The mid-cap universe offers compelling sector diversification and opportunities to participate in the upside of the broader market, according to Dina Ting, Head of Global Index Portfolio Management.

Whether you’re still on the lookout for inflation head fakes or feeling more optimistic about a soft landing for the US economy, we think it’s a good time to re-evaluate portfolio allocations to the often-forgotten mid-capitalization (mid-cap) market segment.

More established and less risky than smaller-cap stocks, midcaps also tend to offer compelling growth potential for those seeking some balance at attractive valuations. Following this year’s rally in technology stocks, mid-cap stocks are now less expensive compared not only with tech-heavy, large-cap peers, but also small-cap firms.

Representing about 27% of the 1,000 largest US companies by market capitalization, the Russell Midcap Index trades at about 16.5 times projected earnings for 2023, compared to 20 times for the Russell 1000 and 23.6 times for its small-cap peer, the Russell 2000 Index.1

Allocation to the large-cap market, which has returned nearly 21% (for the Russell 1000 Index) year-to-date compared to a relatively modest 11% for the market’s midcap segment, understandably tempts investors.2 Though midcaps did slightly outperform larger caps for the month of November, investors may be hesitant to allocate to the segment, believing that a portfolio of large- and small-cap stocks provides adequate exposure across the market-cap spectrum. But it’s important to look at the longer-term potential of midcaps, which outperformed large caps (9.4% vs 8.3% annualized returns) in the 20-year period before the start of this year.3

Keep in mind that just a select few “magnificent” mega-cap tech stocks drove most larger-cap market gains. Mid-cap indexes, meanwhile, tend to be overweight in industrials—a sector that is arguably ramping up following recent US government stimulus initiatives that include the US$1 trillion Infrastructure and Jobs Act, clean energy spending related to the Inflation Reduction Act, and the CHIPS and Science Act, which is poised to strengthen American manufacturing, supply chains and an array of technologies.

Top industrial sector performers this year include a prominent trucking firm that operates in the more recession-resistant “less-than-truckload” transportation and logistics segment, as well as a leading broad supplier of maintenance, repair and operating products.

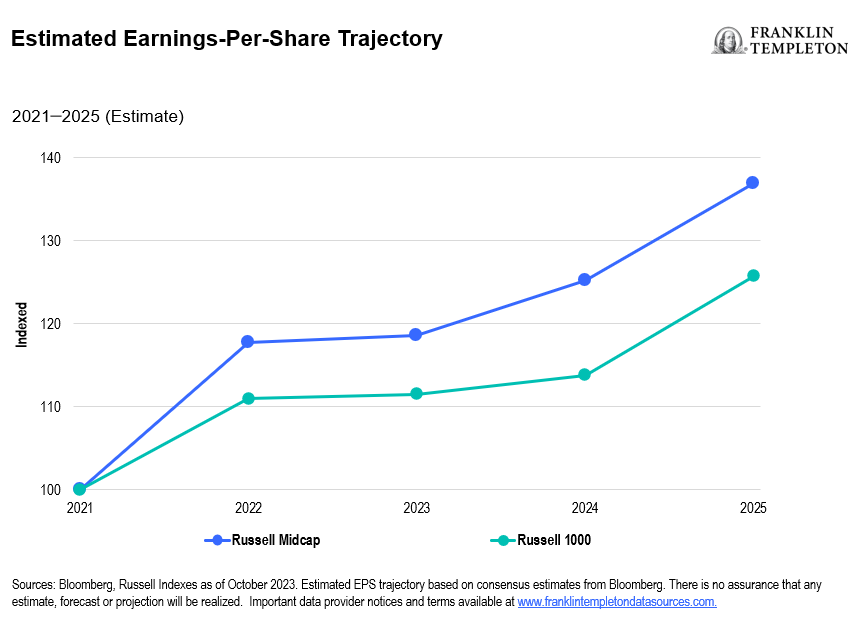

More compelling growth potential vs. large caps

As a highlight to the greater potential of mid-cap companies for expanding market share and entering new markets, consider that Starbucks and Nvidia were solidly in the mid-cap segment 20 years ago, with market capitalizations of just under US$8 billion and US$1.2 billion, respectively. Known to be nimbler relative to larger companies, midcaps can quickly adapt to changing market conditions and capitalize on emerging opportunities. Our research shows that earnings estimates for mid-cap stocks are projected to grow faster than many large-cap companies that may have already reached their life cycle maturity.4

