No Way Out

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsUnbalanced, Imprudent, and Poorly Timed

Crying Wolf

Bipartisan Debt

Naples, Washington, DC, NYC, and Cape Town

Having now spent almost six months describing the historical cycles and massive debt that surround us, I find myself looking for an “easy” exit. Maybe one exists, but I haven’t found it yet. I think we’re stuck. The building will have to collapse around us before we can leave.

This is obviously not a great situation. For one thing, if we don't plan properly, the building could easily collapse on us instead of around us. Our entrapment may also cause us to neglect other big problems and maybe miss important opportunities.

The sad fact is we have no easy way out of the debt situation. Worse, we are actually choosing this fate. It’s not about individual choices; none of us want the crisis that’s coming. But all the solutions require joint actions we are apparently unable to take. Which means we are, by default, choosing a path which for many will be catastrophe.

We face this not just because of government policy choices but the political process itself. It is a function of the two-party system. Our system has lost the ability to act decisively against big problems we all see coming. We are a nation of deer in the headlights.

But our system won’t stay paralyzed forever. At some point, we’ll see action because the crisis will have become impossible to ignore. Then we’ll respond. It will be a furious, poorly planned response with massive side effects that could have been avoided unless some of us begin thinking about possible solutions in advance.

Melodramatic? Hyperbole? Let's rewind the clock to 2008 when then-Treasury Secretary Hank Paulson literally got on his knees to House Speaker Nancy Pelosi, begging her to authorize the bailout for the banks. The system was getting ready to collapse. The plan was poorly thought out, but that is my point. No one really “war-gamed” the possible solutions and choices in advance. Rather, with leaders on both sides of the aisle staring into the abyss and realizing there was no bottom, they made the best choices they could in a very short time.

Now we have an approaching debt crisis we can actually think about in advance. I believe—and hope it’s not just my naive optimism—we will have some time to consider solutions. And as I have been saying for years, nobody will be happy. We have gone way past the time for relatively easy fixes. Having cut taxes and increased spending, we are running almost $2 trillion deficits annually.

As we will see below, when I suggested part of a future compromise, I got serious pushback from readers on both sides. And the irony is I understand the frustration. Viscerally. I agree that everything that I have suggested in the past few weeks and months are bad choices. But in the future, the worst choice will be doing nothing and letting the economy collapse around our ears. Some might come through it, but the vast, vast majority of us won’t.

That’s not the future I want to predict, but I see no other possibilities. I think we have a few years left but there are already mutterings of stress in the US bond markets.

Then again, perhaps the denouement will take longer than I think (Japan?), but it will arrive. Today we’ll talk about why.

Unbalanced, Imprudent, and Poorly Timed

Mathematically, balancing the budget is no great mystery. We know what to do: cut spending and/or raise revenue until the two sides match. But that’s where it all breaks down. No one wants their favorite spending programs reduced or their taxes raised.

This was evident in my letter last month describing a possible value-added tax (VAT) system. It drew far more responses than I usually get, and they were mostly negative. The very idea of any new tax, even one paired with spending reforms and cuts to other taxes, outraged many readers. These are direct quotes from reader emails:

-

“Taxes by our corrupt leaders are NEVER dialed back!! You are dreaming!”

-

“We all know that once a tax increase is allowed, the spending reductions would be ignored.”

-

“You need to cut spending, not reward incompetence and corruption with more gravy.”

- “Absolutely no VAT. Politicians need to control spending. Live within your means. There is so much waste and fraud.”

-

“Worst idea ever. Start by cutting the size of the government.”

-

“If you think the US policy makers would stay put with a 5% VAT—I have a bridge to sell you. They’ll just keep increasing it and won’t cut a tinker’s damn from spending.”

-

“You have clearly lost your mind. You have bought into WOKE. If you give a politician an opportunity to soak you, he or she will. The party makes very little difference these days.”

-

“Another tax? The political class will surely love another source to keep blowing money in newfound ways.”

This isn’t a random sample of the population, of course, but I think the sentiment is common. Many people simply don’t trust elected officials to do what elected officials are supposed to do. They have good reason to feel that way, too.

Contrary to what a few readers think, I'm not on some ideological campaign to raise taxes. I would actually like to reduce income taxes and replace them with a VAT because consumption taxes are less economically distorting. And also cut a lot of spending. We could even have a higher VAT and eliminate Social Security taxes. There are lots of options and my preferences are just a few of scores of options. That is what compromise will look like.

