My first job as an economist was in litigation consulting, digging into the data in a lawsuit to determine the veracity and consequences of allegations of illegal behavior. And when the LIBOR matter arrived at our firm, I couldn’t believe the claim. Was it possible that a core component of the financial system had been manipulated? As I dug into the data, I witnessed the dispersions: LIBOR was not what it claimed to be. And at long last, the prolonged dispute is approaching its final settlement.

In its original form, the London Inter-Bank Offered Rate was a surveyed measure. Each day, a set of bank representatives gave responses to the following prompt: “The rate at which an individual Contributor Panel bank could borrow funds, were it to do so by asking for and then accepting inter-bank offers in reasonable market size, just prior to 11.00 London time.” At its peak, the survey asked for rates in ten currencies and up to 15 maturities.

The prompt reveals LIBOR’s fundamental problem: it was fiction. Respondents did not need to base their answers on any real transactions, only the rate they claimed they could receive from a counterparty. No evidence was required. Actual trades in many of the currencies and terms were scarce, as most bank funding transactions are conducted overnight.

But market participants did not scrutinize the methodology, welcoming LIBOR as a unique and useful reference rate from which to price any number of transactions. From modest and informal beginnings in 1969, use of the rate grew to a more formal survey panel conducted by the British Bankers’ Association (BBA) in 1986. The BBA conducted the survey of 18 international banks every day. The BBA methodology was a trimmed-mean average: the four highest and lowest observations were excluded, and the average of the remaining submissions became the day’s LIBOR rate. Market participants would then price their bonds, lines of credit and any number of structured finance products using a spread to LIBOR.

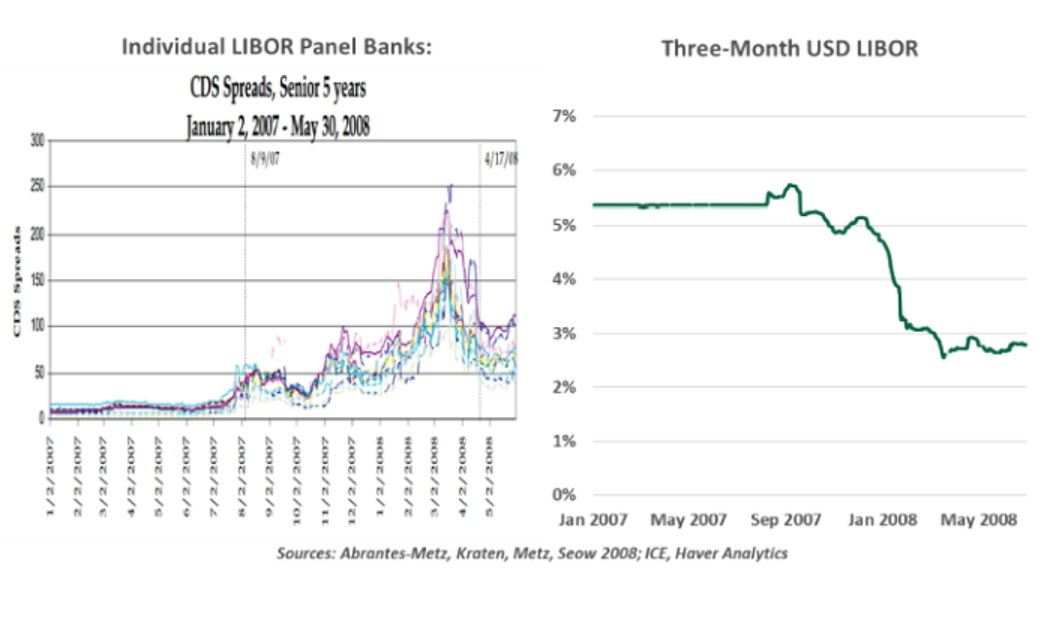

LIBOR was a crucial piece of the financial fabric until 2008, when researchers found disparities when comparing BBA panelists’ steady estimates against their banks’ rising risks. Banks’ credit-default swap (CDS) spreads were rising, reflecting justifiable worries about each firm’s condition, which should have elevated their funding costs; however, their LIBOR submissions did not increase. Targeted regulatory investigations then revealed evidence of traders explicitly asking their BBA representatives to submit particular LIBOR bids; these investigations would yield fines totaling over $9 billion. Motivations were simple: In the heat of the financial crisis, banks did not want to show weakness by standing out with high funding rates. And several fixed income strategies could reap material gains with interest rate movements of just a few basis points.

Cleanup work ensued. Starting in 2014, the Intercontinental Exchange took over LIBOR (rebranding it to Libor), using a new methodology based on actual funding transactions. Still, underlying data was thin, and confidence was shaken. New reference rates were needed.

