I have always had an affinity for short-term interest rates, and it is from my days as an index arbitrageur.

When most people think of index arbitrage, they think of someone scalping stock index futures against an underlying basket of stocks, either electronically or by hand in the old days. But there is more to it than that.

Typically, an index arbitrageur is short a bunch of stock index futures and long the basket of underlying stocks. If you have this position on, you are exposed to a massive amount of interest rate risk. If interest rates dip, you are happy; if interest rates rise, you are unhappy. Often, the profits or losses (P&L) from interest rate movements will dwarf whatever you are doing in intraday trading. There is dividend risk, too, which is not trivial to hedge.

So, at the age of 27 or 28, I found myself spending a lot of time reading speeches from Fed officials, trying to figure out whether they would cut or hike rates. In those days, from 2001 to 2003, the Fed was cutting rates, and we had a lot of rate P&L. In 2004, things got much harder, but by then, I was on to trading ETFs, and we had effectively shut down the index arb business. Others were better at it than we were.

Short-term interest rates are easier to trade than anything else. Why? Because they trend. The Fed doesn’t typically cut, then hike, then cut, then hike. It gets on a rate-cutting or -hiking cycle that lasts for months or years.

That isn’t to say there isn’t volatility in a short-term interest rates position, but it is a lot easier to hold a position than, say, in the Nasdaq or oil, where you are constantly being shaken out with the mean reversion.

Inflection Point

I currently think we are at an inflection point in short-term interest rates.

The Fed has said as much. With a couple of exceptions, pretty much all Fed officials have said that they are done hiking rates, leaving open the possibility of hiking some more if the data gets even hotter. I don’t think that will happen, though.

The first sign of weakness in the economy, the first bad payroll number, and the market will begin pricing in Fed cuts. The market is already pricing in Fed cuts—about 75 basis points over the next year, which is more or less in line with the dot plot. Pretty much everyone knows the Fed hiked too much, and there is open discussion of the idea that long-term interest rates climbing is tightening financial conditions. The next move will be a cut, not a hike—of this much I am certain.

If you believe this, there is an assortment of trades you can put on that give you direct or indirect exposure to short-term rates decreasing. I recommend putting those trades on. I have those trades on.

The conventional wisdom is that the Fed probably won’t cut, and even if it does, it will do a few token cuts in line with the dot plots. No. If the Fed starts cutting interest rates, it is because there is protracted weakness in the economy, and it will cut much more than people think is possible, with the caveat being that it’s unlikely to go back to zero.

We haven’t even discussed the obvious yield curve trades—if this happens, we’ll get the bull steepener, which is one of the easiest trades in all fixed income.

Rate Hike Cycles

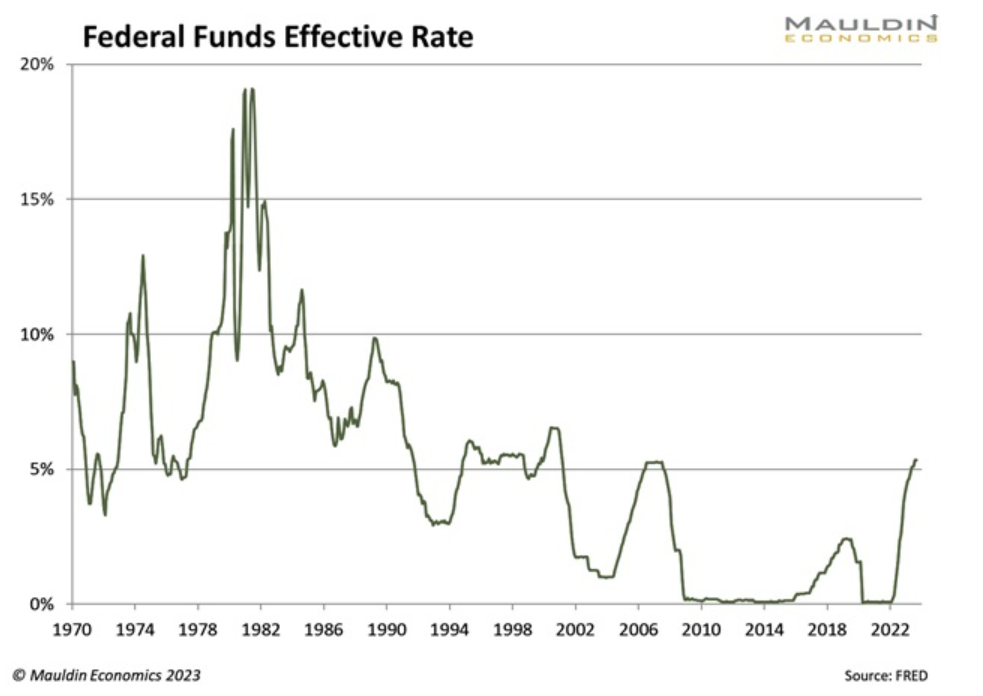

Here’s an interesting factoid for you: The longest the Fed has ever been able to maintain Fed funds at the highest level after a rate hike cycle is seven months. It’s already been two months since the last rate hike. The Fed always overdoes it and has to backtrack—you can see this in a chart of fed funds over the years.

You might have noticed that in the bond meltdown of the last two months, the front end of the yield curve has been more or less anchored. All the pain has been in the back end.

Even if you’re not a trader, even if you’re a casual retail investor, there are ways to take advantage of this—move money into a short-term Treasury or corporate mutual fund. You’re making 5–7% in coupons, and you’ll make another 3–5% in duration, which would be a very good year when it’s likely to be a bad year in everything else.

I am bullish on two things at the moment: short-term interest rates and gold—and practically nothing else. That’s my story, and I’m sticking to it.

Jared Dillian, MFA

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© Mauldin Economics

Read more commentaries by Mauldin Economics