recession indicator. A decline in the availability of credit is more restrictive and problematic for the economy than increasing the cost of credit. In the third quarter banks increased lending standards to a level (Above 20%) that presaged the recessions in 1990, 2001, and 2008. I listen to CNBC all day and I have yet to hear a single ‘expert’ mention the increase in lending standards in the third quarter. Instead, the ‘experts’ say the economy is holding up and any recession is likely to shallow.”

In the December 2022 Macro Tides I discussed why following changes in lending standards is so important. “In the third quarter banks aggressively tightened lending standards, which represents another tightening of monetary policy. The FOMC has increased the cost of borrowing, and banks are now curbing the availability of credit. The Federal Reserve is the liquidity spigot for the financial system, and banks are the nozzle at the end of the liquidity hose that governs the amount of liquidity flowing into the economy. As banks increase lending standards, the amount of liquidity flowing into the economy is less so economic activity slows. As the economy exhibits more signs of slowing in coming months, banks will increase lending standards further. This is what banks did in 2001, 2008, and in the early stages of the Pandemic.” After the Federal Reserve slashed interest rates in March 2020, provided liquidity lifelines to calm financial markets, and the Federal government unleashed a torrent of spending in March 2020 to resuscitate the economy ($2.4 trillion), banks quickly eased lending standards. That wasn’t the case in 2001 and in 2007, which I discussed in my March 2007 ‘The Financial Commentator’ (Macro Tides predecessor).

Excerpt from my March 2007 ‘The Financial Commentator’

“An intense debate is raging on whether the woes in the sub-prime mortgage market will spread to other areas of mortgage lending. As far as I’m concerned, it already has spread in one important way – lending standards. As I mentioned last month, in January (2007), the Federal Reserve’s quarterly lending survey found that more institutions had increased lending standards than at any time since 1991. Let’s think about what that means in the real world. Even though the Fed has kept the Funds rate unchanged for months, monetary policy has been effectively tightened by many lending institutions. This is just the opposite of what was happening as the Fed was increasing the Federal funds rate from 1.0% to 5.25%. The drag effect of those increases did not fully impact the economy, since many mortgage lenders continued to offer consumers mortgage rates of 1% to 2%. The pendulum has now swung the other way. Lending standards are not just being raised for sub-prime borrowers, but for borrowers across the board.”

“Higher lending standards will curb demand, even as foreclosures increase. It is hard to believe that less demand and more supply will not depress home values more than we’ve already seen. When the Fed does lower rates, the higher lending standards will still be maintained for some extended time. The Fed will only lower rates, if the expected late 2007 rebound in the economy looks doubtful, or the housing market weakens sharply. If the economy warrants Fed easing, mortgage payment delinquencies and foreclosures will be rising. That is not an environment conducive to lowering lending standards, and lending institutions won’t. This means the drag on the economy from tighter lending standards will continue even after the Fed lowers rates. This also means the stimulus normally provided the economy from rate reductions will not completely pass through to consumers. Just as mortgage lenders negated the drag from higher rates between 2004 and 2006, they will limit the beneficial effects of lower rates, just as the economy will need them the most.”

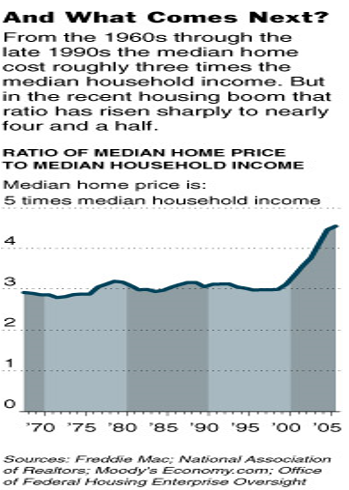

Excerpt from my September 2007 ‘The Financial Commentator’ “Between 1968 and 2000, the ratio of the median home price to median household income fluctuated in a narrow range between 2.8 and 3.2. During this 32 year period, increases in home prices were supported by a rise in household income. This relationship provided underlying support for home prices, even when recessions developed in 1970, 1974, 1981, 1990 and 2001. However, between 2000 and 2006, the ratio rose from its long term average of 3.0 to 4.5. This means median home prices have the potential to fall 33% should the ratio fall back to its long term average.”

“In a recent analysis by Moody’s of home values, mortgage rates, tax rates and incomes going back to 1968, home values appeared 20% too high. Adding validity to this estimate, Federal Reserve Governor Frederic Mishkin recently estimated that housing prices could decline 20% in coming years. It is important to remember that these estimates are based on median home prices. In California and along the east coast, average home prices are two to three times the level of national median home prices. If national median home prices sink by 20% in coming years, home prices on both coasts could fall by 30% or more. The total value of housing in the U.S. is $20 trillion. A 20% drop in home values would slash $4 trillion from homeowners’ wealth, and maybe more if prices drop more on the coasts.”

