Less global integration will bring new costs and inefficiencies.

A perennial challenge faced by all big or small, developed or developing economies is achieving sustainable economic growth that boosts standards of living and financial stability. Globalization has been the road that brought economies to that destination.

The existing globalization model has worked well since the 1990s when the world started to become more interconnected. Easing restraints on flows of goods, services, and people has boosted growth, developed several emerging markets (EMs), and pulled millions out of extreme poverty. In advanced economies, it delivered lower prices, a particular benefit to low-income consumers.

Despite established benefits, discontent with the model has been growing. And as China and other major emerging economies develop, they are seeking to rewrite the rules governing world trade. The West, the original backer of globalization, is evolving toward a stance of greater protectionism.

A slow and uneven recovery from the 2008 financial crisis, rising income inequality, U.S.-China tensions, COVID, and the Ukraine war have all added to skepticism about the benefits of a global orientation. This has fueled geopolitical rivalries, technology decoupling, and trade barriers. With geopolitics becoming a driving force behind economic plans, the era of global integration is giving way to geo-economic fragmentation.

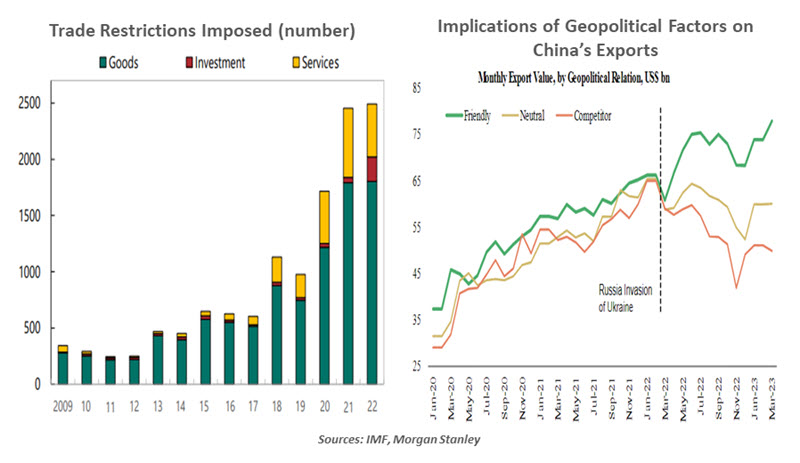

After periods of increasing globalization in trade, investment, and immigration, the global economy is becoming increasingly decentralized. Measures of trade openness have been on a steady decline as restrictions on movement of goods rise. Technology has been at the center of growing fragmentation. Export controls on critical raw materials have seen a sharp increase, especially amid the current U.S.-China tensions, with a rising number of restrictions linked to national security or strategic competition.

In recent years, the U.S. has imposed a sweeping set of export controls to cut China off from procuring advanced technologies aimed at slowing Beijing’s technological and military advances. Japan and other politically aligned economies are following the U.S.’ lead on measures to restrict Beijing’s access to advanced technology. The Japanese government recently announced tighter regulations on semiconductor equipment exports to China.

China seeks to emerge as the leader of the next era of globalization, but its reputation is tarnished by efforts to displace Western firms from key markets and arbitrary actions against businesses and trade partners. Beijing sees export control measures as a violation of the World Trade Organization’s rules; the Chinese government in retaliation launched its own review of imports from America’s largest chipmaker. Geopolitical factors have been weighing on Chinese exports, an important pillar of growth. This can be clearly observed in falling exports to competitor states (see above chart), despite domestic demand holding up relatively well in these markets.

The trend is starting to alter the business landscape. Firms’ interest in realigning supply chains has been growing. Companies are increasingly focused on building resilience to minimize security and logistical risks by shifting production to geopolitically aligned markets. Unlike the globalization cycle, manufacturing decisions are guided by government policies more than efficiency considerations. And this strategy carries its own risks: aside from higher costs, reshoring or friend-shoring will reduce diversification, making economies more vulnerable to economic shocks.

Fragmentation is becoming visible in foreign investment and financial flows. As tariffs and trade frictions rise, financial links also suffer. European nations are pushing for more stringent screening of foreign investments. Countries like Canada and Australia have blocked bids by Chinese companies for domestic corporations. In recent years, India has stepped up scrutiny of Chinese foreign direct and portfolio investments to avoid takeovers of domestic firms. Foreign direct investment (FDI) has already become a casualty of increased fragmentation, with flows more concentrated among geopolitically aligned states and strategic sectors.

Developing and emerging economies will be among the biggest losers from the emergence of geopolitical blocs or fragmentation of FDI flows. Many EMs rely heavily on foreign investments from advanced economies which often are not geopolitically aligned and have been major sources of foreign investments. FDI fragmentation will lead to large output losses, to the tune of 2% of global output, according to the International Monetary Fund.

The economic costs of fragmentation will be far greater than any benefits. Declining global cooperation will shrink the world economy, especially hurting low-income nations. Estimates of the long-term loss from technology decoupling range from 7-12% lower global economic output. Higher costs and lower productivity will complicate central banks’ efforts to tame inflation.

While the world is becoming more fragmented politically and economically, we are hopeful that it is not the beginning of the end of globalization. Economic considerations such as efficiency and corporate profits will continue to hold significance in production decisions.

Huge potential losses from growing fragmentation underscore why global integration needs robust defense, but with a different strategy that caters to all sections of society. Given the evolving nature of economies and challenges, the existing globalization model also needs to evolve. But the solution on offer is not going to fix the problems. It will only feed more discontent.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice, or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© Northern Trust

Read more commentaries by Northern Trust