A Skip, Not a Stop

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSomething Worked

“A Whole New Economic Playing Field”

Nebulous Target

Root Cause: Fantasy

Cancun, Memphis, Dallas, Europe, and Paris

A year ago, the US Consumer Price Index was rising at an almost 9% annual rate. The Federal Reserve was trying to change that trend with tighter policy. But it wasn’t just the Fed. All of us—businesses, consumers, everyone—responded to the pain.

Good news: Our collective decisions seem to have had the desired effect. Annual CPI inflation dropped to 4.1% as of May and the last few months seem to be pointing even lower. The Producer Price Index is similarly retreating, which might reduce some of the cost pressures which lead to higher consumer prices.

On Wednesday the Fed sent a confident signal by declining the opportunity to raise rates again. But no one should think the rate hikes are over. I expect Jerome Powell, who has now defined his legacy as an inflation fighter (at least in his own mind), to respond swiftly and aggressively if inflation starts moving higher again.

Yet in one sense, Powell doesn’t have to “respond.” Simply keeping rates where they already are is additional tightening that should reduce or at least stabilize inflation. The problem is that various measures of inflation conflict. One says the Fed should stop raising rates and others suggest we may need more rate increases, or at a minimum higher for longer. Today I’ll explain how that works and what it means for inflation and interest rates.

Something Worked

Let’s start by reviewing some context. Early 2020 brought the deep but brief COVID recession, along with historically aggressive fiscal and monetary stimulus. By 2021 the economy was bouncing back.

But that’s an understatement. The economy didn’t just bounce back; it came roaring back as the stimulus money and pent-up demand ignited a frenzy of activity. Labor shortages and supply chain issues kept producers from filling the demand, sparking price inflation. Then the Ukraine war raised energy and food prices, sending inflation higher still.

I and many others criticized Fed officials for not responding sooner, but in March 2022 they finally started raising rates (coincidentally as Powell was in the process of being confirmed for a second term). It was always questionable whether higher rates were the best weapon against this kind of inflation. Nonetheless, the latest data shows something, or more likely a combination of many things, seems to have worked.

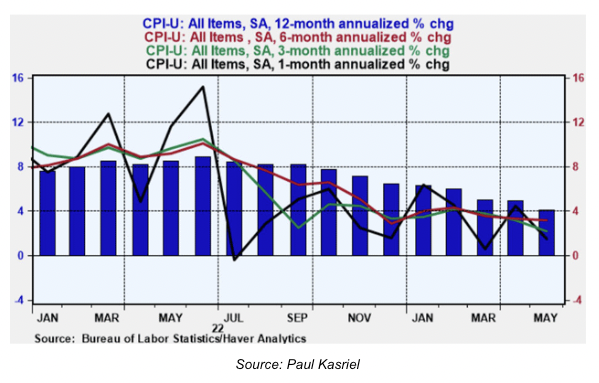

Here’s a good chart from Paul Kasriel comparing annualized CPI over four different time frames.

The shorter periods are naturally more volatile, but they all point to the same conclusion. Headline CPI inflation peaked in summer 2022 and declined steadily since then. Kasriel says tighter Fed policies made commercial banks reduce lending, which reduced demand, which reduced inflation.

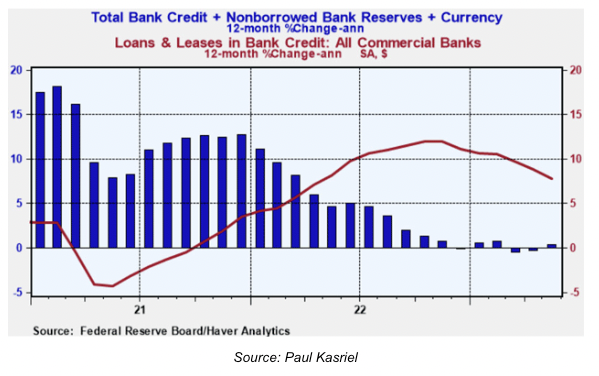

The red line in this next chart is key. When bank credit turned down, inflation did, too.

Of course, the Fed isn’t the only factor here. As I said in my opening, inflation itself changed everyone’s behavior in big and small ways. Higher interest rates gave people—particularly debtors—additional inducement.

I think we should all take a bow, frankly. This inflation on the heels of COVID has been one of the greatest economic challenges in decades. It’s not over but (knocking on wood) we seem to have avoided the worst-case possibilities.

Which is good because our other challenges were already serious enough.

“A Whole New Economic Playing Field”

Kasriel expects the FOMC to hold rates steady until late this year, by which time he believes a recession will have started. Then the Fed will start cutting rates, once again using the only tool it has.