The idea that home prices could fall by more than 20% seemed outrageous in 2007. But the increase in lending standards in 2007 acted as a trip wire for a series of dominoes that led to declining home values, a financial crisis, and an Unemployment Rate of 10.0%. The following review will set the table for what sectors could be most vulnerable to a dislocation in 2023 and 2024 from the recent increase in Lending Standards. These Six Dominoes have increased the risk of a Hard Landing in 2024.

The Six Dominoes of Recession

The first domino is a change in monetary policy as the FOMC determines that it needs to increase the cost of money. The level of inflation has dictated the speed and magnitude of rate hikes. When inflation was a big problem in the 1970’s, the FOMC was forced to jack up the Funds rate. In 1972-1974 the Funds rate was increased by 7.75% in 17 months, and by 10.25% in just 10 months in 1980-1981. The largest increase occurred in 1977-1980 when the Funds rate rose by 14.0% in 32 months. People forget that Chairman Paul Volker slashed the Funds rate in 1980 as the economy slumped only to increase it again in 1981. In 2022 inflation hit its highest level since 1980 so the sharp increase in the Funds rate was warranted. The pace of rate increases in the 2004 and 2015 cycles were much slower and modest because Core CPI inflation was near 2.0%. It is much easier for borrowers to adjust to the higher cost of money if rate hikes are slow. A slower pace of rate hikes has a gradual impact on economic activity and results in fewer unintended consequences, i.e. accidents. The pace and magnitude of the FOMC’s hikes since March 2022 have been aggressive, so the risk of unforeseen accidents is higher.

The second Domino is an inverted yield curve. In the majority of economic cycles since 1947 the yield curve has become inverted after the FOMC continued to lift the Funds rate. An inverted yield curve develops when short term rates (Funds rate, 3- month Treasury bill rate, 2-year Treasury yield) rises above long term Treasury yields (10-year Treasury yield, 30-year Treasury yield). There has been a high correlation between an inverted yield curve and recessions, but the lag time is long and variable. (Average is 19 months since 1950)

An inverted yield curve has been a leading indicator for recession and increases in Lending Standards. As banks anticipate the coming economic slowdown or recession and potential loan losses, they cut back on new lending, increase the spread margin as loans come due, decide to reduce the amount of loans to existing borrowers, or simply choose not to roll the existing loan over. Since 1999 lending standards (blue) haven’t topped until they have been increased to the level of the inverted yield curve (yellow). Lending standards were up in the third and fourth quarter, well before the Regional bank crisis erupted in March. Lending Standards will continue to be increased as the economy shows more signs of slowing. The third Domino is an increase in Lending Standards.

I discussed the coming increase in Lending Standards in the November 2022 Macro Tides. “The FOMC has increased the cost of money, but the availability and access to credit is still easy. This will change in 2023. As the economy slows in 2023, lending standards for all forms of credit will be tightened by banks, representing an additional tightening of monetary policy. The Federal Reserve is the credit spigot and banks are the nozzle at the end of the credit hose. Consumers and small and medium sized businesses will find it harder to borrow and will cut back on discretionary spending and capital spending. Once the availability of credit is constrained, the slowdown in the economy will accelerate.”

After the FOMC increased the Funds rate for the first time on March 16, 2022, Chair Powell emphasized that the central bank he leads could succeed in its quest to tame rapid inflation without causing unemployment to rise or setting off a recession (Soft Landing). “The historical record provides some grounds for optimism.” During his press conference he provided a chart showing that no recession developed in 1965, 1984, and 1995 after the FOMC had increased the Funds rate (red circles on chart). The Fed tightened monetary policy by increasing the federal-funds rate significantly in 1965 (from 3.4% to 5.8%), 1984 (9.6% to 11.6%) and 1994-95 (3% to 6%) without precipitating a recession. In each of these episodes, the Unemployment Rate fell from 5.1% to 3.6% in 1965, 7.8% to 7.5% in 1984, and in 1995 to 5.8% from 6.5%.

Although the FOMC increased the Funds rate significantly in those Soft Landing years, banks didn’t increase their Lending Standards. Consumers and businesses weren’t denied access to credit and were able to borrow what they needed. This is why those three Soft Landings occurred despite the increases in the Funds rate.

As I noted in the March Macro Tides, a recession has followed whenever more than 20% of banks have tightened lending standards since 1990. In the fourth quarter, 43% of banks tightened their lending standards and more will once the economy slows. Investors who are banking on a Soft Landing are likely to be disappointed. At the end of 2022 Lending Standards were tight enough to cause a decline in lending in 2023. The Regional bank crisis will only make it worse as small banks cut lending. The fourth Domino is a decrease in bank lending.