Many said, in various ways, they would agree to new or higher taxes only after every possible spending cut had been tried. But no one specified what spending they would cut. At most, they alluded to vague “waste and fraud.” What is that? We have been trying to cut out waste and fraud for my entire adult life, and I’m sure we have done so in a few areas, but then we add other spending on top of it.

Worse, our decades of delay mean balancing the budget with spending cuts alone would require draconian cuts that would wreak havoc on the economy.

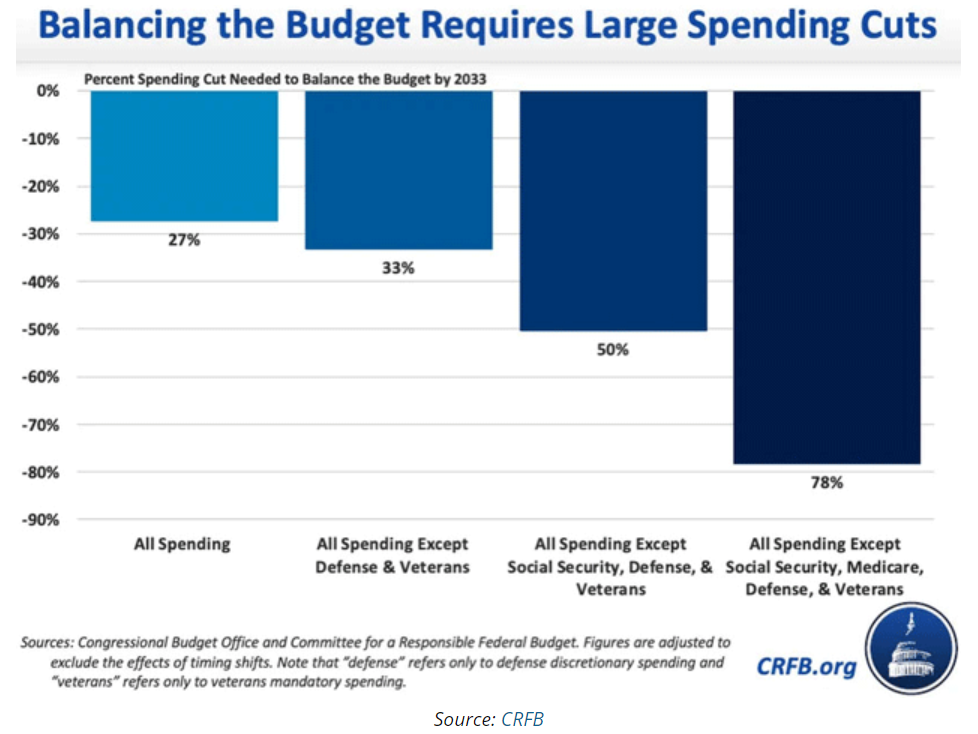

The experts at the Committee for a Responsible Federal Budget put a pencil to this last year. They found balancing the budget by 2033 with spending cuts alone would require immediately slashing 27% of all federal outlays. That would include defense, Social Security, Medicare, veterans benefits, law enforcement, border protection—everything.

That number rises quickly if you start exempting certain categories. Wall off Social Security, Medicare, defense, and veterans programs (plus interest on the debt!) and balancing the budget by 2033 would require 78% cuts to everything else the government does.

I am not here to argue everything the government does is helpful or productive. A great deal of it isn’t. Waste and fraud happen, too. But if you think such giant cuts wouldn’t cause enormous turmoil and side effects, I think you are sadly mistaken. Our entire economy is optimized to the assumption the government will always do certain things.

For example, if you think air travel is miserable now, wait until they fire 8 out of 10 TSA agents and air traffic controllers. Do you really think the air traffic would be safe in today’s environment without TSA? Trust me, after millions of miles in the air, I get the frustration with TSA more than most. Yes, we could raise airline ticket fees to pay for the TSA. Maybe we should. But that’s just one small example. There are literally scores of other things we depend on the government to do effectively. Can the private sector do a lot of them? Sure. And that will almost assuredly be part of the solution. But it’s not something we can set up quickly.

What we need is a rational process of balanced, prudent, well-planned privatization, spending cuts, and tax reforms. That is nowhere on the radar right now. When the crisis comes, without some of us thinking about possible solutions, we’ll get the opposite: unbalanced, imprudent, and poorly planned.

And as bad as those changes will be, at that point they’ll be better than the alternatives. Just like 2008.

