Looking Back and Forward

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsLooking Back and Forward

The Way to Think About Cycles

New Year’s, Washington, DC, and NYC

Should auld acquaintance be forgot

and never brought to mind?

Should auld acquaintance be forgot

and auld lang syne?

-Robert Burns

It's that time of year when we start thinking about the old and envisioning the new. This has always been a special season for me, perhaps because of my unusual quirk of really wanting to divine the nature of the future—not just an investment in economics but in general.

This week's letter will be in a different format, as I recently did an interview with my Mauldin Economics partner Ed D’Agostino where we talk about the past years and then some of the way we see the future and then some new plans for Mauldin Economics. And I offer what I think is the best way to mentally visualize the cycles narratives I have been writing about for the past months (about two-thirds of the way down). This is a very edited version of our discussion and I hope you find a few nuggets here and there. Let’s jump in!

Looking Back and Forward

Ed D'Agostino:

John, I appreciate you taking some time. I'm looking forward to this conversation while we've got a little bit of a lull here in the holidays.

John Mauldin:

I'm looking forward to it too because we get to talk about some of the things we've been seeing in the markets, and some of the plans we have for Mauldin Economics.

Ed:

Let's talk about what we've seen in 2023, and what’s next for the economy, the markets, and the world. This has been a year of contrast and it brings to mind the opening lines of Charles Dickens’ A Tale of Two Cities:

It was the best of times, it was the worst of times, it was the age of wisdom, it was the age of foolishness, it was the epoch of belief, it was the epoch of incredulity, it was the season of Light, it was the season of Darkness, it was the spring of hope, it was the winter of despair…

That sums up the sentiment of many people today, where things are so great on one hand and yet we feel so awful on the other. It's a confusing time for many.

John:

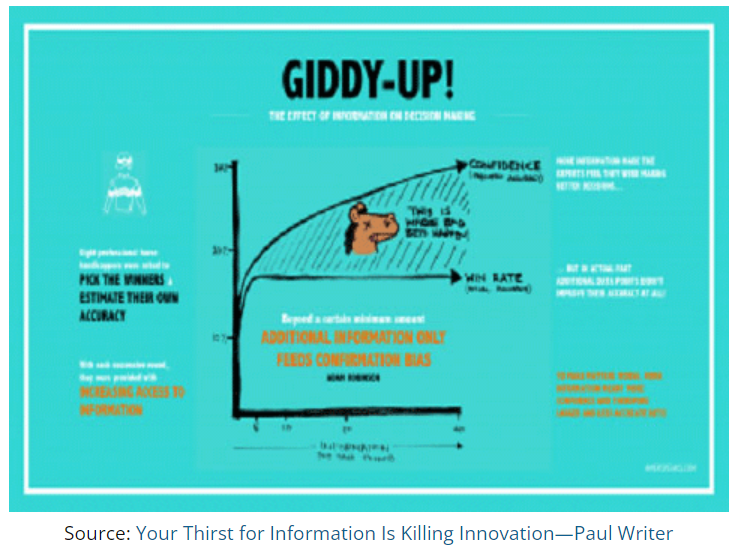

Well, there's several things to be said. A lot of people's optimism flows around their view of politics, and depending on who's in the White House or controls Congress one set of people are happy and other people are not. We've had violent shifts over the last 10 years. That makes it hard for people to trust anything. The media just makes it worse. A constant flow of information doesn't help because ironically—and there's a whole world of behavioral psychology focused on this—we become more confident the more we know.

The classic example is if you take professional horse race handicappers and you ask them to choose a horse, and you give them the five factors (out of 40) that they believe are the most important ones, and you ask them what's their percentage of confidence in the belief, they averaged 17% confidence. The results showed a 70% improvement over mere chance, so they did good. Now, you give them 5 more factors and the win results were the same, but their confidence went up somewhat. This went on and in the final round they had 40 data points, but their win factor did not increase however their confidence almost doubled to 31%. It turns out they're not any more accurate than they were before, but their confidence level went up because “they've got more information.” We live in a world awash in too much information, and sometimes that makes us more confident than we should be.