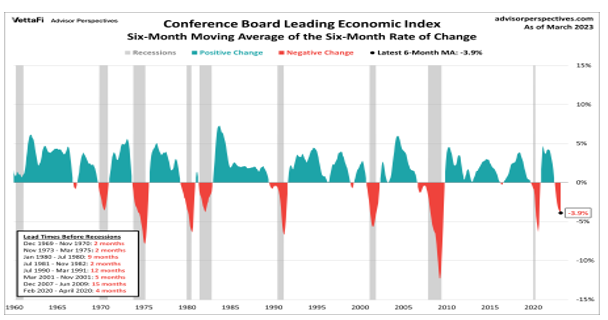

The fifth Domino is the onset of a recession. The Leading Economic Index (LEI) declined for the 12th consecutive month in March and is down -4.5% in the last six months. Since 1959 the LEI has never fallen this much without a recession developing. The LEI is a composite of 10 separate economic data points covering the labor market, goods production, Consumer expectations, housing, and financial markets. In March 7 of the 10 inputs were negative and the other 3 were barely positive. (0.0, 0.1, 0.2)

The LEI didn’t signal a recession in 1965, 1984, and 1995. The LEI has been below its 6-month moving average for 9 months. On average a recession has occurred 6.7 months after the 6-month average has been negative. My expectation has been that the economy will weaken significantly after mid-year and potentially enter a recession before the end of 2023. The trend in the LEI supports this view.

The Unemployment Rate is a lagging economic indicator since employers are reluctant to hire until they’re sure a recession is over and hesitant to fire employees until a recession causes revenue to weaken. Since higher interest rates and tighter Lending Standards initiate a slowing in economic growth, it only follows that an increase in Lending Standards is a leading indicator for increases in the Unemployment Rate. The sixth Domino is an increase in the Unemployment Rate.

The largest increase in Unemployment occurs after the recession takes hold. As the Unemployment Rate increases, Consumer Confidence drops and consumer spending falls as the majority of consumers curb their spending. The retrenchment in consumer spending causes the recession to deepen, leading to more layoffs, and a cutback in business spending. Once a recession becomes obvious the Federal Reserve intervenes by lowering the Funds rate.

The first three Domino’s have already fallen (Monetary policy, Inverted Yield Curve, Lending Standards). A decrease in overall Lending likely began in the first quarter and will become more restrictive in coming months. A recession is likely before the end of 2023 and the Unemployment Rate will begin to inch higher in the second half of this year and jump in 2024.

Most Vulnerable Sectors Now

Commercial Real Estate

In 2021 Commercial Real Estate was up 150% from the low in 2011 and overvalued. The FOMC’s decision to keep interest rates at 0% and repression of long term Treasury yields through Quantitative Easing pushed the Cap Rate for Commercial Real Estate to extreme lows. The Cap Rate is the expected rate of cash flow return for a property. A property worth $20 million generating Net Operating Income (NOI) of $1,000,000 would have a Cap Rate of 5.0%. The Cap Rate is comparable to the Price Earnings ratio used to value stocks. A property with a Cap Rate of 5.0% would have P/E ratio of 20.0 (20 X $1,000,000 = $20,000,000). If an investor was choosing between the 1.6% return provided by a 10-year Treasury bond in 2021 or a property with a yield of 5.0%, it was a relative easy decision. With short term rates up from .12% in March 2021 to 4.75% in March 2023 and the 10-year Treasury yield more than double its 2021 yield (1.60%), properties with a Cap Rate of 5.0% are too expensive and overvalued.

The Pandemic changed where millions of workers work with many being able to work from home rather than in an office. According to a recent report by the Labor Department, 72.5% of businesses surveyed said their employees rarely or didn’t work remotely last year, up from 60.1% in 2021. Research by economists at the University of Chicago found that 27.7% of total days worked were from home, after holding at 30% throughout 2022. According to staffing firm Manpower, 13% of job postings are for remote positions which is down from 17% in March 2022, but up from 4% before the Pandemic. Irrespective of the exact percent, the number of workers that work full time in an office is less than in 2019 and is unlikely to increase significantly in the next two years. Employers need less office space as more workers spend less time in an office.

As leases come due, many employers have or will lease less space and pay less in rent. Leasing activity is down -42.2% from the first quarter of 2020 through the first quarter of 2023, according to Avison Young. Over that same period the amount of subleased space available doubled, as companies locked into a long term lease attempted to recoup a portion of their costs by subleasing space to another firm. Subleases are generally offered at a steep discount to existing leases. The amount of subleased space available will put downward pressure on leases coming up for renewal, until the excess office space supply is absorbed in each city.

