The Seesaw Becomes Extreme

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWe’ve described the past several years’ stock market as a seesaw in which the “market” was the fulcrum of the seesaw. On one side of the seesaw sit the highly speculative growth sectors of the market (Technology, Communications, and Consumer Discretionary) coupled with innovation, disruption, and meme stocks. On the other side of the seesaw, sit virtually everything else in the global equity markets.

The seesaw tilted significantly toward the speculative side during 2020 and 2021, but then significantly tilted in the other direction during 2022. The S&P 500® Growth Index outperformed the Value Index by an annualized 20 percentage points from 12/31/19 to 12/31/21. But then the Value Index outperformed the Growth Index by 24 percentage points from 12/31/21 to 12/31/22. (See Chart 1)

Leadership becomes extremely narrow

The seesaw is now tilting back toward the speculative side in a tremendous way. The stock market’s leadership has become extremely narrow, meaning only a small number of stocks are outperforming and contributing to the market’s year-to-date advance.

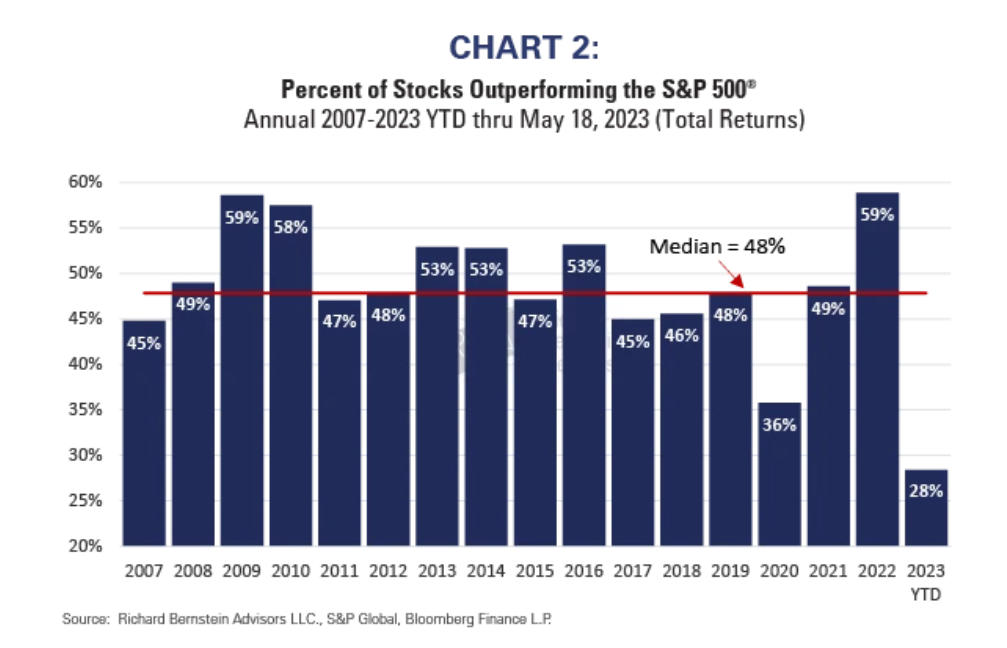

A simple method of measuring market breadth is the percent of the S&P 500® companies that outperform the index. Historically, improving economic conditions broaden the market as more companies benefit from the improving economy. As cycles mature, however, markets tend to become more “Darwinistic,” (i.e., survival of the fittest) because fewer companies can maintain their growth as the economy weakens.

Chart 2 shows the percent of S&P 500® companies that outperformed the index each year. 2023 has been the narrowest equity market since the financial crisis. Only 28% of the S&P 500® companies have outperformed the index so far during 2023. This is clearly extreme and probably unwarranted because the market today is even narrower than during the pandemic in 2020 despite that today’s economy is obviously much healthier than that during the pandemic.

