Fourth Quarter Equity Outlook: Mixed Messages

Mixed Messages

As the economy exited the second quarter of 2023, it appeared that the Fed’s elusive soft landing might actually happen. Persistent rate hikes seemed to be taming inflation without slowing the economy or dramatically raising unemployment, and key trends remained positive during the third quarter. Perhaps most importantly, the August Consumer Price Index (CPI) release reported 3.7% year-over-year inflation. While still elevated relative to the Fed’s 2% target, that rate was far lower than the eye-popping 8.3% in August 2022. Furthermore, year-over-year real Gross Domestic Product (GDP) growth in the second quarter came in at a healthy but not blistering 2.1%, and unemployment rose only modestly to 3.8% in August 2023. Perhaps the Fed’s infamously blunt policy instrument of raising interest rates could work — cooling inflation without derailing the economy.

However, the third quarter also produced a litany of worrying developments from an inflation standpoint:

- Oil prices soared due to tightening supply, with West Texas Intermediate (WTI) climbing from just $70 at the end of June to as high as $91 in the middle of September;

- A long simmering trade battle between the U.S. and Europe on one side and China on the other escalated further;

- The United Auto Workers (UAW) called the biggest strike in decades, with the UAW walking out on several of the Detroit Three automakers’ plants and threatening to widen the strike.

The net effect of significantly higher oil prices, a worsening trade war with China, and a large and potentially widening labor strike could very well mean renewed and persistent inflation. The soft landing that seemed tantalizingly close at the end of the second quarter may now be in jeopardy.

Hawkish Pause

Given the strong economy and risk of persistent inflation, the Fed announced a “hawkish pause” at the end of September. The Fed kept the fed funds rate at an elevated 5.25-5.50%, as was widely expected. However, the Fed’s updated “dot plot” that forecasts future interest rates indicated most Fed participants support hiking the rate once more in 2023 to 5.50-5.75%, and the Fed now anticipates holding interest rates higher for longer due to the risk of elevated and persistent inflation.

As a result, Treasury yields spiked, with the all-important 10-year Treasury trading at 4.6%, the highest yield (and lowest price) since 2007. As one would expect, equities also sold off as the market digested the possibility of persistently high interest rates that raise the cost of capital and increase required returns across the economy.

Soft Landing or Stormy Seas Ahead?

As always, predicting the near-term path of the economy, inflation, and interest rates is fraught with minefields. As we wrote about in our second quarter outlook, virtually every professional economist thought the U.S. was headed into a recession earlier this year, and the question was simply one of timing — whether the economy would go into recession in mid-2023, late 2023, or early 2024. As noted above, however, the economy actually appears quite healthy at the moment.

Therefore, we make economic (and even company-level) projections with great humility, acknowledging that the range of potential outcomes is wide. From our vantage point, a soft landing is still possible, especially if the Fed’s more hawkish projection is merely jawboning, with the intended effect of dampening demand to help tamp down inflation without having to actually raise interest rates. Recent wage gains in excess of inflation and low unemployment mean that the average consumer is actually in decent shape, further greasing the wheels for a potential soft landing. Furthermore, savers’ ability to actually generate a real return on cash for the first time in years — due to higher interest rates — creates added income for well-capitalized companies and consumers. Lastly, companies and consumers who locked in debt at historically low rates the past few years may well be shielded from higher rates for now.

However, we think it is equally possible that elevated interest rates materially reduce demand across the economy and send us into a recession. This possibility becomes more acute the longer high interest rates persist. Thus, time is not necessarily the economy’s friend during a period of high interest rates.