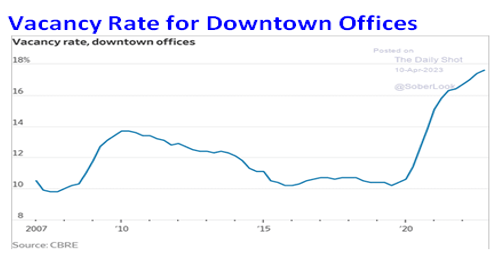

This problem has been particularly acute for properties located in downtown areas. Since the end of 2019 the vacancy rate for downtown office building has soared from 10.2% to 17.8%, according to CBRE. This has materially lowered the Net Operating Income for office buildings and reduced the value of the properties. Downtown Office buildings in some cities have experienced a decline of more than 40% in their value based on the increase in Cap Rates.

San Francisco has been hit especially hard given the concentration of Tech and Financial firms. In the last year some of the largest high profile technology companies have let go of thousands of workers that have headquarters or a large office space foot print in San Francisco. According to CBRE nearly 30% of San Francisco’s office space is now vacant compared to just 4% prior to the Pandemic. In the first quarter asking office rent was down only -14.8% ($88.40 - $75.25 per square foot) but lower prices are coming. Companies that have reduced their office space have been subleasing their unwanted space at $25.00 a square foot or down -71.7%. This excess supply will continue to put downward pressure on rents until it’s absorbed. In 2019 a prime building in downtown San Francisco had a value of $300 million. The occupancy rate today is just 25% after Union Bank and other tenants left. It’s up for sale and bids are expected for $60 million or 80% below its 2019 valuation. The decline in Commercial Real Estate values in the next two years will lower tax collections for cities and pressure budgets. Tax collections will also be reduced as small businesses that relied on office workers for revenue close or move out.

The decline in commercial Real Estate values isn’t limited to Office buildings. The increase in interest rates has lowered the Cap Rate for Real Estate values in general. Apartment buildings and shopping Malls have lost more than 18% of their value and losses of more than 10% have clipped Industrial buildings and Retail strip malls. The question is which lenders will be exposed to potential losses on their Commercial Real Estate loans.

Small Banks are Vulnerable

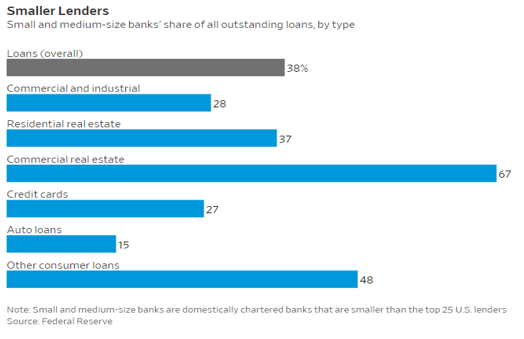

After the Financial Crisis Small banks (assets less than $250 billion) ramped up their lending to Commercial Estate far more aggressively than large banks. At the end of 2022 Commercial Real Estate lending comprised almost 30% of all loans for Small Banks compared to just 5% for Large Banks. Small Banks hold 67% of all bank Commercial Real Estate loans and will suffer the consequences as valuations fall and defaults increase.

Of the $4.532 trillion in Commercial Real Estate debt, Banks have lent 38.6%, Fannie Mae and Freddie Mac are on the hook for 21.0%, with Insurance Companies exposure at 14.7%. All of these lenders will cut back on lending for construction of new properties which will lower GDP growth and employment growth in the next two years. Although banks aren’t the only lenders that are at risk for losses from the $4.532 trillion in Commercial Real Estate loans, bank losses will negatively impact bank lending and economic growth.

The real crunch will develop as $1.4 trillion in Commercial Real Estate loans come due in the next two years, with rates up 3.5% to 4.5%, according to Morgan Stanley. Small banks have the most exposure (67% of total R.E. bank loans) and will be forced to make difficult decisions.

As Commercial Real Estate values decline in the next two years, there will be properties that are worth less than the loan forcing small and large banks to increase loan loss reserves. The Cap Rate for some properties won’t support rolling over the existing loan so the terms will be adjusted. Less favorable terms (higher interest rate and smaller loan to property value) will increase the economic pressure on property owners. Some owners will be able to handle the less favorable terms. Other owners will walk away from properties that are under water and leave the bank with a loss on the original loan. And after having increased their Lending Standards, there will be properties that small banks will be unwilling to lend any money. Property owners will scramble to find another lender on far less favorable terms, or be forced to sell into a weak market and drive valuations lower. In the next two years there will be an increase in loan defaults and property foreclosures. If a recession develops before year end as I expect, the problems small banks and property owners are already experiencing will get much worse in 2024. This is one problem that could cause a Hard Landing in 2024.