Crying Wolf

I have been saying this for a distressingly long time, long enough to be labelled “the boy who cried wolf.” And others were saying it years before I did. The coming debt crisis may be the most widely predicted one in history.

But here’s the rub: Wolves actually exist and, given the opportunity, can hurt you badly. There is no doubt the debt exists, and that our ability to sustain it is steadily declining. Anyone paying attention to political news, no matter what side you’re on, can see we’re doing nothing to change course. I don’t feel like I’m crying wolf. But I’ll admit to being early. Timing is hard.

For example, here’s a quote from my May 7, 2011, letter titled Muddle Through, or Crisis?:

“I think we have two choices as a country. We can elect to deal with the deficit proactively or wait until there is a crisis and react. And make no mistake, there is an approaching Endgame, with regard to how much debt the market will let us have. We don’t know that point now, but if it happens it will be quite a ‘surprise!’

“… Let’s assume we do not deal with the deficit in any meaningful way. Eventually the debt will rise to epic, Greek proportions. The bond vigilantes arise from the dead and start to push up interest rates. Interest as a percentage of government spending rises, crowding out other government expenses or increasing the debt still further.

“Then we have a crisis. We are FORCED by the bond market to get the deficits under control, but now we are doing so in a crisis. Health care will have to be slashed by far more than it would in a more controlled scenario. Tax increases will be brutal. You think Social Security is untouchable? Not in this crisis world. Means testing and spending freezes will be the rule of the day. Military cuts will seem draconian. Our allies who depend on us for a defense shield will not be happy. Federal education spending? Not all of it, but some of it will be on the chopping block…

“What’s my basis for this? History. This movie has played over and over again in various countries in modern history. While we may be the world’s superpower, we are not immune from the laws of economic reality.

“In such a scenario, I expect QE 4-5-6. Could the Fed literally monetize the debt and then “poof” it? When our backs are against the wall, don’t assume that what has been seen as normal will be the reigning paradigm.”

I wrote that almost 13 years ago and I stand by every word today. Crisis is coming. If we had taken some relatively modest steps to avoid it when I wrote those words, we would be in a better position now. We didn’t… so here we are.

Bipartisan Debt

The most frustrating part is this could all have developed quite differently. As recently as 2001 the federal government had a budget surplus. Revenue was actually about $133 billion more than spending that year. There were smaller surpluses in 1999 and 2000. They resulted from a unique set of circumstances: the strong 1990s economy, low interest rates, and bipartisan tax and spending reforms. Bill Clinton and Newt Gingrich, realizing neither would get anywhere without the other, worked together and (trigger warning!) compromised to get some of what each wanted.

Alas, this brief period of sanity ended after 2001. Had it continued we might have slowly paid down the debt. Fantasy? No, not at all. CRFB issued a report last week showing what might have been. It’s long but well worth reading.

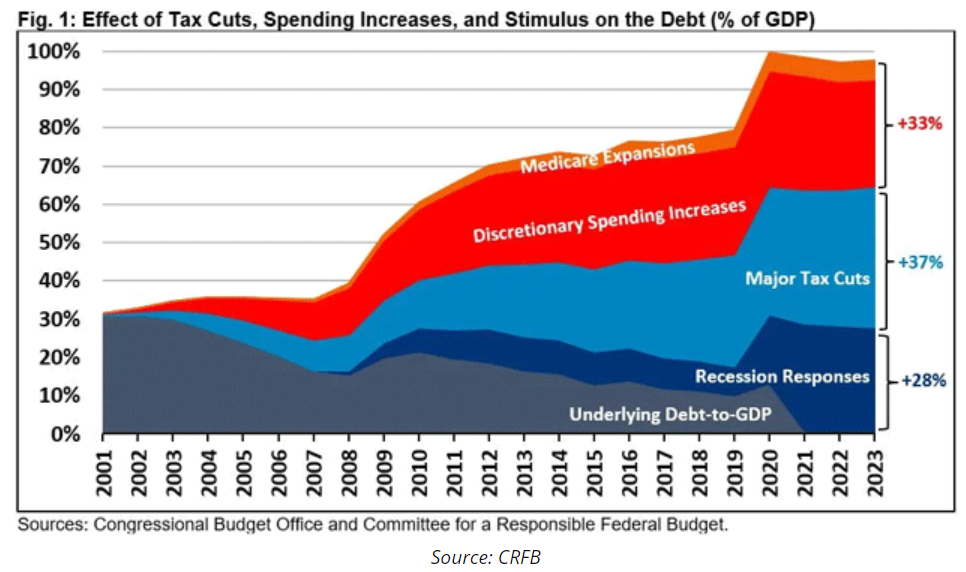

“In 2001, the Congressional Budget Office (CBO) projected that the national debt would effectively be paid off in full by the end of Fiscal Year (FY) 2009. Instead, federal debt held by the public grew from 32 percent of Gross Domestic Product (GDP) at the end of FY 2001 to 98 percent of GDP at the end of FY 2023.

“Reviewing major deficit-increasing legislation and executive actions over the past 22 years, we find that major tax cuts are responsible for 37 percentage points of debt-to-GDP, net discretionary spending increases and major Medicare expansions are responsible for 33 percentage points, and response measures to the Great Recession and the COVID-19 pandemic and recession—before accounting for economic feedback—explain 28 percentage points.

“Absent any two of these sets of policies, the debt-to-GDP ratio would be near the FY 2001 level. Absent these tax cuts, spending increases, and recession responses, debt would be fully paid off.”

John here again. It’s fair to wonder what skipping the “recession responses” would have done. Certainly, some of the spending was excessive and even counterproductive. But leaving millions to fend for themselves in a crashing economy might not have worked out so well, either. Even so, simply omitting the other spending increases and tax cuts over this period would have us in a far better position now.

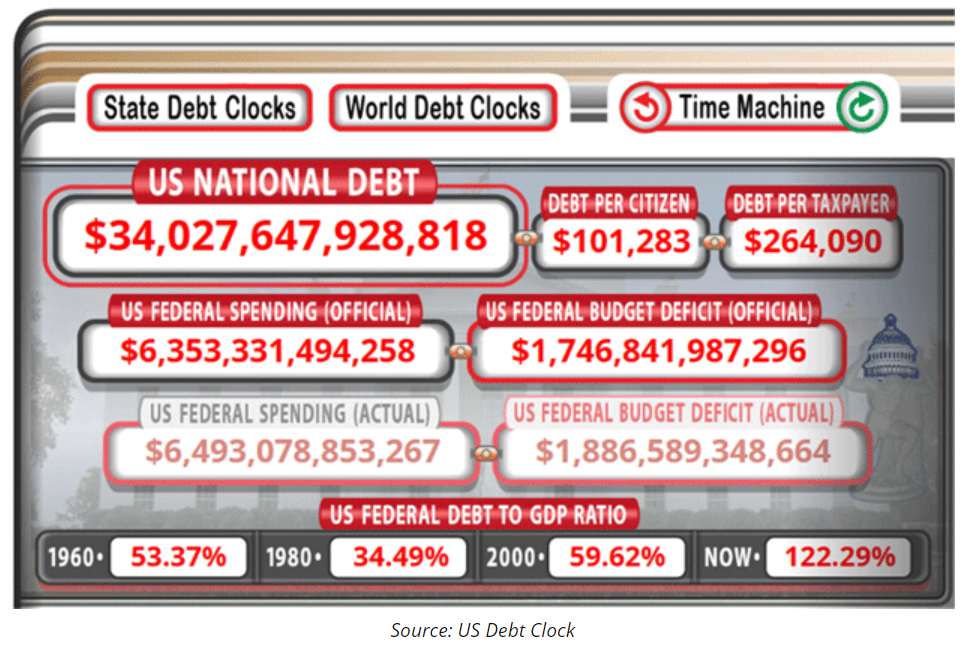

(Note: More than a few readers observed that debt-to-GDP is more than 98%. When the CRFB and most budget analysts talk about debt-to-GDP, they use “debt held by the public,” not counting the Social Security trust fund and similar arrangements. The all-in debt-to-GDP ratio is 122%, as tracked by that wonderful website USdebtclock.org.)

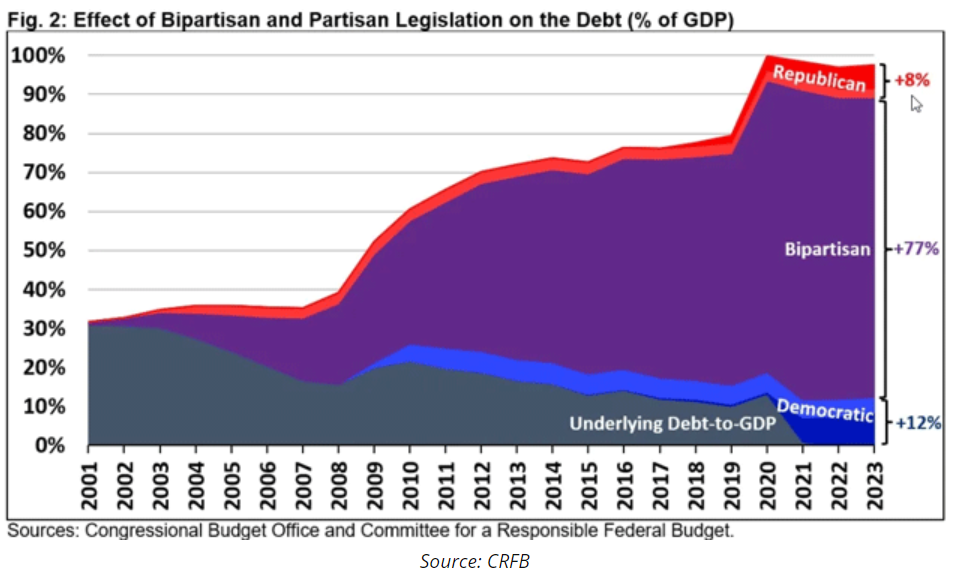

CRFB looked specifically at the tax and spending bills that account for the debt growth and found it was mostly bipartisan.

“Of the policies we reviewed, 77 percentage points of debt-to-GDP can be explained by legislation with some meaningful level of bipartisan support. Highly partisan Democratic actions explain 12 percentage points, and highly partisan Republican actions explain 8 percentage points. Many bipartisan actions extended policies that were originally more partisan in nature.”

John here again. Let me repeat that: CRFB finds 77 percentage points of the current 98% (122%) debt/GDP ratio can be attributed to legislation that passed with strong bipartisan support. That means the politicians were probably confident their voters would like it.

All this legislation was also scored by the CBO, so representatives and senators knew (roughly) what it would do to the debt. They did it anyway.

More debt growth is coming. Eventually, as I explained in that 2011 quote above, the bond market will stop absorbing it… and then we’ll have the crisis that forces change. I am hearing from my sources that the primary dealers who are responsible for buying US Treasury debt are beginning to wonder how they will absorb $9 trillion worth of debt this year? Yes, 80% of that will be rollover so should be manageable but at some point…?

Worse, there is a strong chance this debt crisis will coincide with the kind of cyclical social crisis I’ve described in this series. Neil Howe, George Friedman, Peter Turchin, and Ray Dalio (among others) have all warned us it will be bad. Add a debt crisis on top? We’d better buckle up.

We will get through it. We always do. But at what cost?

Naples, Washington, DC, NYC, and Cape Town

This Wednesday I fly to Miami and then drive to Naples to meet with Pat Cox and a few friends. I will be in the bar at the Ritz Carlton at 6:00 pm for an hour or so if you want to meet. Then I fly to Washington, DC, for a meeting on a new longevity drug and then take the train to New York for a series of meetings with my publishing partners, David Bahnsen, and other friends, flying back to San Juan the next Wednesday. Truly planes, trains, and automobiles.

A quick heads-up—as part of my 75th birthday year, I mentioned a month ago a fishing trip in northwest British Columbia at the end of August at the West Coast Fishing Club. This is not your usual fishing camp. It is a 5-star all-inclusive resort, truly world class, where you will be fishing for two types of salmon, halibut, and ling cod. You will fish from Boston Whalers with experienced guides (2‒3 per boat). They can arrange to have your fish shipped to you (even smoked). We have 30 spots reserved, and there are five left. You fly into Vancouver on a Wednesday night and stay at the Fairmont at the airport. We then fly out the next morning to Masset, northwest British Columbia, then take helicopters the next morning to the fishing camp on an island, spend 3 days fishing, then come back to the camp for gourmet meals. The food is amazing. Hot tubs, a spa, comfortable beds, and incredible company. It's a little over US $6,000. You show up in Vancouver and the rest is pretty much covered (except for massages, etc.). Email Tammi at [email protected] and she will put you in contact. It is pretty much first come, first serve for the remaining spots, although we may be able to pick up a few more.

And with that, it's time to hit the send button. I hope you enjoy your week as much as I intend to enjoy mine, with great conversations and good friends. And don't forget to follow me on Twitter X!

Your thinking about 30-lb. salmon and 40-lb.+ halibut analyst,

John Mauldin

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All