Supply chains are realigning, to China's dismay.

“Digging to China” is a classic parental joke in America. Any kid with a shovel in their hand in the yard has probably been told that if they dug a hole and kept going, they would eventually reach China. The phrase was often featured in cartoons where characters actually dug their way to an Asian country. In the book Walden, Henry David Thoreau wrote that “there was a crazy fellow once in this town who undertook to dig through to China, and he got so far that, as he said, he heard the Chinese pots and kettles rattle.”

One doesn’t have to dig that deep to see how rattled the Chinese economy is today. A month ago, Carl highlighted how China’s reopening surge had hit the wall. Economic woes have only piled up since.

A couple of years ago, firms and governments expressed intentions of changing supply chains in the wake of pandemic-related disruptions. But many believed that the process would be slow, as companies would give precedence to profits over geopolitics. The hard data suggests corporations are not only acting on these intentions but moving quite swiftly indeed.

Recent trade data shows that China’s status as the world’s largest exporter, which was further enhanced during the pandemic, is now under threat. China’s exports fell for the third month in a row in July. The 14.5% year-over-year contraction was the biggest drop in more than three years, with declines among most of its major trade partners. Shipments to the U.S. fell for the twelfth consecutive month. Exports to both the European Union (EU) and to the Association of Southeast Asian Nations declined by 21% during the year.

China’s exports to Western markets are dampened, in part, by weaker demand. However, an acceleration in supply chain re-routing in the face of rising geopolitical tensions is also a key factor, as Western corporations are increasingly reassessing their China exposure. U.S.-China trade flows demonstrate this clearly.

Despite a weaker renminbi (RMB), China's exports to America plummeted by 25% in the first half of 2023, compared to only a 7% decline in U.S. goods imports from the rest of the world. Beijing’s politically sensitive trade surplus with Washington narrowed by 27% to $30 billion. For the first time in 15 years, China is no longer the top provider of goods to the U.S.

As the flow of goods from Beijing into America declines, imports are growing from nearly every United States ally. Mexico and Canada have each individually surpassed China as the U.S.’ leading sources of imported goods. This is a huge decline for the country that five years ago accounted for more than a fifth of all American goods imports. The European Union is also trying to de-risk by reducing its reliance on Chinese imports but has struggled so far. China has remained by far the largest supplier of goods to the bloc this year.

The decline in sourcing from China has been incentivized by the U.S. administration’s industrial policies, such as the CHIPS and Science Act, which aims at attracting firms to invest in America. Restrictions such as the Uyghur Forced Labor Prevention Act, which supersedes a series of individual import bans, are also discouraging U.S. businesses from sourcing products from China. Imports of products like cotton and polysilicon (used widely in the solar panel industry) are facing greater scrutiny under this act.