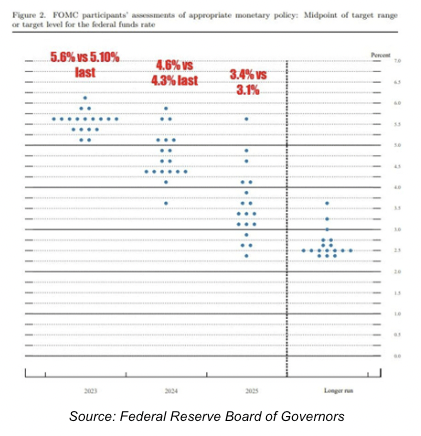

I think that’s a plausible scenario, but I also see a real chance for more rate hikes first. If job and wage growth continue the Fed will have to wonder if the economy is still running too hot. The newest dot plots show they still project two more quarter-point hikes this year (out of four remaining meetings). Skip, jump, skip, jump?

Powell took a lot of (justifiable) criticism for letting inflation fester too long. He needs credibility above all else. As I read the tea leaves, he won’t want to risk letting inflation return. And, as I’ve noted often, he is keenly aware of his 1970s predecessors who proclaimed victory over inflation too soon.

However, there’s another angle to this. Simply keeping rates steady at this higher level is itself further tightening. The effects spread more widely as time passes. Peter Boockvar described the process in one of his pre-FOMC letters.

“Just keeping rates at high levels for longer is a continued form of monetary tightening as each day that passes someone's adjustable rate mortgage resets much higher, someone's commercial real estate debt is coming due at an interest rate on offer more than double on the loan that is maturing, some businesses debt needs to be refinanced also at a much steeper rate, and some project or business doesn't get started because more equity is needed because the cost of capital is too high to make the numbers work, each and every day from here. And each time it happens, more cash is allocated to interest expense than something else or some business doesn't make it. Throw in the ever-growing needs of the US government who is now crowding out the private sector and this is a process of tighter money and less financing availability that will take years to play out, again assuming the Fed is committed to keeping rates higher for a while.

“To my continued point of the new rate world we're in and the high costs of it, if you didn't see the WSJ article over the weekend titled Startups Struggle to Stay in Business as Funds Dry Up, the piece said ‘Fresh capital from venture investors and bank loans is scarce and expensive. Going public is near impossible. Some business models that worked when cash was cheap are unsustainable now. That means venture-backed startups are running out of money and facing hard choices.’

“The credit crunch is here, and this will take not quarters, but years to play out if the cost of capital remains high. Understand too that many small and medium sized businesses have to pay an interest rate on a loan that is above 10% if they can even get one. Things in the private economy worked ok at 3‒4% interest rates, not so much at 10% as we're on a whole new economic playing field that I don't think is being fully appreciated.”

Read that quote two or three times. An entire generation of investors and business leaders has never known a capital-constrained economy. Can they adjust? Probably, but not easily or instantly.

Another aspect of this is the change in real interest rates. “Real rates” are inflation adjusted, since inflation lets you repay with depreciated money. If your nominal rate is, say, 7% and inflation is 5%, your “real” rate is 2%. Until recently real rates were mostly near zero or even negative, which helped incentivize the debt that’s becoming problematic.

If a) the Fed keeps nominal rates steady or higher and b) inflation keeps falling—both of which seem likely at least over the next few months—real interest rates will rise, aggravating the process Peter Boockvar describes. That process eventually leads to recession if allowed to go on too long. But then Volcker had no issue putting us into two recessions.

Powell needs to keep policy on a narrow path. Cut too soon and inflation could return. Wait too long and the inevitable recession will be worse. That’s tough no matter what, but even more so when he’s flying blind.

Nebulous Target

In this week’s statement the FOMC reiterated its 2% inflation target. Having a target is good and necessary to guide policy decisions. The problem is this target is more like a nebula: fuzzy, irregular, and ill-defined.

The first problem is that inflation affects everyone differently depending on how they spend their money. Your cost of living is different from someone with a different occupation and family situation who lives in another state. A policy that helps one of you may hurt the other. Then multiply that by millions of households and businesses.

But beyond that, knowing an accurate inflation rate requires measuring things that don’t want to be precisely measured, like housing prices. Aside from the “all real estate is local” aspect, benchmarks like CPI have to wrestle with timing questions. Renters typically sign a year-long lease, during which their rent stays the same. Someone in the identical apartment next door may pay considerably more or less if they moved in a few months later. How do you reflect that in national-level data?

The answer, at least for CPI and PCE, is to amortize rent price changes over a one-year period. That makes a kind of superficial sense, but it takes a long time to reflect changes. The same happens in owner’s equivalent rent, which uses local rental rates to separate the “investment” part of your home’s value from the “service” you receive in having a place to live.