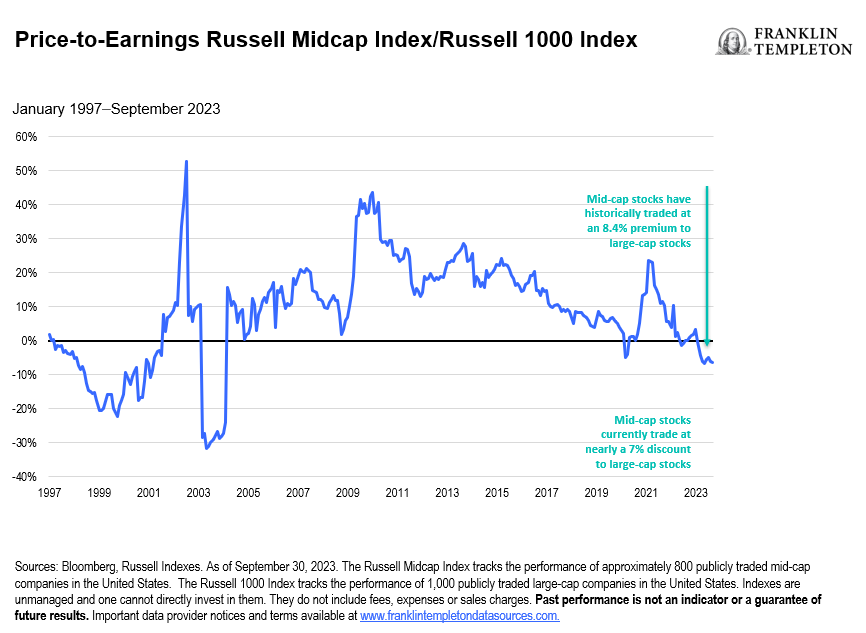

At the end of the third quarter, midcaps also had the benefit of being less expensive. Mid-cap stocks have historically traded at an 8.4% premium to large-cap stocks. But at the end of the third quarter, midcaps were trading a nearly a 7% discount to larger stocks.5

We believe the mid-cap universe offers compelling sector diversification and opportunities to participate in the upside of the broader market. What’s more, rules-based exchange-traded funds that are anchored around diversifying factors such as quality, value, momentum and low volatility can offer smoother performance for weathering market volatility.

The LibertyQ US Mid Cap Equity Index places a significant emphasis on security quality and value factors, while incorporating momentum and low volatility factors to a lesser extent for its top 25% of holdings. Year-to-date, quality has been the main driver of returns for the Index and its return on equity (ROE) was 90% higher than the Russell Midcap Index as of the end of October.6

And lastly, while midcap indices are less IT-heavy than larger-cap peers, multifactor tilts mean that they can still have meaningful weightings to the technology darlings of tomorrow.

1. Bloomberg Nov. 14, 2023. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. There is no assurance that any estimate, forecast or projection will be realized.

2. Bloomberg Dec. 4, 2023. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or a guarantee of future results.

3. Bloomberg Jan. 1, 2002 to Dec. 31, 2022 Russell Midcap Index, Russell 1000 Index. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or a guarantee of future results.

4. There is no assurance that any estimate, forecast or projection will be realized.

5. Sources: Bloomberg, Russell Indices. As of the end of the third quarter, 2023.

6. Source: Morningstar. As of October 31, 2023. The LibertyQ US Mid Cap Equity Index is based on the Russell Midcap Index, its parent index, which measures the performance of the mid-cap segment of the US equity universe. The LibertyQ US Mid Cap Equity Index is designed to reflect the performance of a Franklin Templeton strategy that seeks exposure to four factors: Quality, Value, Momentum and Low Volatility. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or a guarantee of future results.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Franklin Templeton Investments

More Exchange-Traded Products Topics >