Strategic Income Outlook: The Watched Pot

The Watched Pot

The upcoming recession seems to be the proverbial “watched pot” that has yet to boil, and boy has it been watched! No matter how many millions of eyeballs are scouring the data investment pros, economists, CEOs, CFOs, purchasing managers, etc. — that pot just will not boil. Much to the chagrin of those who were loudly proclaiming that the recession would soon follow the yield curve inversion in early 2022, we are still waiting.

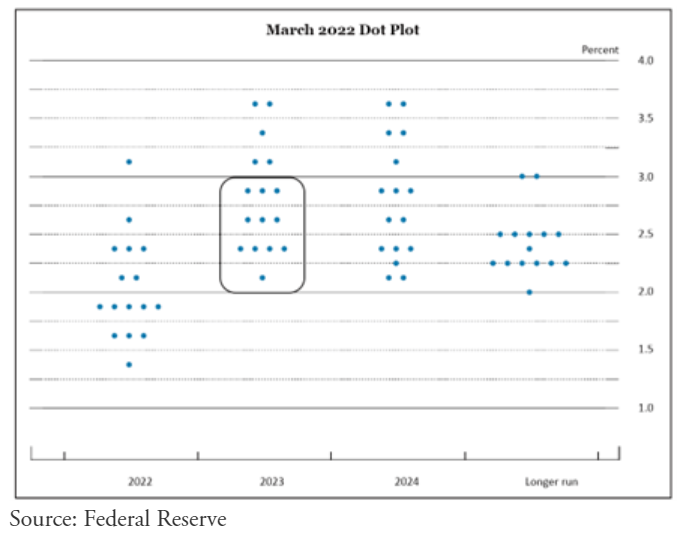

As you can see below, based on the Fed’s dot plot from the March 2022 FOMC meeting, most of the governors were expecting a fed funds rate below 3% by year-end 2023.

Clearly, those “experts” had a bit too much faith in the influence of their own policy decisions, even accounting for the typical lag. Alternatively, they may have initiated their tightening cycle too late to slow down inflation quickly, allowing expectations to become entrenched. Either way, unsurprisingly, the dot plots turned out to be quite inaccurate. As we have long maintained (and as history has repeatedly demonstrated), the dot plots are an unreliable indicator of future interest rates.

While segments of the economy have been affected by the new rate regime and are experiencing their own mini-recessions — commercial real estate, brick and mortar retail, telecom equipment, and parts of the health care market – they have failed to weigh heavily enough on the broader economy to pull it down. Investors who positioned their portfolios in anticipation of a 2023 Fed shift from hawkish to dovish (i.e., rate cuts) have been sorely disappointed. It seems that the one point that pundits and experts grossly underestimated was the ongoing strength and resiliency of the consumer, which is crucial as consumer spending makes up nearly 70% of domestic GDP. As we look at the data today, the consumer looks to be in much better financial shape than most would have guessed.

Those who were making the early recession calls were surely leaning on the assumption that the consumer’s financial strength would fade, and spending would promptly go into lockdown mode as the Fed embarked on its tightening path. Anyone who made that early call would likely understand that the process of hiking rates would eventually impact corporate spending and hiring, but that the effects there would be felt as an evolving process and not as an immediate event. Therefore, it would be necessary for consumer weakness to kick off the chain reaction, eventually leading us into recession.

If these forecasts were true, we should have seen weakness in demand for travel, new cars, furniture, dining out, clothes, and furniture by now. While we have seen episodic hints of weakness in each of these areas over the last 18 months, demand has stayed healthy enough to keep the economy growing. The media, with its persistent recession rhetoric, has likely scared some people who have seen the remnants of their Covid stimulus checks dry up, but the lower income cohort is always the most vulnerable to economic speed bumps. Likewise, the forthcoming resumption of student loan payments could provide some headwinds to the consumer, but we prefer to wait for the data rather than speculate. Regardless, broadly speaking, the employment picture has remained very solid throughout the Fed’s tightening cycle. Despite recent softness in the July JOLTS numbers, which showed the number of job openings fall to their lowest level in two years, the labor market is holding up well and unemployment claims have remained subdued.

As a result, the consumer balance sheet is in solid shape. According to Mizuho Group economists Alex Pelle and Steven Ricchiuto, Consumer Net Wealth is currently at 860% of disposable income, which is only slightly off its all-time high. Cash-like holdings at 90% of disposable income are similarly close to an all-time high. Conversely, Household Liabilities at 100% of disposable income and Credit Card Debt at just 5-6% of disposable income are near 20- and 30-year lows, respectively. Also, despite the 500 basis point increase in the fed funds rate over the last 18 months, the consumer debt service burden is still lingering around 40-year lows. That might seem surprising given that mortgage interest is generally the largest consumer interest expense, and mortgage rates have shot up to 6.5-7.5%, but those rates only impact consumers who took out mortgages recently. Due to the paucity of turnover in the secondary housing market, mortgage originations have slowed to a trickle. Consequently, the average interest rate on outstanding mortgages has only risen by 8 basis points, according to Jim Reid of Deutsche Bank. That has, so far, combined with a healthy labor market, had only had a de minimis impact on consumers’ abilities, and more importantly willingness to spend. As Pelle and Ricchiuto point out, only four times in the last 75 years has a consumer spending contraction subtracted from GDP, and with a healthy balance sheet as well as many still looking to make up for cancelled trips and postponed vacations experienced during the pandemic, it does not appear to us that the consumer will be a material drag on GDP anytime soon.

While the consumer and the economy have remained more resilient than most have been predicting, we do believe that at some point there will be a broader economic recession. However, the markets do not seem too concerned about this yet. The longer the economy remains aloft, without some sort of demonstrable fracture, the more consensus seems to shift in favor of the soft-landing scenario. Broad investor sentiment has become less dire, which has strengthened the resolve of the equity market bulls this year. Their enthusiasm has helped to propel stocks higher this year, especially the Nasdaq Composite, which is up a whopping 27% year-to-date through September 30.