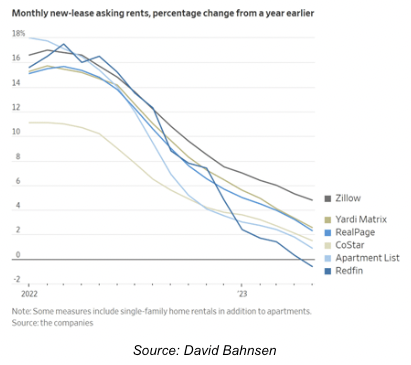

This methodology kept CPI from reflecting rapidly rising housing costs in 2021. Now it’s going the other way. Private data trackers show rental rate growth slowing sharply across the country. Here’s a chart David Bahnsen shared.

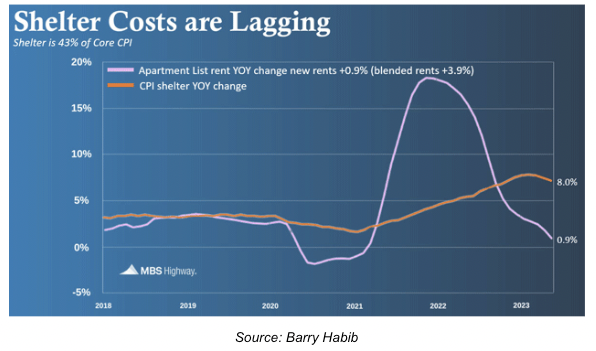

If your lease came up for renewal in early 2022 the new rate was, on average (and with giant local variation) around 15% higher than a year earlier. That’s serious inflation, given that rent is the largest single expense for many families. Yet at that point the Fed was still sitting on its hands because this was affecting inflation benchmarks only in small incremental steps.

Notice this next chart (from Barry Habib) shows that time lag. Rents were rising dramatically in 2021 but didn’t show up in CPI because of that 12-month lag.

Let’s go back to that chart showing 6 measures of housing inflation from David Bahnsen. Quoting:

“Blending the six measurements together has rent price inflation year-over-year at +1.9%, down from +14% the year prior, the largest drop in residential price inflation in any year they have ever measured. Redfin, by the way, which includes single family residence and not just apartments, shows actual price deflation year-over-year. Use +1.9% as a shelter inflation (and that is the HIGH end), and it takes 2.16% OFF of the 4% inflation rate, so, voila, you are at the Fed’s 2% target.”

Dave Rosenberg, who has stayed on “team transitory” through this whole era, thinks inflation is effectively done, except in rents and used cars. Yet a majority of FOMC members, knowing full well about “lagging effects,” still say they want to hike rates another 50 basis points this year. Why? Well, they are not looking at CPI but PCE (Personal Consumption Expenditures). And PCE gives a different picture.

My friend Barry Habib sent me this note (emphasis mine):

“Inflation isn’t easy to measure, but it doesn’t have to be that hard either. We have seen inflation, as measured by headline CPI, drop dramatically from 9% to its current level of 4%. But coming on July 12, with the release of the June CPI data, we expect inflation to decline significantly to 3% on a year-over-year basis. With a little luck, we may even see a 2-handle. This is reflective of lower monthly inflation readings, but mostly due to the way year-over-year CPI works. As new data is released, it replaces the corresponding month’s data from the previous year. The new June data for 2023 will replace a very elevated 1.2% reading for the month of June 2022 alone.

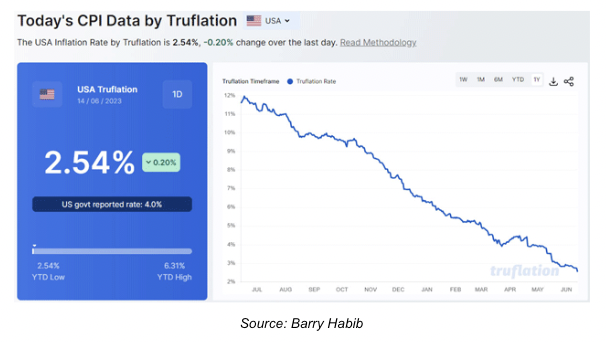

“…Inflation is coming down, but it depends on how it’s measured. CPI considers 80,000 data points, much of them lagging, but inflation, as measured by the folks at Truflation, considers 10M data points in real-time, showing inflation around 2.5%.

“At the latest Fed meeting, it was very clear that Jerome Powell and the Fed now want to see an inflation reading of 2% on core Personal Consumption Expenditures (PCE), which has a lower weighting on shelter costs and is a bit different than CPI. The current core PCE reading is 4.7% year-over-year…so there’s a long way to go to reach 2%. As mentioned earlier, when each new month’s data is released, it replaces data from the same month in the previous year. According to our math, core PCE will make progress towards about 3.7% by the end of 2023, but nowhere near the 2% the Fed wants… Remember, to get to 2% year-over-year, you’d need an average reading of 0.166% per month; that’s very hard to do.”