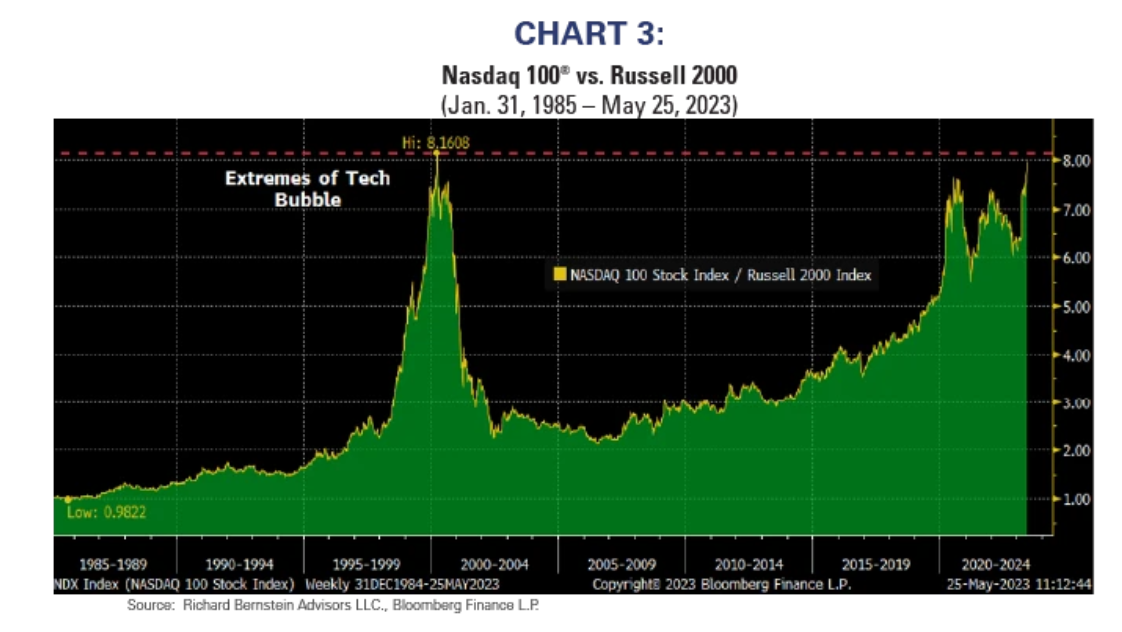

The relative performance between the most speculative larger capitalization growth stocks and the broader market has also reached an extreme. In fact, the current performance difference between the Nasdaq-100® and the Russell 2000 indices is currently mimicking that seen during the most extreme points of the Technology Bubble in 1999.

Aren’t there any other growth stories?

Historical evidence suggests that the present remarkably narrow leadership is not without precedent. Previous periods have witnessed instances where investors underestimated the abundance of growth stories available in the market.

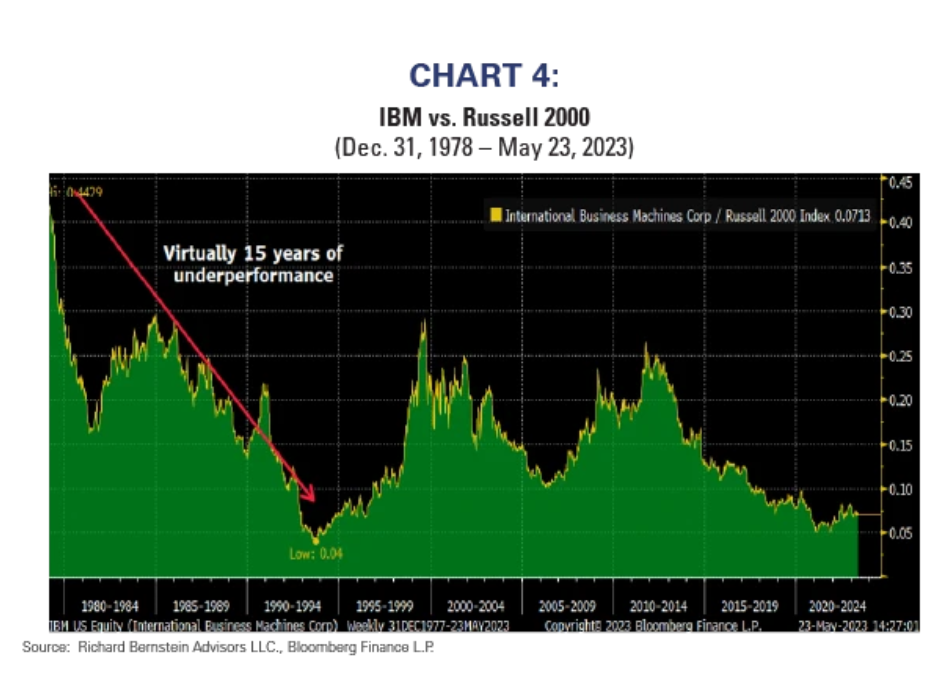

Some market observers have noted that Microsoft (MSFT) and Apple (AAPL) are now nearly 15% of the S&P 500®’s market capitalization, which is the largest proportion any two stocks have comprised of the S&P 500®since IBM and AT&T in 1978. (Note: RBA may own all four stocks in various portfolios.)

Investors unrealistically believed there were essentially only two growth stories in 1978. Of course, that was incorrect, and the stocks’ performance did not recover from those unrealistic expectations.

Chart 4 shows the relative price between IBM and the Russell 2000. After the 1978 peak, IBM effectively underperformed the Russell 2000 for most of the next 15 years. A similar analysis for AT&T is impossible because of the early-1980s divestiture of the Bell Operating Companies, but few investors today consider either stock to be a market bellwether.

We strongly doubt investors today could imagine Apple and Microsoft underperforming the broader market for the next 15 years, but 1978’s investors probably felt the same way about IBM and AT&T.

We aren’t the bears in the room. Are you?

We find it amusing that people say our views are so bearish when we actually believe the current menu of investment opportunities is very large. We do not particularly like the sectors and speculative assets that have become so popular, but they all reside on one side of the seesaw and that seat is up high in the air right now.

The implied economic forecast of investing in that side of the seesaw seems immensely bearish. The implication is the global economy will be so weak that only a handful of companies will be able to grow. That is a very bearish, almost dire, forecast of corporate survival.

On the other hand, the other seat on the seesaw contains all the other investment opportunities in the US and around the world. This is the side of the seesaw that dominates our portfolios.

Our view of the world seems very optimistic relative to the implied forecast that only a handful of companies can grow. We strongly doubt a global depression that might justify a Nifty 2 is imminent and believe the dire forecast implied by the market’s performance extremes will be proven wrong.

Investment opportunities seem plentiful relative to recent market action and investors’ momentum-dominated portfolios.

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All