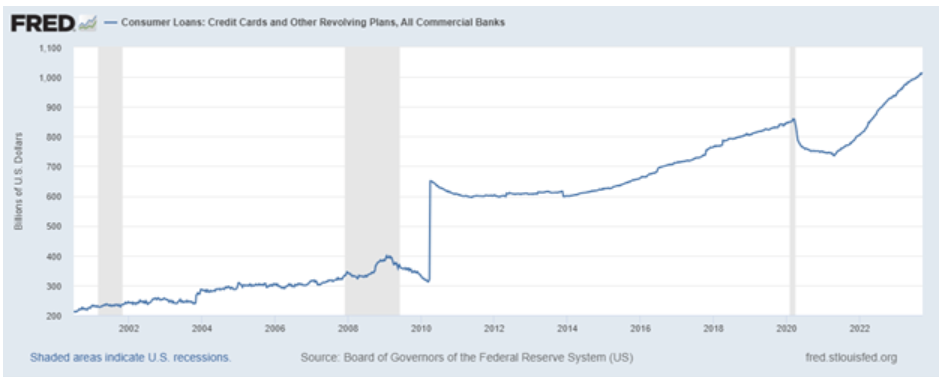

Consider credit card debt, which recently rose to all-time highs of over $1 trillion after plunging over the past two years. Credit card interest adjusts with the market, so consumers with outstanding credit card balances feel a direct impact as rates rise and fall.

Even if the Fed simply maintains rates at current levels, credit card expenses today are much higher than last year because of higher balances. Add in elevated rates and the problem becomes more acute. Consumers will see similar impact for new and floating-rate auto loans, student loans, and mortgages.

Similarly, companies that carry large debt loads well in excess of cash balances have begun to face significant drags on profitability, and we have seen many signs of distress among over-levered private and public companies.

The longer rates remain high, the greater the problem for companies and consumers, especially as refinancing becomes necessary. Exogenous factors like higher fuel and a resumption of federal student loan repayment in October after a three-year hiatus could create added headwinds.

Where to From Here?

The optimist in us looks to the long term and takes comfort in the famous resilience of the American consumer, who drives roughly 70% of economic activity. However, our pessimistic side keeps us paranoid and thinking about the potential risks ahead. We believe owning a portfolio largely comprising high quality, growing companies should serve our clients well given the unclear macro environment. Companies with durable competitive advantages, long runways for growth, strong balance sheets, and good management teams tend to grow earnings, cash flows, and dividends in both strong and weak economies. Purchasing such companies at attractive valuations should prove beneficial to investors.

Conversely, we are especially wary of companies carrying excessive debt given the current macro backdrop, and we are emphasizing companies that should be able to pay growing cash dividends in any environment, underpinned by strong and expanding free cash flow.

We are also now more open to carrying cash in the portfolio as it provides a buffer against volatility while generating a reasonable return due to elevated short-term interest rates. Cash also serves as a reserve, enabling us to take advantage of attractive buying opportunities during market corrections.

We thank you for your continued confidence and are always available should you have questions.

John Osterweis

Gregory Hermanski

Nael Fakhry

Disclosures

The Osterweis Funds are available by prospectus only. The Funds’ investment objectives, risks, charges and expenses must be considered carefully before investing. The summary and statutory prospectuses contain this and other important information about the Funds. You may obtain a summary or statutory prospectus by calling toll free at (866) 236-0050, or by visiting www.osterweis.com/statpro. Please read the prospectus carefully before investing to ensure the Fund is appropriate for your goals and risk tolerance.

Mutual fund investing involves risk. Principal loss is possible. Investments in debt securities typically decrease in value when interest rates rise. This risk is usually greater for longer-term debt securities. From time to time, the Fund may have concentrated positions in one or more sectors subjecting the Fund to sector emphasis risk.

No part of this article may be reproduced in any form, or referred to in any other publication, without the express written permission of Osterweis Capital Management.

Consumer Price Index (CPI) reflects the weighted average of prices of a basket of consumer goods and services, such as transportation, food, and medical care.

Gross Domestic Product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period.

The fed funds rate is the rate at which depository institutions (banks) lend their reserve balances to other banks on an overnight basis.

West Texas Intermediate (WTI) is a light, sweet crude oil that serves as one of the main global oil benchmarks.

Treasuries are securities sold by the federal government to consumers and investors to fund its operations. They are all backed by “the full faith and credit of the United States government” and thus are considered free of default risk.

A yield curve is a graph that plots bond yields vs. maturities, at a set point in time, assuming the bonds have equal credit quality. In the U.S., the yield curve generally refers to that of Treasuries.

Free cash flow represents the cash that a company is able to generate after laying out the money required to maintain and expand the company’s asset base. Free cash flow is important because it allows a company to pursue opportunities that enhance shareholder value.

Osterweis Capital Management is the adviser to the Osterweis Funds, which are distributed by Quasar Distributors, LLC.

[OCMI-434035-2023-10-06]

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© Osterweis Capital Management