Low commodity prices are containing inflation in emerging markets.

Dr. Karl Otto Pöhl, a German economist and a former President of the Bundesbank, once said: “Inflation is like toothpaste. Once it’s out, you can hardly get it back in again. So, the best thing is not to squeeze too hard on the tube.” The quote was in reference to his struggle as a central banker in the early 1980s, trying to bring German inflation under control.

Four decades later, there is a renewed struggle to contain inflation. In a reversal of traditional roles, emerging markets (EMs) are having better success in this effort than their larger cousins.

Responding to the pandemic, governments pursued extraordinary fiscal and monetary policies. Such measures created supply and demand imbalances, driving consumer prices higher. The war in Ukraine further aggravated the inflation shock. More restrictive economic policy has helped to drive inflation down from uncomfortable peaks. However, the process is taking longer than expected, especially in advanced economies (AEs).

Historically, inflation in EMs has exceeded that of AEs. Yet price rises in the developed world are running ahead of those in developing nations. Headline inflation across Asian economies moderated to a 20-month low of 2.1% year over year in May, which is half the pace of U.S. price increases and about one-third of those seen in the eurozone. China is staring at potential deflation, as consumer prices have essentially stagnated on a year-over-year basis. Major emerging economies like Brazil and India have lower inflation than Europe does.

A number of factors explain why EMs are witnessing more rapid disinflation than their advanced counterparts. The composition of emerging market consumer price index (CPI) baskets is one of the more important ones. Food alone carries weights of over 40% in the CPI for some emerging economies. If energy is brought into the picture, you have half or more of the inflation basket. By contrast, volatile food and energy components represent less than a third of the CPI basket in North America and Europe.

This means that inflation in the developing world is largely a function of global commodity prices, and also explains why inflation expectations are generally less anchored in EMs. When global commodity prices rose sharply, they created a larger surge in inflation for the developing world than for advanced economies. Over the past year, however, falling commodity prices have fostered faster disinflation in EMs.

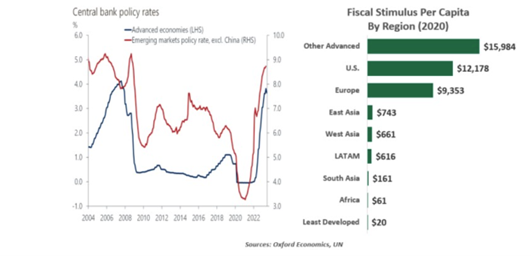

While the fading commodity shock has played a significant part in bringing inflation down, the early response of EM central banks to the threat of rising prices has also helped limit the problem. Many EMs tightened monetary policy starting in early 2021, a year sooner than most of their advanced counterparts. Their tightening was often more aggressive, thereby helping anchor inflation expectations.

Central banks in emerging markets were able to achieve their inflation objectives without creating financial instability. The tightening of monetary policy around the world has often triggered financial stress or even crisis in EMs, due to higher credit and currency risks. This was the case in the 1980s, the mid-1990s, and to a certain extent in 2013.

Improving frameworks, credibility, and proactive actions have allowed developing economies’ central banks to withstand policy tightening without inciting major turmoil at home. This time around, developing nations were able to avoid large capital outflows and significant depreciation of the local currency. The latter has historically been a significant contributor to inflation in EMs.

Services inflation, the stickier component in many developing economies, has also been more subdued when compared to North America and Europe. Labor markets are not as tight in the emerging world, limiting the kind of wage growth that produces upward pressure on service prices.

Varied fiscal responses to the COVID shock also help to explain the difference in inflation experiences. Advanced economies’ average fiscal support amounted to about $12,000 per capita, compared to as little as $20 in the poorest nations. EMs were thereby able to avoid the kind of demand-supply gaps that are prolonging inflation in higher-income economies.

Disinflation has been faster in EMs during the current cycle, but smaller economies remain more vulnerable to upside inflation surprises given higher exposure to domestic and exogenous shocks. El Niño poses risks to global food output and prices. Structural inefficiencies, such as poor infrastructure, will continue to exert upward pressure on prices in developing countries by raising production and transportation costs.

And economic reforms have been uneven across nations. While monetary policy frameworks have improved in recent decades, central banks in countries like Turkey and Venezuela remain subject to frequent government interventions.

With peak inflation likely behind us, the current tightening cycle is approaching its final stages for some emerging economies. But EM central banks cannot lower their guard and should be on the lookout for upside inflation surprises. For developing countries, maintaining tight policies and strong frameworks will remain the key to keeping toothpaste in the tube.

Information is not intended to be and should not be construed as an offer, solicitation, or recommendation with respect to any transaction and should not be treated as legal advice, investment advice, or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulations. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our white papers.

© Northern Trust

Read more commentaries by Northern Trust