Small Businesses are Vulnerable

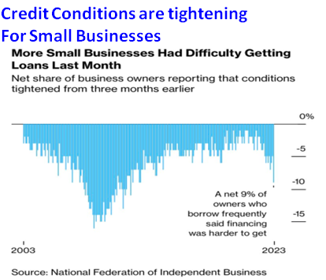

Large public companies can tap the credit market when they need funds by selling bonds or stock, so they are far less dependent on banks to fund their growth. Small businesses don’t have access to the credit market and are dependent on banks to extend credit via a loan. When banks increase Lending Standards small businesses pay more for credit (Loan spread above Prime Rate increases) or have less access to credit. According to last month’s survey of small businesses by the National Federal of Independent Business, a net 9% of owners said borrowing was more difficult. At the lows of the Financial Crisis the net was about 16%. More often than not, small business owners have a long standing relationship with their bank. But when banks become concerned about the economy, banks get tough on the small businesses that are less stout. As the economy slows in coming months banks will become more stingy as loans come due, which will force many small businesses to cut costs including laying off workers.

Since Small Banks provide a lot of credit to many sectors within the economy, a further increase in Lending Standards will have a chilling effect on the overall economy and contribute to the onset of a recession. This was reviewed in the March 27 Weekly Technical Review. “Small banks provide 38% of all lending so the negative impact on overall credit will extend beyond commercial real estate. Small banks fund 28% of Commercial and Industrial loans in the US so many small businesses will feel the crunch as small banks increase their lending standards and decrease their lending volumes. Consumers will feel the pinch since small banks fund 27% of credit card debt, and potential home buyers find it more costly to land a mortgage since 37% of mortgages are provided by small banks. It will likely be tougher and more expensive to borrow for a car purchase as small banks underwrite 15% of auto loans. The coming contraction in lending by small banks is going to have a far reaching dampener on economic activity in the next year.”

The increase in Lending Standards in the third and fourth quarter is already having a big negative impact on Private small businesses. The four week average of weekly bankruptcies has increased from 1 or 2 in the first quarter of 2022 to 9 per week in March. The increase mirrors the increase in the Funds rate, but there are likely other factors in play. The money received from the federal government in 2020 and 2021 may have run out for some firms. The surge of inflation likely squeezed some firms that failed to manage the increase in costs well. We know that many small firms struggled to find workers which may have forced them to reduce their operating hours if they were a retail business. It must be noted though that this increase occurred while the economy was still experiencing nominal growth of 9.2% and real growth of 2.1% in 2022. Tighter Lending Standards and a recession will cause many more small businesses to go bankrupt by the end of 2024 with an attendant increase in unemployment.

Consumer Credit

In January 2023 1.89% of auto loans were at least 60 days past due and ‘severely delinquent’. That was the highest rate since 2006, and higher interest rates are surely playing a role. No surprise then that in the first quarter of 2023 the percentage of banks tightening Lending Standards for Auto Loans increased from 1% to 17%. From 2021 until January 2021 a consumer needed about 35 weeks of income to buy a new car or truck. The price of a new car soared in 2022 and it now takes 44 weeks of income to buy a new vehicle, even though wages have increased too. The default rate on Auto loans will jump during the next recession and provide an opportunity to buy a used car at a lower price.

The delinquency rate for Credit Cards began to trend higher after the FOMC increased the Funds rate in March 2022. The increase has been especially swift for younger card users (those under 40), which are more delinquent now than any time since 2010. This is why banks significantly tightened lending standards on credit cards in the fourth quarter and further in the first quarter. Keep in mind that the Unemployment Rate is at a 50 year low. The delinquency rate will soar and banks will tighten their credit card lending standards more, after the Unemployment Rate begins to rise. This will crimp consumer spending as the economy enters a recession and deepen it. This is another reason why a Hard Landing is possible in 2024.

Small banks have been aggressive in recent years in extending credit through credit cards. In aggregate Small Banks now own 27% of credit card debt and 15% of auto loans. The top panel highlights the delinquency rate for credit cards issued by small banks compared to large banks. The delinquency rate for small banks at the end of 2022 was 6.4% compared to 2.0% for large banks (left scale). Large bank write offs are negligible but small bank write offs were 7.1% (right scale). Small banks have done a great job of positioning themselves so they will lose money on Auto loans and Credit Cards, and a lot of money on Commercial Real Estate. As the losses become public (quarterly reports), what do you think will happen to Small Bank deposits?

