Despite softening demand, US home prices remain elevated. The culprits are high interest rates, limited supply and owners' reluctance to take on new mortgages.

A lot has been written about the US housing market of late, but you’d be forgiven if it’s all as clear as mud. To untangle the unusual dynamics of a market often seen as a bellwether of US economic growth, we need to rethink traditional expectations of how interest rates affect housing supply and demand.

On one hand, sales volume is way down. “Rock bottom,” said Glenn Kelman, CEO of real estate brokerage Redfin, adding that the only ones moving from their homes are those who absolutely have to. On the other hand, prices remain elevated—especially in supply-constrained markets where bidding wars are still the norm and good deals are hard to come by.

So, does that mean the housing market is weak or strong? Yes.

Defying the Laws of Supply and Demand

If we told you a year ago that the Federal Reserve would hike the Fed funds rate by more than 5% but that US home prices would be down only marginally, you’d likely have thought we lost our marbles.

But that’s exactly what happened.

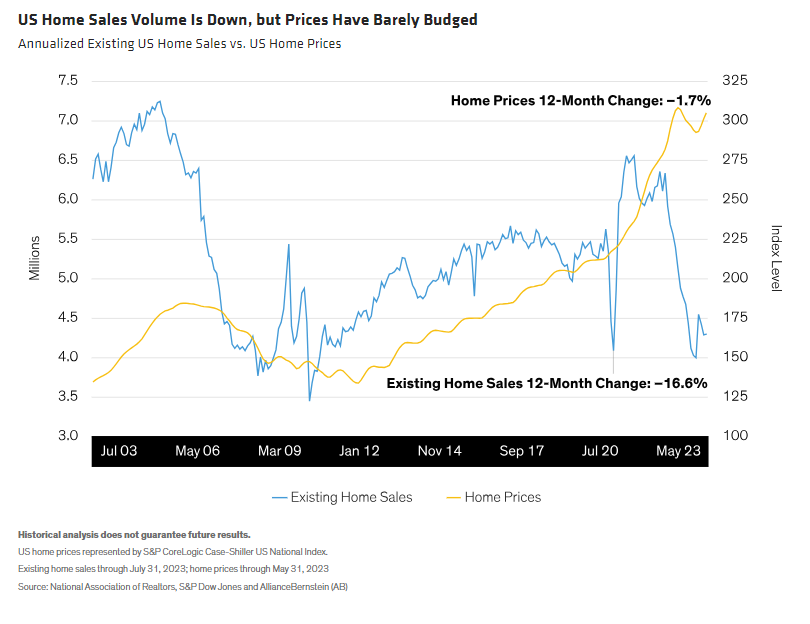

Sales of existing US homes are down nearly 17% since last July, according to the National Association of Realtors. But home prices, as measured by the S&P CoreLogic Case-Shiller US National Index, are off just 1.7% since last May (Display).

Normally we’d assume that higher interest burdens would deter home-buying activity. But demand has remained surprisingly robust—propping up the US economy more than many would’ve expected.

In its efforts to tame surging inflation, we believe that the Fed hiked rates so quickly that tighter monetary policy constricted the supply of existing homes more than it dampened demand—contributing to today’s stubbornly high prices.

When the Best Strategy Is Staying Put

How did this happen? Consider that the average interest rate for a 30-year fixed-rate mortgage has risen from just 3.1% at the start of 2022 to around 7.6% today. Comparing average home prices in early 2022 against today’s prices—and assuming a 20% down payment—that comes out to a monthly difference in interest expense of around $1,200 per month. Few people want to move out of their current homes and give up low-rate mortgages, only to buy more expensive properties at higher rates.

Meanwhile, chronic underbuilding has exacerbated already-constrained inventories, which are still well below pre-pandemic levels. The net effect has been a downward shift in the supply curve, putting pressure on existing home sales.

Housing Reflects Broader Supply Trends

In some ways, US housing can be viewed through the same prism as other industries suffering from supply chain disruptions. We see parallels to the US automotive market, which saw supply chain issues constrict inventory during the pandemic, inflating prices for both new and used vehicles. The Manheim Used Vehicle Value Index soared a whopping 65% from pre-pandemic levels through 2021. Since then, it has fallen 17%, with momentum shifting further to the downside.

The turning point was when the auto industry ramped up production and began replenishing depleted inventories. We believe that the same will have to occur in the US housing market for prices to come down meaningfully.

Cutting Through the Clutter: What’s Ahead for US Housing?

Given the mixed signals, what can we expect from the housing market over the coming years?

Much depends on monetary policy. We believe that interest rates—and, by association, mortgage rates—are close to peaking in the US and will eventually stabilize near current levels. With rates still elevated, we don’t expect to see a dramatic surge in home purchases, but neither do we expect a significant weakening in demand.

As it has been for the past couple of years, the X factor will be supply. Given long-term inventory constraints, the US housing market needs rate stability to see a rebound in construction activity. Increased housing supply could contribute positively to economic growth, while preventing rising home prices from disrupting the broader disinflation process. If rates don’t rise much further—or if they don’t drop dramatically—the housing market could contribute to the relatively soft landing that we currently forecast.

In the meantime, we expect the housing market to defy historical norms. As cities regain their footing and core inflation cools, we expect to see housing prices hover at lofty levels, even if sales volume fails to impress. Ultimately, the Federal Reserve and homebuilders could hold the keys to the American dream.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© AllianceBernstein

Read more commentaries by AllianceBernstein