Currently, the optimistic sentiment in the markets suggests to us that greed is definitely favored over fear. This usually concerns us. Stocks barely blinked as markets absorbed with relative ease 2 of the 3 largest bank failures in U.S. history this past spring as Silicon Valley Bank and First Republic Bank failed within six weeks of each other. According to Bloomberg, the equity risk premium for the tech-heavy Nasdaq 100 is currently at levels seen only in the run up to the Financial Crisis and the Dot.com bubble. We are also beginning to see the IPO window reopen. After raising $275 billion for 911 different issuers in 2021, the IPO market collapsed along with the broader equity markets in 2022, raising a paltry $18 billion for 148 issuers. Year-to-date in 2023, there have only been 69 IPOs raising almost $19 billion, but that is showing signs of a change as the successful launches of Instacart and Arm Holdings portend a wave of deals that could come to market to satisfy “greedy” investors. We may not be at the levels of “irrational exuberance” that Greenspan saw in the equity markets in the late ‘90s, however, with the current rate environment making debt financing costs for all businesses more expensive, earnings and P/E multiples for equities should logically be negatively impacted by today’s higher borrowing costs. While equity markets do have a history of defying gravity and logic for a time, we don’t think it’s prudent to fight the Fed by heavily leaning into today’s “risk on” mentality.

As we like to say, the non-investment grade credit market is a market of bonds rather than a homogenous bond market. Therefore, we analyze each security and make each decision on a case-by-case basis to find the most attractive absolute return opportunities. At the same time, we constantly monitor market technicals to measure investor sentiment and risk tolerance. Today, credit spreads in both the investment grade and high yield bond markets are near their tightest levels since April of 2022. Banks have been able to unload hung deals that have been on their books for as long as two years. Debt deals for highly levered companies are clearing the markets with relative ease. Even some dividend deals, where equity sponsors borrow money to pay themselves dividends on their equity investments, are getting done. So, as we have observed in the equity markets, a “risk-on” bias toward credit seems to be in play today as well. However, according to research from Barclays, despite the increase in gross issuance in the high yield market, year-to-date net issuance is still negative $36 billion. Added to the shrinking risk premium we observe in the equity markets, this corroborates our view that both the equity and credit markets are leaning into risk presently, and we need to remain very selective about where we are making new investments.

Presently, the “Gift Horse” opportunity in the market is in the 1 to 24-month tenors. We have been able to invest our cash at 5.75-6.75% in short-term, higher-quality bonds, which is a very comfortable return to earn while we wait for prices of securities on our watch list to come back to attractive levels. These short-term bonds should also provide an excellent ballast against any potential decline in equities or credit while earning us higher yields than we have seen on this kind of high-quality paper in many years. The opportunity cost of hiding out at the short end of the curve is very small presently. Adding risk to try to pick up an extra 150-200 basis points by either going down the credit spectrum or extending duration and making a bet that the long end of the yield curve will rally does not make sense right now, especially when we can protect capital and earn a decent return while staying defensive. We have a long list of securities that we would like to buy and own longer term, but we are patiently waiting for better entry points.

As always, we remain ever vigilant over our portfolio and continue to apply a commonsense approach to managing risk through our rigorous investment selection process. We continue to maintain a healthy balance of cash and cash-like instruments that will enable us to act quickly to redeploy capital into long-term investments as more attractive opportunities present themselves.

We thank you for your continued support and confidence in our team.

Carl Kaufman

Bradley Kane

Craig Manchuck

Disclosure

The Osterweis Funds are available by prospectus only. The Funds’ investment objectives, risks, charges and expenses must be considered carefully before investing. The summary and statutory prospectuses contain this and other important information about the Funds. You may obtain a summary or statutory prospectus by calling toll free at (866) 236-0050, or by visiting www.osterweis.com/statpro. Please read the prospectus carefully before investing to ensure the Fund is appropriate for your goals and risk tolerance.

Mutual fund investing involves risk. Principal loss is possible.

Past performance does not guarantee future results. This commentary contains the current opinions of the authors as of the date above which are subject to change at any time. This commentary has been distributed for informational purposes only and is not a recommendation or offer of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but is not guaranteed.

No part of this article may be reproduced in any form, or referred to in any other publication, without the express written permission of Osterweis Capital Management.

As of 9/30/2023 the Osterweis Strategic Income Fund did not own Instacart or Arm Holdings.

Current and future holdings are subject to risk.

A basis point is a unit that is equal to 1/100th of 1%.

The Nasdaq is an index that consists of the equities listed on the Nasdaq stock exchange. One cannot invest directly in an index. The Nasdaq 100 Index is a basket of the 100 largest, most actively traded U.S companies listed on the Nasdaq stock exchange. The index includes companies from various industries except for the financial industry.

Yield is the income return on an investment, such as the interest or dividends received from holding a particular security. A yield curve is a graph that plots bond yields vs. maturities, at a set point in time, assuming the bonds have equal credit quality. In the U.S., the yield curve generally refers to that of Treasuries.

Spread is the difference in yield between a risk-free asset such as a Treasury bond and another security with the same maturity but of lesser quality.

Price-to-Earnings (P/E) Ratio is the ratio of a company’s stock price to its twelve months’ earnings per share.

The fed funds rate is the rate at which depository institutions (banks) lend their reserve balances to other banks on an overnight basis.

Osterweis Capital Management is the adviser to the Osterweis Funds, which are distributed by Quasar Distributors, LLC. [OCMI-432945-2023-10-04]

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Osterweis Capital Management