Deposit Drain Will Continue

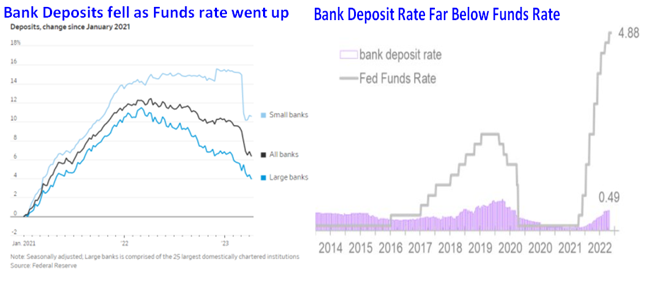

After the FOMC increased the Funds rate Deposits began to leave banks. At first the drain was slow, but as the spread widened between what a deposit could earn at a bank versus a money market fund or on short term Treasury debt, it accelerated especially at large banks. Small banks offered higher yields so deposits were sticky. That changed with the failures of Silicon Valley Bank and Signature Bank. Deposits will continue to flow out of banks since the fundamental problem hasn’t changed – yields are much higher elsewhere. (4.5%+ vs. 0.49%)

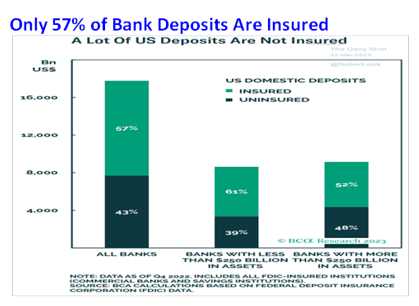

Safety is the second determinant. Only 57% of bank deposits are insured and the spread between small banks (61%) and large banks (52%) isn’t much different. What sparked the run on Silicon Valley Bank and Signature Bank was the departure of uninsured deposits above $250,000. Future runs could be avoided if the deposit insurance level was increased to $1,000,000, as that would insure the majority of account holders. If this change isn’t made, the risk of another run on more small banks will be higher, as losses in coming quarters from Commercial Real Estate and consumer loans scare depositors away.

Bank runs are driven by fear and in this era of technology can spread faster than any bank run in the 1930’s. The best way to stop a bank run is before it starts and an increase in the insured deposit amount would be a smart step forward. Some politicians will oppose an increase but they need to consider a second issue. Large ‘too big to fail’ banks have a perceived unlimited insured deposit level since they will never be allowed to go under. The government’s response in the 2008 Financial Crisis proved this point. Small banks don’t have the ‘too big to fail’ shield and an increase in deposit insurance would provide most small bank depositors peace of mind.

As fear swept the banking system in March, deposits flowed out of small banks and into large banks for the protection ‘too big to fail’ banks provide. In the short run this solved a problem for depositors, but may create a longer term problem. The top 15 banks in the US already have 74.0% of total deposits. The largest 5 banks have 46.2% of bank assets, according to the St. Louis Federal Reserve, up from 31.1% in 2003. Small banks have a unique position in most communities and can provide personalized services that help local small businesses prosper. An increase in deposit insurance will help keep small banks alive and in position to compete with the ‘too big to fail’ banks in communities throughout the US.

Employment

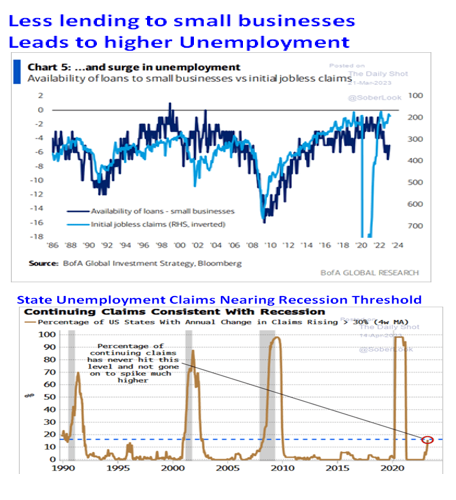

Since 1985 there has been a high correlation between the availability of credit for small businesses and the labor market as measured by jobless claims. As banks increase Lending Standards to small businesses and reduce lending, economic growth slows. Eventually small businesses respond to the weaker economic environment by letting workers go who then file an unemployment claim. As noted previously, a net 9% of small business owners said borrowing was more difficult in last month’s survey of small businesses by the National Federal of Independent Business (chart pg. 10). The number of Unemployment Claims has been trending upward in a number of states, but has yet to reach the threshold that has signaled a recession. That signal will arrive before year end.

The consensus is that the economy can avoid a recession and many point to the continued strength in the labor to support that view. The problem is that the labor market is a lagging indicator and the most reliable leading indicators have already spoken: a recession is coming.

