Waiting to Exhale: Commercial Real Estate Lending and Small Banks

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsStephen L'Heureux, CFA, Portfolio Manager, Global Commercial Real Estate & CMBS Strategist, Mortgage & Structured Finance and Julian Wellesley, Senior Credit Research Analyst

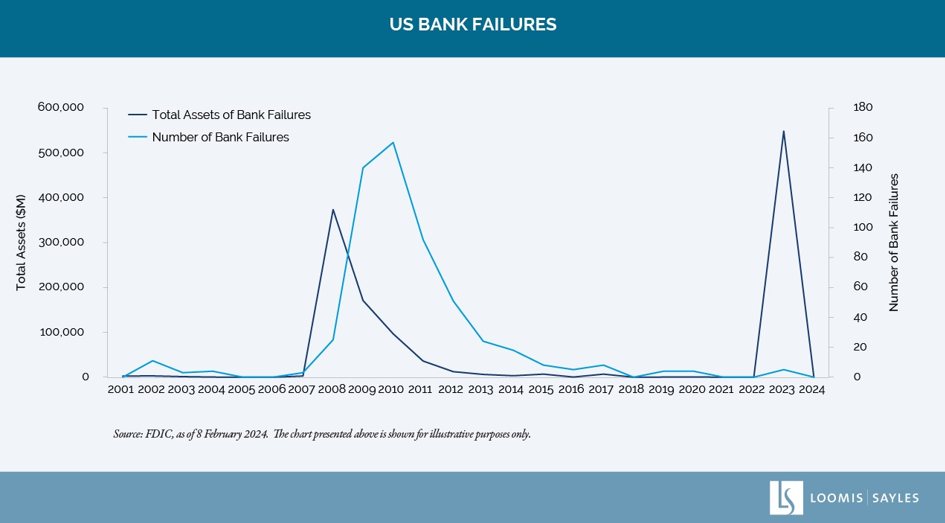

Throughout 2023, our analysts opined on risks related to commercial real estate (CRE) and their lenders. There was plenty to say about these sectors amid high vacancy rates, rising inflation rates, higher interest rates and the failure of three mid-size US banks and one large foreign bank—circumstances that left many investors holding their breath and wondering if there would be another shoe to drop.

In the following Q&A, two seasoned investment professionals, Stephen L’Heureux, a global commercial real estate portfolio manager and CMBS strategist, and Julian Wellesley, a senior bank credit research analyst, bring us up to date on the intersection of CRE and banks and whether it’s time to exhale.

Julian, who are the lenders to commercial real estate borrowers?

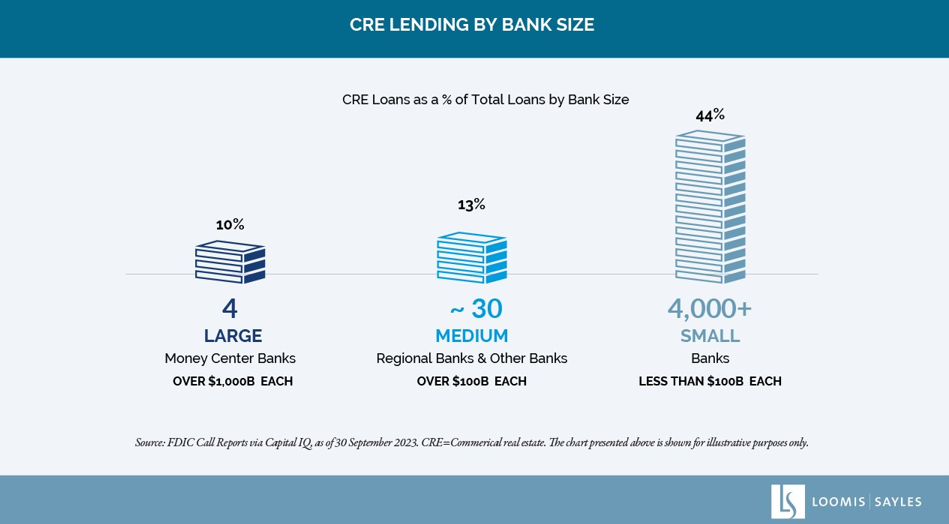

Banks provide approximately half of the total US commercial real estate debt, and most of that comes from smaller banks. 1 Other providers of CRE debt include government-sponsored enterprises, securitizations (CMBS and REITs) and insurance companies.

There are three groups that make up the 4,000+ US banking industry, and each makes up about one-third of US loans and deposits. Small banks have been growing CRE lending faster than large banks. This has contributed to small banks accounting for approximately two-thirds of total commercial real estate bank loans in the US, and many with high exposures to the asset class.2 According to FDIC reporting, CRE loans represented 44% of total loans made by small banks. That is in contrast to CRE loans as a percentage of total loans at the four large money center banks, which stood at 10%.

Julian, economic conditions have eased somewhat for the banking sector, how has this influenced your outlook?

In my view, conditions for banks and their commercial real estate borrowers have improved substantially since bond yields peaked in October. The risk of a recession appears to have fallen, and borrowers can likely refinance their debt more cheaply.

The Fed’s interest rate pivot and lower bond yields are positives for banks of all sizes. These factors have eased the headwinds that banks were facing in 2023. While non-performing loans have continued to grow, especially in the office and low-income consumer categories, most banks are not seeing widespread default risks in their loans outside of these two areas.