For me, hearing bias-confirming information makes me uncomfortable. At the beginning of the year, I thought we would see a recession this year. Lots of economists were predicting a recession. I'm uncomfortable when I have that much company.

Ed:

85% of economists thought we’d see a recession by year end.

John:

They did, and I was one of them, I’ll admit. It was a reminder—every time I get in the middle of a consensus, I get this tingle and I think, you're going to be wrong.

I did not predict a fed funds rate of over 5.25%, unemployment at 3.7%, GDP pushing well over 3%, and a good consumer spending Christmas.

I didn't have on my bingo card that commercial real estate, while going down and a problem (as I forecasted), is not taking any big major banks down with it. We had a round of banks going bankrupt earlier this year but that was management incompetence as opposed to something endemic going on in the universe.

And honestly, a lot of people that are very savvy thought we would see a bigger banking problem because of commercial real estate. It hasn't shown up yet. Now maybe it shows up in 2024, but all in all, 2023 was a pretty good year.

Ed:

Going back to what you said about confirmation bias, that's really important. I was speaking with a friend of mine who's a portfolio manager at a multi-billion-dollar hedge fund. I asked him who he reads, what research he follows. It turns out he doesn't follow many economists (he reads you, though). The reason, he said, is, "The bear case is always so compelling and sounds so intellectual, but it's never helped me in my job of managing money because at the end of the day, the market tends to go up a lot more than it goes down."

John:

I remember back in 2010 or so, my friend David Rosenberg announced at our Strategic Investment Conference that he was becoming bullish.

He'd been justifiably bearish for some time prior. When he turned bullish, he lost a third of his subscribers. It turns out they wanted Rosie to confirm their bearish views. And when he was telling them to buy with both fists, which was the right thing to do at the time, they couldn't live with that. They wanted somebody to feed that bearish bias.

Ed:

I see it all the time too, John, when I interview people for Global Macro Update as part of my research process. When I speak with a guest who is optimistic or positive, I get a lot of negative comments.

John:

But the data is clear—it pays to be optimistic. I remember writing a chapter for my book, Bull’s Eye Investing. I wrote that optimists always have problems. Pessimists always have problems. But research shows that the best stance for your portfolio is cautious optimism. Investors should be thinking, “This is where we're going, but we need to have risk controls. How am I going to deal with risk? What am I going to balance it with?” Now, for over 50 years, the way you balanced stock market risk with was with bonds, especially longer-term bonds. And when the stock market was going down, the bonds would go up, offsetting the damage from your stock portfolio. That was the genesis of the 60‒40 portfolio.

But these last few years, since Covid, you couldn’t count on bonds to balance your equity risk. It was the opposite. Not that we've had much equity risk since the bottom, but you certainly have had bond risk. It has backed off a little bit. We've watched the 10-year retreat a hundred points, and the world didn't blow up, nothing happened.

All that being said, I still look around and I see opportunity everywhere. There's always something that's going up.