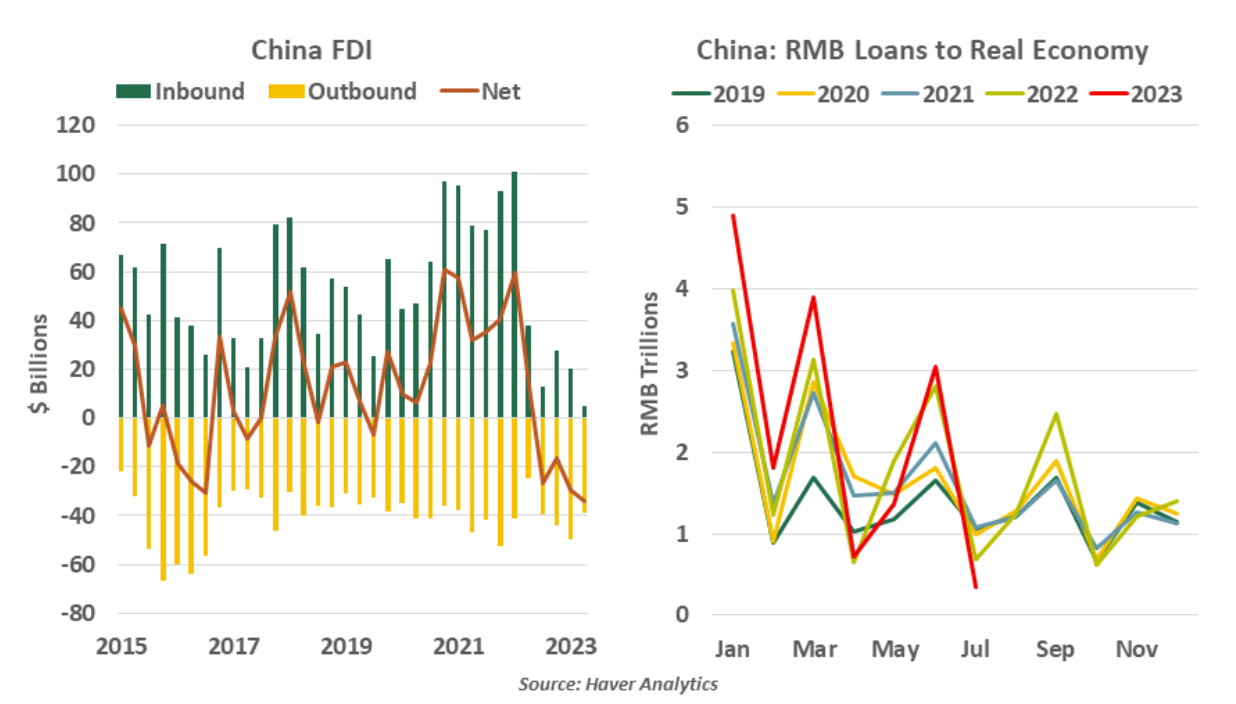

Foreign direct investment (FDI) into China fell to a record low in the second quarter of 2023. Only $4.9 billion was invested in the country, down 87% from the same quarter last year and the lowest level since records began in 1998. Restrictions on Beijing’s access to advanced technologies are redirecting investment flows away from China. The sharp decline in FDI is also painting a calamitous picture for exports as “exports by foreign companies operating in China account for about 30% of China’s total exports”, according to Nomura.

Falling exports, a huge source of revenue for Beijing, are going to have wider implications. Exports were providing much-needed support to the Chinese economy as it grappled with stringent lockdowns and a tumbling property market. Millions of small firms are now struggling to stay afloat due to the drop in earnings. China’s domestic demand has remained lackluster. July imports suffered from declines across both consumption- and capital-related goods.

Lower demand for Chinese goods has led to a slowdown in production and investment, contributing to a deflationary environment. A protracted period of falling prices will dent corporate profits and consumer spending, exacerbating debt burdens. RMB loans to the real economy have plummeted to their lowest level since 2006, underscoring the weak domestic demand and the need for further stimulus. Slower growth will only generate higher unemployment and further deflate both asset and consumer prices.

China’s massive real estate sector, where the majority of household wealth is parked, is a large and growing headwind. Last week, one of the country’s largest property developers missed interest payments on its external debt. Though the company carries a lower debt burden than Evergrande, the timing of this occurrence is quite concerning, as the trouble is brewing at a time when policies are already being eased. News of a leading Chinese trust company missing payments on several investment products over the weekend has added to the fears that the economic slowdown may trigger a liquidity crisis beyond the real estate sector.

These are testing times for the Chinese economy. The policy stimulus measures implemented so far have been insufficient to spur a meaningful economic recovery. But there is not much more that Chinese policymakers can do about it. They cannot count on government stimulus and exports to turn things around.

Interestingly, if one started digging in Beijing and burrowed 12,000 kilometers to the other side of the earth, you would emerge in Argentina. As China stares into its economic hole, that is not a destination it wants to reach.

Information is not intended to be and should not be construed as an offer, solicitation, or recommendation with respect to any transaction and should not be treated as legal advice, investment advice, or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions. © 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulations. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Northern Trust

Read more commentaries by Northern Trust