We expect banks’ non-performing loans to continue to increase in 2024—especially those related to office, multifamily and construction projects. Some smaller banks may run into trouble, but I am no longer worried about systemic risks from small banks’ commercial real estate exposures.

Non-performing loans weren’t banks’ only problem in 2023. Some banks had large unrealized losses on their securities portfolios. Therefore, capital quality was quite weak in some cases. While banks still have unrealized losses on their securities portfolios, levels have shrunk since October as bond yields declined.

Many banks also suffered deposit outflows and falling revenues last year—these continue but I expect revenue to stabilize in 2024.

Steve, are you concerned about the refinancing needs of CRE borrowers?

Yes. I have a less sanguine outlook for CRE. With nearly $1.2 trillion of loans maturing during the next two years ($660 billion of loans maturing in 2024 and another $540 billion in 2025), borrowers will likely face a challenging commercial mortgage market and this poses a tail risk for the financial sector.3 The US Office of Financial Research has joined the European oversight agencies in warning that commercial real estate loans will continue to pose a risk to financial stability.

We expect the lending environment to stabilize in 2024, albeit slowly and at very low levels. I think borrowers will find it increasingly difficult to refinance existing loan balances at maturity. Lenders are requiring new equity infusions to increase borrower equity in assets (required loan-to-value ratios have been reduced by 10%) while property values are down more than 20% from the March 2022 peak.4 For borrowers, underwriting requirements for debt-service coverage (the ability of asset income to make debt payments) have also tightened, reflecting operating headwinds for new construction in several sunbelt markets. At the time pf this publication, apartments and offices remain the weakest sectors, but other sectors are also under pressure. Although a tail risk, I believe that if there is a recession, the decline in commercial real estate values could persist into 2025.

Against this backdrop, underwriting standards will likely remain tight and the number of borrowers facing problems as loans mature will likely rise and could contribute to loan defaults. Banks prefer not to hold foreclosed property on their balance sheets. Refinancing of loans will be limited with many existing borrowers requiring loan extensions/modifications or recapitalizations of ownership structures. This situation will likely unfold over the next several years and limit upside. Banks’ CRE loans are typically floating rate, with about five-year maturities.

Steve and Julian, where do the regulators stand?

Steve: Regulators have encouraged banks to modify and extend loans. In July 2023, the Federal Reserve issued a policy statement encouraging banks to “work prudently and constructively with creditworthy commercial borrowers experiencing financial difficulties.”5 I think that loan modifications typically don’t work so well for construction loans which are not income-producing, or for income-producing properties with high vacancy rates.

Julian: Smaller banks that represent a significant part of the CRE lending base typically have less onerous oversight from regulators. Depending on the size of bank, there are different treatments for regulatory capital. For smaller banks, none of their unrealized losses on securities are reflected in their regulatory capital—a stark contrast to the biggest banks.

Steve, as we enter 2024, what indicators are you watching for insight into CRE health?

On the fundamental side, completions (additions to supply that raise vacancy rates and depress rents) are running ahead of absorption (demand for space) due to elevated starts during the past few years. This imbalance would need to be resolved before vacancy rates stop rising and rent softness recovers.

For property owners, the repricing of properties for high capitalization rates6 and mortgage costs is well underway, but owners continue to face operating headwinds. Weak rental market fundamentals and rising expenses threaten to slow growth rates for net operating income. Slowing aggregate income typically implies certain assets, sectors and regional markets will experience declining income. A recession would aggravate this weakness. We expect values, already down 22% from the recent peak (Green Street Market Index), to be down another 10% in 2024.7 A severe recession, which I do not expect, would lead to steeper declines.

For lenders, the erosion of borrower equity may be slowing, but challenges will shift to strains in property cash flows, which could lead to pre-maturity defaults. We expect delinquencies to rise in 2024. However, losses should be contained as lenders and their servicers continue to modify defaulting loans. This willingness to negotiate troubled loans is typically true of most lenders, but especially banks and insurance companies with regulated capital.

Do your contrasting outlooks mean it is too soon to exhale when it comes to CRE lending and borrowing?

While it may be too soon to exhale completely, in a sector where there are improved outlooks as well as continued causes for concern, there will likely be investment opportunities. It will be for us to accurately gauge valuations amid such a backdrop.

MALR032580

This blog post is provided for informational purposes only and should not be construed as investment advice. Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors only and do not necessarily reflect the views of Loomis, Sayles & Company, L.P. Information, including that obtained from outside sources, is believed to be correct, but Loomis Sayles cannot guarantee its accuracy. This material cannot be copied, reproduced or redistributed without authorization. This information is subject to change at any time without notice. Market conditions are extremely fluid and change frequently.

2 Source: Federal Reserve H.8 data. Smaller domestically chartered banks, outside the top 25 domestically chartered banks, accounted for 36% of total US bank loans, and 66% of commercial real estate loans as of 17 January 2024.

3 Source CRED IQ, as of 12 December 2023.

4 Green Street Market Index All-Property Index—a measure of pricing for institutional-quality commercial real estate, as of 5 January 2024.

5 Source: Federal Reserve joint press release, 23 June 2023.

6 Capitalization rate: operating income divided by current property valuation.

7 Source: Green Street Market Index All-Property Index—a measure of pricing for institutional-quality commercial real estate, as of 5 January 2024.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Live Virtual Event: Join Now

Upcoming Virtual Events View All