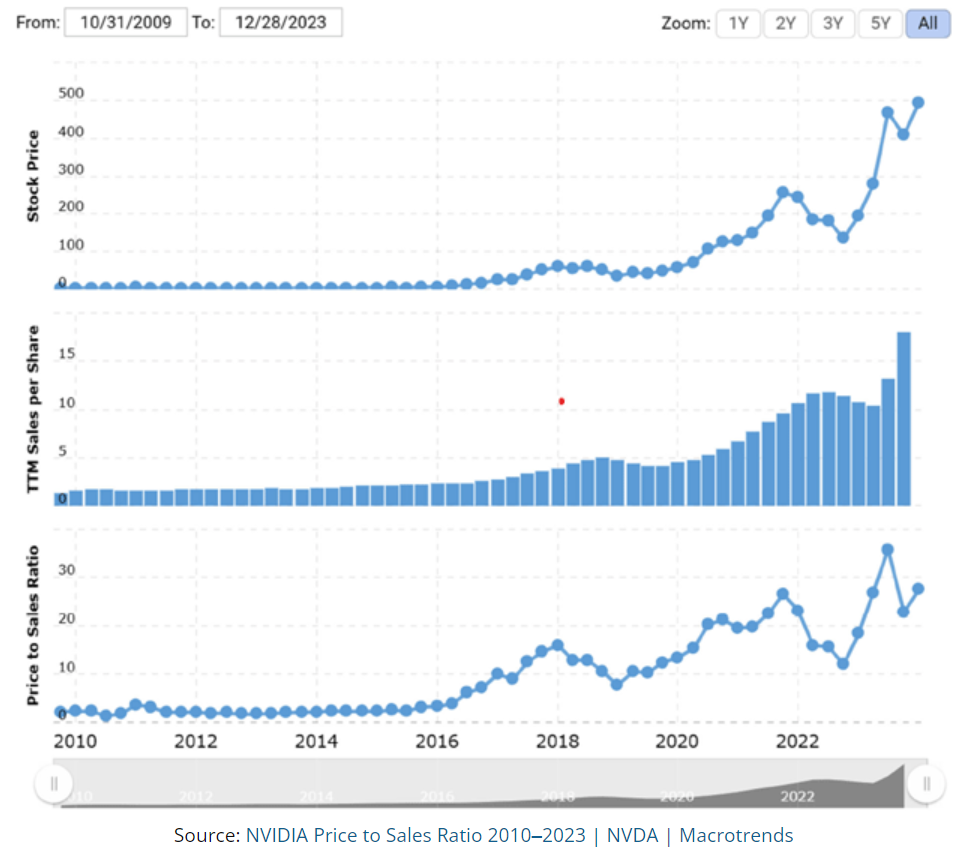

And a lot of times, it's because governments, organizations, just get in the way and they mess things up. Sometimes, it's from exuberance. Things run ahead of themselves. I'm thinking of Nvidia right now.

When something is selling for 27.50 times sales it should mean that investors expect massive revenue growth. Nvidia total revenue is around $45 billion with a profit margin of over 50%. Does anyone really think Nvidia can grow sales to $1 trillion and keep those margins? Forget about competition. Even at the rates they're compounding, it can't grow fast enough to catch up. So, you end up with lots of problems when the market looks around and thinks, "Okay, this is overvalued." It doesn't mean that Nvidia isn't one of the most important companies in the world. It is. But that doesn't mean it's a good stock to buy today. And of course, now that I've written that, the price of Nvidia will likely double over the next few months.

I've been writing lately about cycles, and as I near the end of this series, I'm going to have to ask, "What does your portfolio look like?" I’m thinking about the end of this cycle, at the end of this decade, when we start seeing what I think is going to be a pretty tumultuous period. I’m looking at my own portfolio and I’ve realized, "This isn't the portfolio I want to go into that period with."

The object, I think, for investors, is to take as much buying power as we have today and get it to the other side. And that doesn't necessarily mean an S&P index. There's lots of ways to get your buying power to the other side. Some of it's with macro ideas that you and I talk about. Some of it is simply asking, what's going to be there in 2034?

Ed:

I think you have to determine what is an appropriate framework for yourself. Each investor has to figure out what is the right framework for them to view the world. We are moving from an index-driven world to a more thematic world where you need to have a framework for understanding what are the truly dominant themes or trends that will drive investment success and lead you to the companies that are going to be there in 10 years.

John:

You and I have been talking about this for 10 years. 25 years ago, as I started writing this letter, I was thinking in these macro terms.

And over time, it’s evolved. And you have been on the same journey lately. You have done a remarkable job with your interviews and expanding our network. We have access to so many smart people. And then, between the conference and who we are, we have so much information.

Ed:

That's a big part of what we try to do, is help people filter what is important. We try and show all sides of an issue, in a way that is complete but efficient.

John:

Right. With my letter, I have lots of links to sources. If a reader wants to go deeper, have at it. Mauldin Economics is becoming what I hope is an essential filter where we help you find information in a way that makes sense.

Ed:

Exactly. The number-one question that we get almost every week—you from your readers, me from my viewers—and the top comment coming out of our Strategic Investment Conference every year is, "This was amazing. Thank you. But how do I invest?"