Globally, committees convened to devise replacement reference rates: In the U.S., the New York

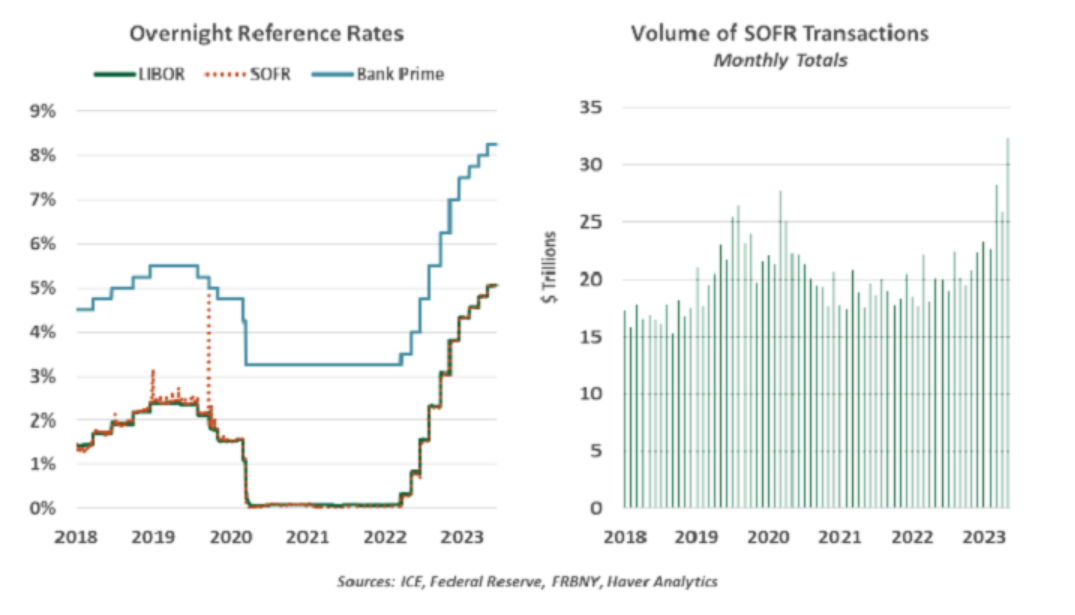

Fed publishes the Secured Overnight Funding Rate (SOFR) based on overnight repurchase (repo) transactions. The European Central Bank settled on a similar Euro Short Term Rate (€STR), while the U.K. relies on the Sterling Overnight Index Average (SONIA). Lenders are free to choose other proxies, such as the Federal Reserve’s Bank Prime Loan rate, which is based on a survey of bank commercial loan rates.

But the limitations of LIBOR foretold the complications facing its replacements. Rates must be rooted in actual transactions, but funding deals are primarily overnight. The term structure of LIBORs had no ready replacement, but term rates were important to be used as a base rate for a variety of contracts. Thus, an effort began to recreate the term structure. Term SOFR uses the pricing of interest rate futures contracts to set rates in one-, three-, six-, and twelve-month tenors. While these term rates have a limited history, they are meeting a market demand.

The new rates also differ in their collateral. LIBOR was an unsecured borrowing rate. SOFR is based on rates paid in repo transactions, in which U.S. Treasury securities are pledged in exchange for cash. These transactions are fundamentally lower risk than unsecured borrowing. While this accurately represents the mechanics of interbank funding, the analogy becomes strained when applied to other forms of lending. The loans and credit structures that priced relative to LIBOR have an array of terms and covenants that differ from interbank lending.

Now, the moment of truth for these alternative rates is upon us. Fifteen years after the allegations were first published, LIBOR will meet its end. Friday, June 30, 2023 will be the last day banks will be expected to submit the prices that feed into LIBOR. This will be the final step in LIBOR’s dismantling: reference rates for five minor currencies were terminated in the initial reforms, and LIBORs for the euro, pound sterling, yen, and Swiss franc ended in 2021. Only the U.S. dollar LIBOR is still standing, but not for long.

Work has been underway to move away from LIBOR for a long time. However, sunsetting a structural part of the financial system is no small task, with more than $300 trillion of financial products formerly tied to the rate. Some contracts were especially challenging, offering no provision for replacing the reference rate. To address these “tough” contracts, Congress passed a funding bill in 2022 that granted a blanket authorization to replace reference rates with a set of rates to be determined by the Federal Reserve. The Fed has since endorsed Term SOFR as the new standard.

The LIBOR saga offers a few lessons that extend beyond the realm of fixed income. First, it’s important to understand the market mechanisms we rely upon. LIBOR was an unsteady foundation for a massive financial enterprise. Are there other data points or market structures that might not be fully understood or used for the correct purpose? More encouragingly, the concerted, industry-wide effort to replace LIBOR shows that even difficult changes are possible. Reforms can be slow and costly, but greater stability and certainty are worthwhile ends. And though I gained valuable experience as a consultant, I will support any outcome that avoids complex litigation.

Ryan James Boyle is a Senior Vice President and Senior Economist within the Global Risk Management division of Northern Trust. In this role, Ryan is responsible for briefing clients and partners on the economy and business conditions, supporting internal stress testing and capital allocation processes, and publishing economic commentaries.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions. © 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© Northern Trust

Read more commentaries by Northern Trust