After a challenging 2022, many advisors and investors began to question their traditional retirement approach to investing. Tony Davidow, Senior Alternative Investment Strategist with Franklin Templeton Institute, illustrates the potential impact of adding alternative investments to pursue growth and income—as well as seek to dampen volatility—during the accumulation and distribution phases of retirement.

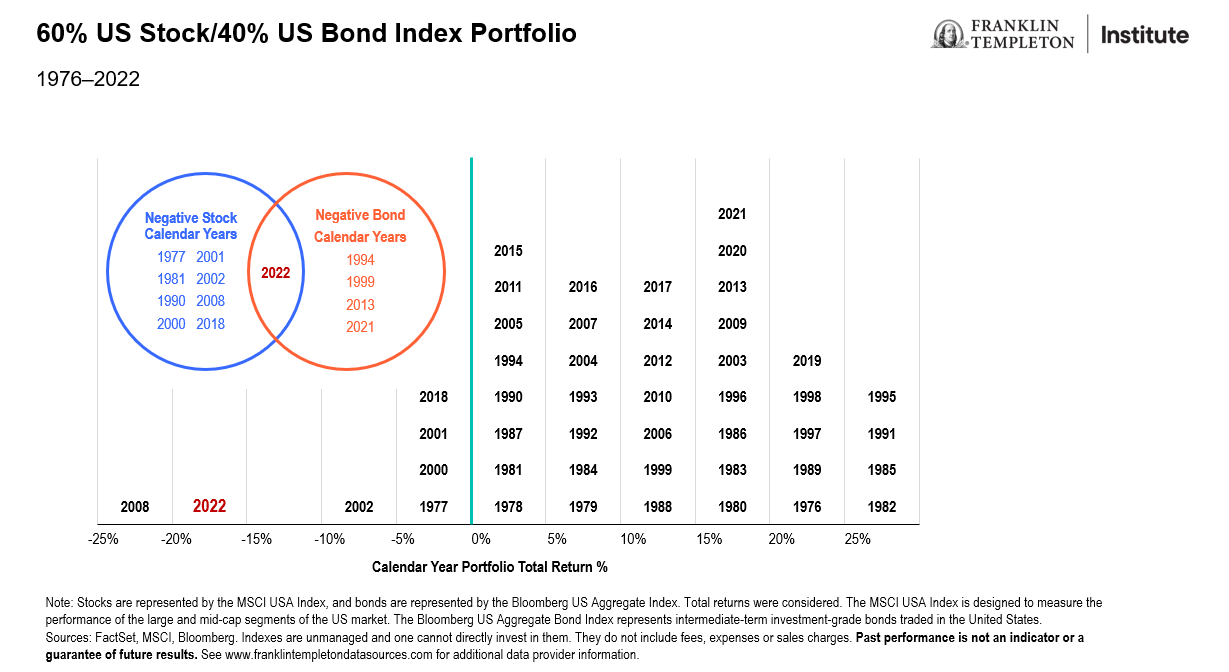

In 2022, stocks and bonds were both down double-digits for the year. According to Callan Associates, there have been only two other years since 1926 when both stocks and bonds have been negative—1931 and 1969.1 Rising interest rates, record inflation, increased volatility, and double-digit negative returns for both stocks and bonds during 2022 left many advisors and investors wondering if they need to reconsider their retirement portfolios.

We should be careful to separate the potential benefits of diversification and the 60/40 portfolio as a proxy. Unfortunately, as we experienced in 2022, there are periods of time when traditional investments are highly correlated to one another.

The roles and use of alternative investments

Pension plans have historically made significant allocations to alternative investments because of the various roles that they can play: pursuing growth and income, portfolio diversification, and inflation hedging. However, up until recently, many of these investments were limited to institutions and family offices. Now through product innovation, these investments are more accessible to a broader group of investors, with more flexible features.

Overall, in our view, retirement plans should be modernized to reflect the broader set of tools available to pursue client goals. We believe advisors and investors should rethink their retirement strategies to respond to the changing market environment, the new products at their disposal, and the fact that many retirees are living longer, more productive lives through their retirement years. Alternative investments can play multiple roles in retirement portfolios, which include generating potential growth and income, seeking to dampen volatility, and/or helping to hedge the impact of inflation.

We believe advisors and investors should develop different approaches for the accumulation and decumulation phases of retirement, and should periodically revisit retirement plans to ensure they are on target for their objectives. If used appropriately, alternative investments may improve the likelihood of achieving the various goals through retirement planning phases.

To learn more, please visit Alternatives by Franklin Templeton.

WHAT ARE THE RISKS?

All investments involve risks, including the possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline.

Investments in alternative investment strategies are complex and speculative investments, entail significant risk and should not be considered a complete investment program. Depending on the product invested in, an investment in alternative investments may provide for only limited liquidity and is suitable only for persons who can afford to lose the entire amount of their investment. An investment strategy focused primarily on privately held companies presents certain challenges and involves incremental risks as opposed to investments in public companies, such as dealing with the lack of available information about these companies as well as their general lack of liquidity.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed, or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions, and analyses are rendered as of the publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region, or market. There is no assurance that any prediction, projection, or forecast on the economy, stock market, bond market, or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not an indicator or a guarantee of future results. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third-party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated, or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from the use of this information and reliance upon the comments, opinions, and analyses in the material is at the sole discretion of the user.

Products, services, and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on the availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Distributors, LLC, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com – Franklin Distributors, LLC, member FINRA/SIPC, is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

1. Source: Kloepfer, J. “Unprecedented Territory—and the Inherent Limits of Diversification,” Callan, May 13, 2022.

A message from Advisor Perspectives and VettaFi: To learn more about this or other topics, please check out our most recent white papers.

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments