For much of the past 15 years, the 60/40 portfolio of 60% U.S. stocks and 40% U.S. fixed income has been the foundation of portfolio construction, providing investors with exposure to the growing U.S. economy and to fixed income securities for protection during downturns.

Over the past two years, this portfolio strategy has broken down. Stock returns have been volatile and barely positive. When volatility sent investors looking for shelter, fixed income provided little refuge. In fact, the Bloomberg U.S. Aggregate Bond Index produced consecutive years of negative returns -- the first time in its history.

The culprit is inflation and the Federal Reserve’s interest rate hikes to combat rising prices. Inflation has been absent in the economic conversation for nearly 20 years, and investors have forgotten many of the lessons of the past. To understand what might lie ahead, investors need to assess both recent inflationary forces and historic trends.

“90% Risk”

The 60/40 portfolio currently faces several challenges, but market risk is perhaps the most significant. A 60/40 strategy may have 60% of the portfolio in equities, but that 60% represents closer to 80-85% of risk. In 2023, it was even worse. For the S&P 500, up 26.3% in 2023, the largest 7 stocks were 28% of the weight and fully 60% of the performance.

The Magnificent Seven -- Microsoft, Apple, Amazon, Nvidia, Facebook, Google, Tesla -- share similar characteristics. They are all very large technology or technology related firms in the U.S., and all have considerable interest in advanced technology and artificial intelligence. In the scope of portfolio construction, there is little difference or diversification between them.

The effect these stocks have on market capitalization weighted indices amplifies the risk of investing in equity and pushes the proportion of risk from equity in the 60/40 up to and even beyond the 90% level.

An easy solution would be to simply lower the weight of equity in an investor’s portfolio, creating a 40/60 portfolio, or even a 20/80 portfolio. With bond yields at 4% or more, such a strategy could make a lot of sense and generate reasonable returns. But in the past two years fixed income and equity investments have moved in the same, not opposite direction, increasing the 60/40 portfolio risk.