Stocks

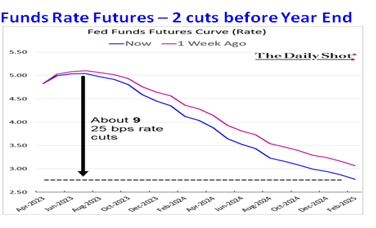

Wall Street expects the FOMC to lower the Funds rate in the second half of 2023. Chair Powell has repeatedly referenced the labor market as being the key to monetary policy since his speech at Brookings on November 30. In Powell’s prepared statement after the FOMC meeting on March 22 and before the start of his press conference Powell said, “The labor market remains extremely tight.” The FOMC won’t lower the Funds rate as long as the Unemployment Rate is below 4.0%. Wall Street has yet to pivot from believing that inflation is the FOMC’s guidepost for policy. With inflation falling Wall Street thinks it’s just a matter of when the FOMC cuts the Funds rate. They’re wrong.

Wall Street also believes the stock market will zoom higher when the FOMC does lower the Funds rate. The FOMC only cuts the Funds rate when there is a severe liquidity squeeze, financial crisis, or significant economic weakness. The stock market doesn’t respond well to these events since all lead to a decline in earnings. This is why the S&P 500 has declined every time after the first rate cut by the FOMC. Large draw downs occurred in recessions with the largest declines following the times valuations were excessive (1973, 2000, 2007, and 2022?). Unless the economy avoids a recession, the S&P 500 is likely to experience a meaningful decline once a recession appears before the end of the year. The additional hurdle in this cycle is that Chair Powell has said it would be a bigger mistake for the FOMC to prematurely lower the Funds rate before inflation is under control. In the last 20 years Wall Street has been trained by the FOMC to cut the Funds rate at the first sign of weakness. The FOMC was able to respond with cuts because inflation was only modestly above their 2.0% target. Powell is saying the FOMC doesn’t have that flexibility with inflation so far above the inflation target. Wall Street has yet to hear his message. Since the message isn’t likely to change, it’s only a question of when Wall Street listens and acts surprised!

As discussed in the April 24 Weekly Technical Review, the S&P 500 is still expected to rally above 4195. If it does rally above 4195, short covering could lift it to 4250 – 4275, possibly up to the August high of 4325. If the S&P 500 closes above 4200, armchair technicians will note the S&P 500’s breakout above 4200. Fundamental analysts will say that the S&P 500 is telling them the risk of a recession is low since markets discount the future. (Even though the S&P 500’s all time high in January 2022 failed to warn them of the coming +20% plunge!). Investors should use this rally to reduce exposure.

Irrespective of a rally in the near term, the outlook remains for the economy to show more slowing after mid-year, with the odds of a recession beginning before year-end. Once this becomes clear to those who think there will be No Landing or Recession, the S&P 500 is expected to retest the October low of 3492, and potentially fall to 3200. Once the short term bounce is over, the S&P 500 will be vulnerable to a larger decline. I will provide instructions for shorting the S&P 500 in the WTR.