That's the biggest unanswered question we've had since we started Mauldin Economics. How can readers take the macro, the big picture, the cycles, the trends, the Great Reset, reshoring, AI, all these big, big topics we cover—how can they invest around these trends in a way that makes sense?

And that's the evolution of Mauldin Economics that we've been working towards for several years. We are weeks away from being able to provide the answer.

John:

How long have you been doing your podcast now?

Ed:

A little over a year. At first, people who know me were saying, "Well, this is great information, but why are you doing it? You're busy with your day job running the business." The answer is, this is part of my research process. It started as a way for me, personally, to create my own investment framework.

John:

That was my motivation when I started writing the letter—how can I understand this? Writing helps me think through the noise.

Ed:

Some of this we do just because we love the topics and we find it fascinating and it is important. But then it comes back to that question, right? How do I invest in this? And that's where investors need to draw a line between the big trend and cycle data that we talk about versus how to invest.

John, all these topics we've been talking about make me think about the work that you've been doing on cycles. You've studied multiple authors, big thinkers for your cycle work. What's the five-minute summary? Are you optimistic and how does technology factor into all this?

The Way to Think About Cycles

John:

I'm always optimistic long-term, but if the midterm is five to seven years, I'm not very optimistic. I've written about four people's views of long-term generational cycles. I've got my own view about debt and the debt supercycle and our economy that ties into that same pattern. And all of them deal with different ways to view trends from the past. Neil Howe works with generational patterns he outlined in his book The Fourth Turning Is Here.

Peter Turchin's End Times where he talks about the overproduction of “elites,” where he sees the problems in society as problems of too many elites competing for too few leadership positions, which he takes back millennia and shows the same overproduction of elites ends up in wars or large economic shake-ups (really, it was often just too many barons and dukes have kids and they all wanted to be at the top).

Friedman looks at long geopolitical cycles. Dalio looks at big market economic cycles. And all of them, they are looking at the same historical patterns. They just see it through a different lens, but it all points to a culmination of crisis, if you will, a problematic era. The French call it fin de siècle, the end of the cycle or era which they all see is about the end of this decade.

Normally when we think of cycles, we think of a big circle. It just keeps repeating itself. I think that's the wrong way to look at it today. We should view these cycles as spirals. It's not repeating, it's still going up and down, but it's not going up and down like it did in the past, it's in a different time frame. Through time we're spiraling through these cycles. And we've got multiple spirals all working with each other, but in my mind, what I see is a central arrow, a thrust, a cord right down the middle, that's technology.

Technology is pulling all of this forward. It has its own center of gravity, if you will, that shapes and changes how these spiraling cycles play out. A world with instantaneous social media is radically different than 1860s US, World War II, the 1930s. It’s a different framework. The same patterns are there, but with different causes, different gravity if you will, through the center.

It's like technology is becoming its own gravitational force. It changes things as it goes through the cycle. If these guys are right, we're going to end up with a better world, with much better technology. AI is going to change things. So did the internet, so did electricity and railroads, but not as fast as AI is going to change things. We went from 80% of the people working on the farm to 1%, but that was over generations. AI is going to change things a lot faster.

Ed:

I agree. From the investor's perspective, this is where the narrative gets confusing. Every company CEO for the next two years or so, on every earnings call, will be talking about how they're using AI. And most of that will be hype. Very few companies are going to get AI right in 2024. I think most people are already playing around with ChatGPT and tools like that and figuring out how to accelerate daily tasks.

Attorneys will use it to write briefs and analysts will use it to pull research. Writers will use it to edit documents. That is what I mean when I say CEOs are going to talk about how they're using AI. Technically speaking, they are using AI, but that's not a good investment case. That’s what everyone is doing. There’s no advantage.

AI is one of the big investment themes we are following. There are a select few companies that started integrating AI before we were hearing about ChatGPT and Sam Altman. These early adopters were integrating AI deep into their processes. They pulled their procedures apart and identified all the areas where they could inject AI. And AI is in large part just leveraging their own data and then figuring out how to predict customer behavior and needs, create new products and services, and grow without adding more staff.

John:

I complained to you about a local bank that my poor assistant had to get on the phone at 7 o'clock her time and didn't get off till 11:45. She had to pull me in seven or eight times. We went through, and this is not an exaggeration, 20 different reps.

