Spillovers From China’s Malaise

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsA hard landing in China would rattle Asian economies.

There is an old cliché that if the U.S. sneezes, the world catches a cold. It is used to highlight the spillover effects of trends in the world’s largest economy upon other parts of the world.

With China’s rise as an industrial powerhouse, developments there have broad global consequences. But I would propose an alternative cliché: when China’s economy feels the heat, the world sweats.

After four decades of robust performance, China’s economic growth is slowing and the soft patch is unlikely to be transitory. As we wrote here and here, the Chinese economy faces a series of challenges that will be difficult to manage.

China has become a dominant worldwide player across a number of sectors. The country is the world's largest manufacturer and exporter of goods. Supply chains for many industries are rooted in the country, earning it the title of the world’s factory. China is also the world's largest purchaser of several key commodities, consuming about half of the global supply of basic metals and one-fifth of the global oil supply.

With Western nations expected to slow in 2023, the International Monetary Fund projected that China would account for over one-third of global growth this year. That forecast is unlikely to be realized.

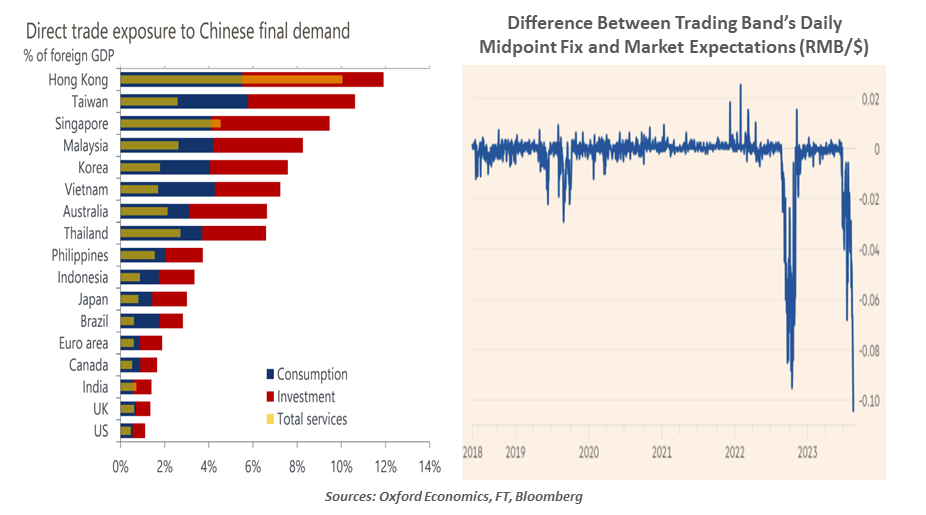

China’s economic woes are sparking warnings of contagion to other parts of the world. China’s regional trading partners, along with commodity exporters, are especially exposed to its waning consumer and industrial activity. China is a key trading partner for south Asian economies, not only in goods but also in services such as tourism. The commercial hubs of Hong Kong and Singapore are especially vulnerable, given that Chinese demand accounts for 13% and 9% of their gross domestic product (GDP), respectively.

South Korea’s exports fell in July at the steepest pace in more than three years, while factory activity there fell for the 14th month in a row in August on the back of smaller shipments of computer chips across the Yellow Sea. Vietnam, a key exporter of textiles, footwear and electronics is witnessing similar trends, with its shipments dropping 14% in the second quarter from a year earlier.

The Chinese property sector has been a significant source of demand for building materials. The current downturn in the industry means it requires less industrial metals like iron ore and copper. Even distant nations will feel the burden: Zambia exports 20% of its metals to China, as well as 10% of metals sent from Chile.

China is the most important destination for Australian and Japanese goods. Australia’s trade surplus shrank more than expected in July as weak demand in China weighed on the exports of commodities like iron ore, lithium and natural gas. The Australian dollar is trading at its lowest levels in almost a year against the U.S. dollar as China’s economic prospects are being scaled back. Japan’s shipments to its largest trading partner registered a decline of 13% year-over-year in July, led by drops in exports of major items like automobiles and integrated chips.

Owing to relatively small trade exposure to China, the negative growth impulse to Western developed economies will be much more modest. Sales to Beijing account for only 4-8% of revenue for listed companies in America and Europe. Germany is an exception, as faltering demand from Asia’s largest economy is one of the reasons behind the economic stagnation in the eurozone’s largest economy.

Historically, financial spillovers from China to the developed world were thought to be negligible or non-existent due to the fact that Beijing maintained a closed capital account regime, with limited financial links to the West. Some, like Nobel laureate economist Paul Krugman, are still of the view that even a 2008-style crisis in China is unlikely to lead to major global spillovers. But given the country’s deepened integration into the broader global economy in recent years, a hard landing scare could generate spikes in global financial volatility.

Mounting concerns over the health of the Chinese economy and the widening interest rate differential with the U.S. have put pressure on the renminbi (RMB). The currency has dropped to a 16-year low against the dollar. The gap between expectations and the daily trading band’s

midpoint fix set by the People’s Bank of China (PBoC) is the largest since the survey began in 2018, which shows the discomfort at the central bank over the sudden fall (see above chart).

Haunted by the recent past, when foreign reserves dropped by around $1 trillion from 2014 to 2016, the PBoC has been hesitant to deplete its reserves in an effort to prop up the value of the currency. Instead, it has used other measures such as cutting the foreign reserve ratio to provide support to the RMB.

A weaker renminbi could offer some support for the Chinese economy, given the deflationary environment at home and falling exports. However, a significant depreciation will have unwelcome consequences. Sustained pressure on the RMB will add to debt in domestic currency terms, thereby likely increasing leverage. And it could raise accusations of trade manipulation from the United States and others.

2023 has been the hottest year on record around the world. But as China stares at rising economic risks, the heat it feels is especially intense. Its business partners may find it very difficult to stay in the shade.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions. © 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulations. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All