Treasury Yields

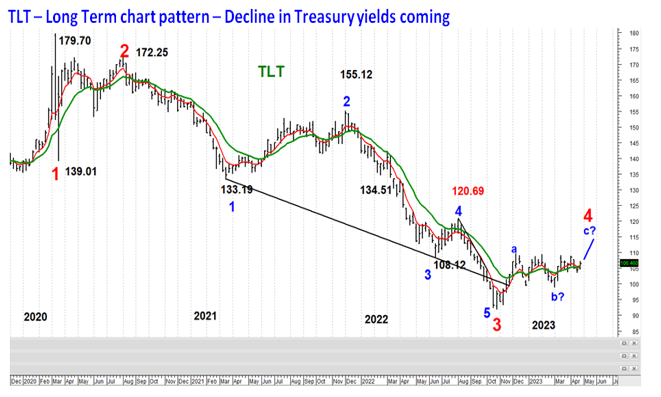

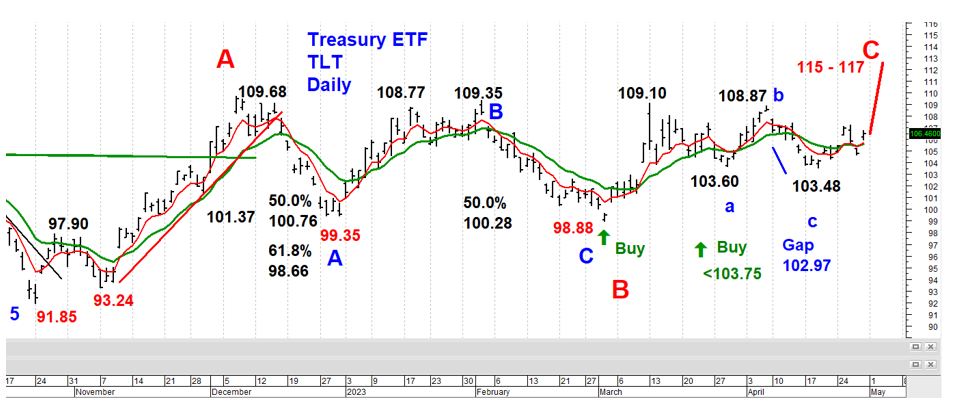

Fundamentally, I expect a recession to begin before the end of 2023 which should be a tailwind for Treasury yields to fall. Technically, the chart pattern in the Treasury bond ETF (TLT) suggests TLT will rally as Treasury yields decline. TLT has completed 3 waves down (red numbers) of what is expected to be a 5 wave decline from its March 2020 high. Since bottoming for Wave 3 (red) in October, TLT is rallying in Wave 4.

The first phase of the Wave 4 rally carried TLT from 91.85 to 109.68 (red Wave A of Wave 4). The pullback to 98.88 represents red Wave B of Wave 4, which should be followed by Wave C of wave 4 above 109.68 (high of Wave A). Price wise Wave C is often equal or longer than Wave A. TLT rallied from 91.85 to 109.68 or 17.83. An equal rally from the price low of red Wave B (98.88) would lift TLT to 116.71 for Wave C of Wave 4. TLT could rally to 120.69 which is Wave 4 of lesser degree. A breakout will be signaled once TLT closes above 109.68 for 2 days. Traders can buy TLT if it declines below 103.48 using a close below 101.35 as a stop. There is a gap at 102.97 on March 8 that may be filled.

Dollar

The Dollar topped on March 8 and declined after the Regional bank crisis convinced currency markets that the FOMC might not increase the Funds rate anymore and was more likely to lower it in the second half of 2023. The FOMC isn’t going to lower the Funds rate with the Unemployment Rate below 4.0% and Chair Powell saying the labor market is extremely tight. Once currency traders realize this, the Dollar has the potential to rally above the March 8 high of 105.88, as long as it doesn’t close below recent lows of 100.78. A rally in the Dollar should pressure Gold, Emerging Markets, and International equities in general.

Gold

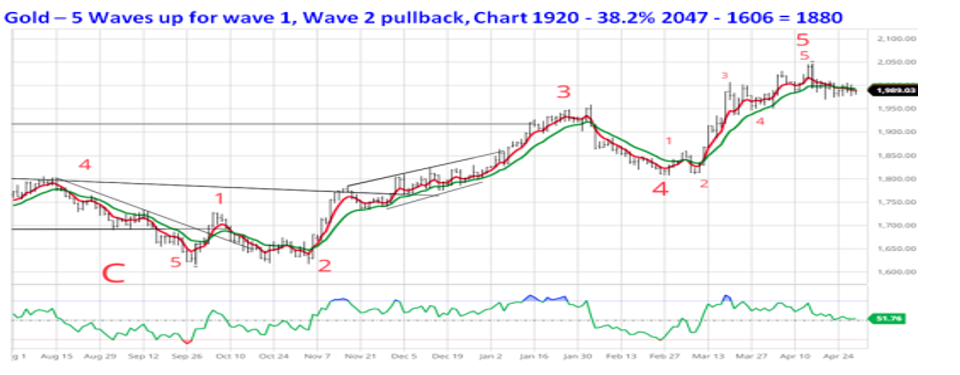

The Dollar was hurt by the Regional bank crisis and Gold benefitted as traders assumed it would force the FOMC to become more Dovish. Fundamentally, members of the FOMC will continue to remind markets that they intend to hold the Funds rate at the terminal rate for all of 2023. If the Dollar rallies in response to this message, Gold will experience a correction. Technically, Gold’s chart pattern suggests a Wave 2 pullback is developing that could bring Gold down to $1900 - $1920 at a minimum. The 38.2% retracement of Gold’s rally from $1616 to $2047 would bring Gold down to $1865 - $1890. Wave 4 of lesser degree at $1810. Gold rallied for 30 weeks so Wave 2 could last 8 to 12 weeks. The 5 Wave rally from the September low of $1616 (large red numerals) suggests Gold will rally to a new all time high in Wave 3, after the Wave 2 correction runs its course.

If Commercial Real Estate causes as much indigestion for small banks as I expect, and Lending Standards are increased even more by all banks, this is what the No Landing, Soft Landing, and No Recession will look like in 2024.

Jim Welsh

The Daily Shot

Every month I include dozens of charts and the majority of them come from The Daily Shot. I highly recommend those who like charts of economic data to subscribe to The Daily Shot https://thedailyshot.com/.

@JimWelshMacro

[email protected], MacroTides.com

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All