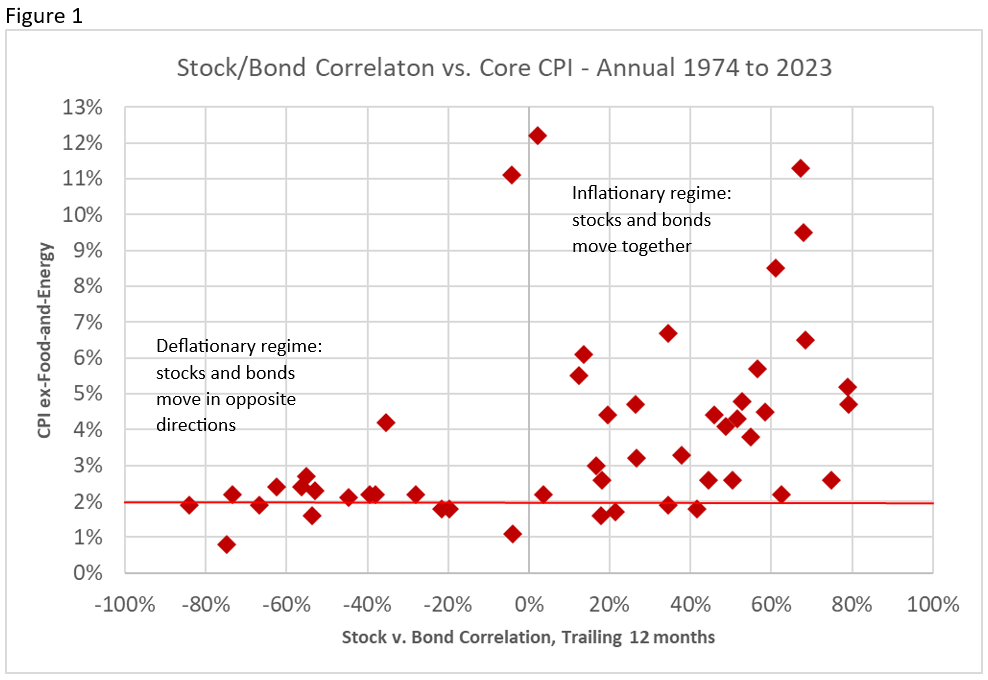

Again, inflation is the culprit. Historically, when inflation is higher, the diversifying benefit of bonds goes away. High inflation leads to higher interest rates, and fixed income investments become more attractive. Investors divest from equities, waiting until rates fall before reinvesting. In such environments, the Federal Reserve is no help, as it’s focused on controlling price growth, and is reluctant to lower rates when the economy looks soft. This is what is known as an inflationary regime.

When inflation is low and stable, as it had been for two decades prior to 2022, we have had a disinflationary regime. The Fed focused on stimulating economic growth which indirectly supported stocks, giving birth to the ‘Fed Put’. The 60/40 strategy works well in such a regime as stock and bond returns tend to move in opposite directions.

Where is the dividing line between these two regimes? An inflation rate around 3%. Figure 1 shows the correlation between stock and bond returns with different inflation rates. When inflation rises above 3%, stock and bond correlations have been positive, while below 3%, stock and bond correlations have been negative.

With much uncertainty about 2024 market it is unclear whether the 60/40 can provide a diversified portfolio. However, investors can include several different investments to provide all-weather portfolio robustness.

Commodities: Commodity investing provides diversification to equity portfolios in inflationary regimes. Active management strategies such as managed futures combine active management with the diversification effects of commodities to provide value for investors.

Small Cap Equities: There are ways to include equity in a portfolio while minimizing the risk levels that large U.S. stocks provide. Small cap investing has always been a segment where active investors can benefit, thanks to the lack of attention this area receives. Recently, small cap underperformance, combined with a turn in the interest rate cycle makes small caps more attractive.

Emerging Markets: After 15 years of underperformance, Emerging Markets are considerably undervalued relative to developed markets. But the diversity and health of emerging market economies and a peaking U.S dollar may provide catalysts for EM in the coming years.

Volatility: Volatility is an asset class that has developed over the past 30 years with the increase in volume in option markets. Investors can tap into this liquidity not to speculate, but to generate income through covered call writing, commonly called equity-income investing. Products delivering this strategy have exploded in popularity in the past 3 years.

Fixed Income: Fixed income still belongs in any portfolio construction, particularly with current higher yields. While a more uncertain inflation environment provides challenges to returns, active management in fixed income has had considerable success adding value. Putting a portion of our fixed income allocation into an active product can turn bonds into a source or performance instead of simply a safe and diversifying return.

Conclusion

The critical question for asset allocators in 2024 is the state of the inflation cycle. Inflation was triggered by a combination of massive fiscal and monetary stimulus and supply-chain disruption, both related to the pandemic. With these inflationary forces established, it is hard to believe that inflation will return to the 2% level that the Federal Reserve targets. Three percent is more realistic. The 60/40 portfolio has been a great strategy for many investors, but the economic regime is changing. Successful investing for the next decade will depend on a broader range of investments based on lessons from the past.

Derek Izuel is Chief Investment Officer at Shelton Capital Management.

Important Information

Investors should consider a fund’s investment objectives, risks, charges, and expenses carefully before investing. The prospectus contains this and other information about the fund. To obtain a prospectus, visit www.sheltoncap.com or call (800) 955-9988. A prospectus should be read carefully before investing.

INVESTMENTS ARE NOT FDIC INSURED OR BANK GUARANTEED AND MAY LOSE VALUE.

A message from Advisor Perspectives and VettaFi: Advisors: You're Invited to Exchange! Nothing would be a better start to the new year than if you joined us at Exchange, an in-person conference for members of the financial services community in Miami, Florida on February 11-14th. For a limited time, we're offering you a free Exchange ticket!* Register today with code WINTER24 to claim your pass.

© Shelton Capital Management

Read more commentaries by Shelton Capital Management