And they would all start out asking the same questions to verify my identity.

That’s a task that an AI could do better than a human, and everyone would be happier, especially the customer. Maybe the reps who lose their jobs wouldn’t agree.

Ed:

I don’t see AI destroying jobs. There will be transitions that will no doubt be negative for some, but on the whole, we need productivity to increase. AI will make that a reality. But again, today there are only a select few companies with the management wherewithal to identify these problems and the tech savvy to implement AI, not just superficially at the ChatGPT level, but deep in their systems and reinvent their processes.

Whenever you have a good customer service experience with a bank or insurance company and you're surprised, there's usually a level of AI behind it that has smoothed things out. That's only going to get better.

But this is where it gets really hard for an investor, because there will be lip service for AI across the entire investment ecosystem. We are searching for the early adopters that really get it. Most of these companies will use facilitators—savvy consultancies essentially—that work with them to integrate AI across the board. There’s a narrow band of companies to invest in at this stage of AI's evolution.

John:

I agree. But let's say this bank figures out their problem, and within this next year they adopt AI. They're going to cut some large number off their expenses and improve customer experience. This is a $10 billion bank. Cutting even $100 million of expenses doesn't move the needle. It certainly makes their customer experience better, but it's not going to make their stock better.

Whereas, whoever the group was that helped them get there is the company that's really going to profit, percentage-wise. The pick-and-shovel guys... Yeah, we're going miss the thrill of finding that motherlode in the Sierra Nevadas, but we're going to want to buy the companies that sell a lot of picks and shovels in the meantime.

Ed:

Yes, I think this is a classic pick-and-shovel play. And I'm not sitting here saying I'm a stock jockey. That's never been my trade. But like you, I like to build the framework necessary to develop these themes, and thankfully, internally we have the stock jockeys. We're close to delivering a service that goes beyond providing a theme or a framework. We’ll soon have the whole package—a framework that includes ideas for your portfolio.

John:

Ed, that's just one of the reasons why I'm pretty enthusiastic about what you're doing. We've been talking macro. We've been trying to figure out how it fits in and how we can help our readers. And what you've been doing, the team you've been pulling together, it's kind of a culmination of, well... next year will be my 25th year of writing this letter, which has had a macro theme. But now we're collaborating together, we're working together to pull this into a framework that becomes more useful.

My letter has been self-limiting because I was a broker-dealer, an investment advisor. I had limits on what I could say to buy or sell. You don't have those limits. Our business structure is completely different now. You're allowed to come in and say, "Let's take this work..."—not just my work, but along with your own research, all of this data that we get together, and let's put it into an actionable framework. I think that's going to be a really exciting culmination of what I’ve been working on for a very long time.

New Year’s, Washington, DC, and NYC

As you are reading this letter, I am out shopping or cooking for the roughly 300 people who have said they're coming to our home on New Year's Day for Shane’s black-eyed peas and my chili and prime, plus a lot more. 15 gallons of chili, about the same amount of black-eyed peas, 40 lbs. of prime and lots of mimosas and wine. It will be awesome!

I will be in Washington, DC, on January the 20th and likely the next day take the train to New York where I will be for three or four days meeting with clients and partners and potentially some media.

I am always optimistic at this time of the year. There's a new year just waiting to surprise me. Some years my optimism is warranted, and some years it's not. But I still start out optimistic. I really expect that the gravity of technological progress will pull us through whatever we face in the future to a much better world. In 2035, nobody's going to want to go back to the good old days of 2023. Let alone 2020.

Thanks for giving me your time and attention. I really appreciate it. As a final parting gift, I maybe listen to 30 different acapella versions of Auld Lang Syne. I discovered a new group (to me) called Home Free. Their version mesmerized me. I hope you enjoy it. The link is here.

It's time to hit the send button. My son Trey and his son Dakota with their significant others will be at the home tomorrow to celebrate New Year’s with us. Plus help with the cooking. Here's my best to you for the New Year.

Your remembering old friends and hoping to meet new ones analyst,

John Mauldin

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All