If the measure they prefer shows inflation in the high 3% range, even if CPI has a comfortable “2-handle,” that is enough to make them stay higher for longer. And maybe even raise rates again and then again as their dot plot shows. Ugh.

The net effect of having this subjective committee make subjective decisions about a subjective goal will likely mean they once again act too late. Just as they let inflation get worse than it had to be, they will (potentially) keep policy “higher for longer” and perhaps even raise rates and let the next recession cut deeper than it otherwise would.

Root Cause: Fantasy

For better or worse, the Fed seems bent on getting real interest rates firmly into positive territory. One could argue this will ultimately be for the better, short-term pain notwithstanding. Let me explain.

Last summer I shared some excerpts from Edward Chancellor’s masterful book The Price of Time. Chancellor surfaced an 1856 Walter Bagehot quote on how the average Englishman (“John Bull” in the time’s colloquial term) reacted to low interest rates.

“Whenever money becomes very cheap, experience teaches us to expect that it will be misspent. John Bull, as has been wisely observed, can stand a good deal, but he cannot stand two percent. The particular form of mania differs in various years; but when the common and tried employments of money yield but a low profit, recourse will be had to new and untried ones, some of which will be unprofitable, and a few of which will be absurd. It is only at the outset of such manias that warning is of the least use—when they attain a certain growth, advice is thrown away. Everybody is seen speculating; and what everyone does must be judicious. Foolish person No. 2 imitates foolish person No. 1.”

In other words, when people can’t make a decent return investing their money at interest, they are drawn to risky and sometimes shady speculations. This is what produced the South Sea Bubble, Tulip Mania, and similar crazes.

Now, think about our own time. We used to have a “risk-free rate of return.” You could buy Treasury bills or bank CDs and make a safe, guaranteed return, often 5% or even more. Inflation cut into it, but anyone could still make a positive return without undue stress (as opposed to the “return-free risk” of the last 10‒15 years).

This was important in ways I’m not sure we appreciated. We all just assumed 5% returns on short-term Treasuries and bank deposits were normal. Everyone, even the least-educated laborer, had the opportunity to save their money and watch it grow. A basic level of capitalism was open to all. You could start slowly and expose yourself to losses only when you felt ready.

That is no longer the case. And it’s probably not coincidence much of post-2008 “capitalism” is no longer worthy of the name.

Moreover, artificially low interest rates produce malinvestment. They fund marginal ideas and projects that would be quickly rejected if they had to justify real-world financing costs. Those enterprises usually fail, but they survive long enough to keep many better ideas from ever seeing the light of day.

Even worse, the persistently low rates raised wealth and income disparity. Zero interest rates hurt retirees and savers and benefited people with money and access to opportunities.

The root cause of all this is the fantasy that a small group of elites can sit around a table and decide what capital should cost for everyone. That’s never going to work very well. It has some benefits; modern central banks have prevented the kind of financial panics that were common before the 20th century. But that benefit has come at great cost.

I think we could probably find a better way. But we won’t, until we decide to look for one.

One final thought: We last adjusted how we measure housing inflation in the early 1980s. Technology and data collection has vastly improved in the last 40 years, but the government and the Fed, with all those economists, have not updated our housing inflation measures.

Given how this has clearly, obviously, manifestly distorted monetary policy, you would think there would be serious effort to develop better inflation data. But if we did that, it would narrow the path choices the Fed has. Now they can do whatever they want and simply say we are data dependent. Except the data they “depend” on is clearly dysfunctional, if not outright misleading. And if they think that data truly reflects reality, then gods help us.

Cancun, Memphis, Dallas, Europe, and Paris

Shane and I will be in Cancun at the end of the month where my son Henry is getting married and I'm his best man. Then we will be at Freedom Fest in Memphis July 12‒16, speaking several times and meeting with friends and clients. If you are there, I would love to meet you.

We will be in Dallas in early August and the plan is then we travel to Europe in early September but with the focus on being at Charles Gave’s 80th birthday September 9 in Paris. I am open to speaking opportunities. (It is also Gavekal’s 25th anniversary.)

I am here in Nashville to speak with a group of extraordinarily bright young portfolio managers at Ashler Capital, an equities investing business at Citadel, one of the world’s most successful hedge fund firms. It is both quite exciting and intimidating. I always learn more than I impart. Good times and I want more of them. Just like the “old” days.

It is time to hit the send button and wish you well! Have a great week and don't forget to follow me on Twitter!

Your frustrated with nearly all things government analyst,

|

John Mauldin Co-Founder, Mauldin Economics |

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All