- Rates rode quite a roller coaster last year as the Fed aggressively hiked rates. How did the municipal market react to the rate volatility?

2023 was quite a ride for the municipal bond market – one that produced a positive annual return despite significant momentum swings from quarter to quarter.i While rates peaked in October, dovish Fed messaging in December sparked another rally as investors priced in an approaching end to the Fed’s tightening cycle. During the December move, Treasury yields fell more than 100 basis points from their peak and municipals rallied even more strongly. The rate relief helped produce positive annual returns for the Bloomberg Municipal Bond Index, which climbed back into the black after the longest stretch of cumulative negative returns (42 months) since its inception in 1980.ii The rate market selloff also provided an opportunity for actively managed portfolios seeking to harvest tax lossesiii and reinvest at higher yields, potentially increasing the tax-exempt income stream for their portfolios. We observed significant tax-loss-harvesting activity, which contributed to secondary trading volumes peaking in the fourth quarter.

- What is your view of municipal market valuations? How might they affect market performance in 2024?

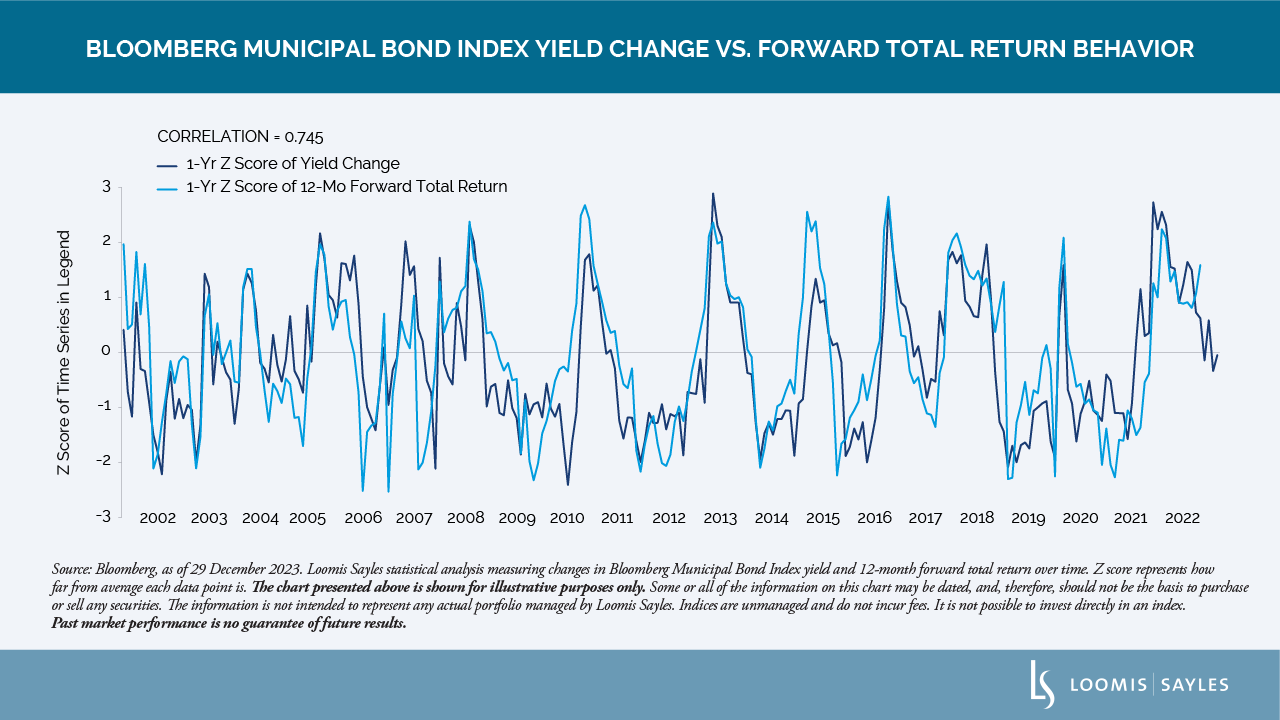

In addition to strong nominal market performance, municipals registered strong relative market performance in 2023, especially versus Treasurys. Municipals were not distinct in that regard. Risk markets of all stripes generally outperformed Treasurys as investor sentiment abruptly shifted in the last months of the year. This outperformance pushed valuation ratios to the richer end of historical ranges (AAA-rated muni yields/Treasury yields).iv While valuations can be a useful shorthand technical metric for evaluating risk/reward conditions in the market, they are only one metric. We believe valuations should be weighed with other factors, particularly credit fundamentals and, as simple as it may sound, nominal yields. Though it may seem counterintuitive, our analysis found generally limited statistical correlation between richening or cheapening valuation levels and nominal forward one-year total returns.v In contrast, and perhaps more intuitively, we found very strong correlation between richening or cheapening nominal yields and forward one-year returns.vi With current yield levels generally higher than those prevailing over most of the past decade, we continue to see opportunity in the municipal market, despite the recent rally.

- How do you expect supply and demand dynamics to play out in 2024?

Though rates declined sharply in recent weeks, municipal yields remain above levels typical of the past decade. We expect that elevated yields will continue to help drive underlying investor demand. The prospect of a Fed policy pivot bolsters our market outlook. In our view, a shift toward looser monetary policy would likely provide a tailwind for the municipal market, offering some potential relief after two years of aggressive rate hikes. We anticipate a modest increase in new issue volume this year as a more benign rate environment likely draws issuers off the sidelines. And with more than $6 trillion currently in money-market funds,vii we believe a pivot to looser Fed policy would encourage investors to reallocate to longer-term asset classes like municipal bonds.

MALR032375

Market conditions are extremely fluid and change frequently.

This blog post is provided for informational purposes only and should not be construed as investment advice. Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors only and do not necessarily reflect the views of Loomis, Sayles & Company, L.P. Information, including that obtained from outside sources, is believed to be correct, but Loomis Sayles cannot guarantee its accuracy. This material cannot be copied, reproduced or redistributed without authorization. This information is subject to change at any time without notice.

i Source: Bloomberg, 12-month return for Bloomberg Municipal Bond Index as of 31 December 2023.

ii Source: Bloomberg, as of 31 December 2023.

iii As explained by Investopedia, tax-loss harvesting is a strategy investors can use to reduce capital gains taxes owed from selling profitable investments. A tax-loss harvesting strategy involves selling an asset or security at a net loss. You can use proceeds from a sale to purchase a similar asset and maintain the portfolio balance.

iv Source: Bloomberg, as of 31 December 2023.

v Loomis Sayles statistical analysis of Bloomberg Municipal Bond Index 12-month total returns versus price ratios (10-year AAA /10-year US Treasury) from January 2001 through December 2023.

vi Loomis Sayles statistical analysis of Bloomberg Municipal Bond Index 12-month total returns versus average 12-month change in index yield-to-worst from January 2001 through December 2023.

vii https://www.financialresearch.gov/money-market-funds/

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© Loomis, Sayles & Co.

Read more commentaries by Loomis, Sayles & Co.