Franklin Fixed Income CIO Sonal Desai discusses why the January inflation print confirms that the “last mile” of disinflation may prove to be a lot harder than markets expect, and investors should brace for more volatility and a possible move of 10-year Treasury yields back in the 4.25%-4.50% range.

January’s US inflation print came as an unwelcome spoiler for financial markets, dealing what looks like the final blow to hopes of a March interest-rate cut, sending bond yields back up and triggering a major one-day correction in equities.

First, let’s put all this in perspective. Headline year-over-year inflation still came down—to 3.1% from December’s 3.4%—though remaining above the expected 2.9%. And the equity market correction, while a significant one-day move, still leaves in place the upward trend seen since October.

Having said this, there is a lot in January’s inflation report to support my long-held view that the “last mile” of disinflation is going to be a lot harder than markets expect, the Federal Reserve (Fed) will need to be very patient on monetary easing, and the new equilibrium we’re trending to will have markedly higher rates than we’ve been used to in the pre-inflation surge period.

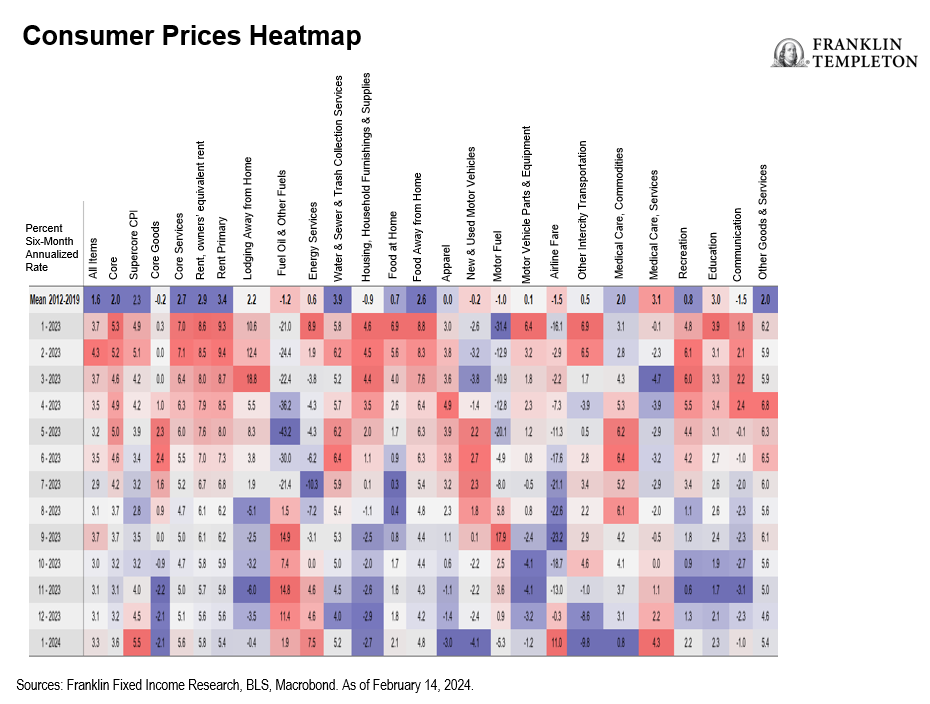

Start with “supercore” inflation, i.e., the price of services excluding energy and housing. The Fed has highlighted this as the measure that is likely most representative of underlying inflation trends and most sensitive to wage pressures. It was up 0.9% month-on-month, marking three continuous months of acceleration and the fastest pace of increase since April 2022. The acceleration was driven by medical services, recreation, education, communication, hotels, airfare and other intercity transportation—a rather wide range of categories. On a year-on-year basis, the supercore index change is well above 4%. More worrying still, on a six-month annualized basis, supercore inflation is now up 5.5%—not seen since late 2022 (see heat map below).

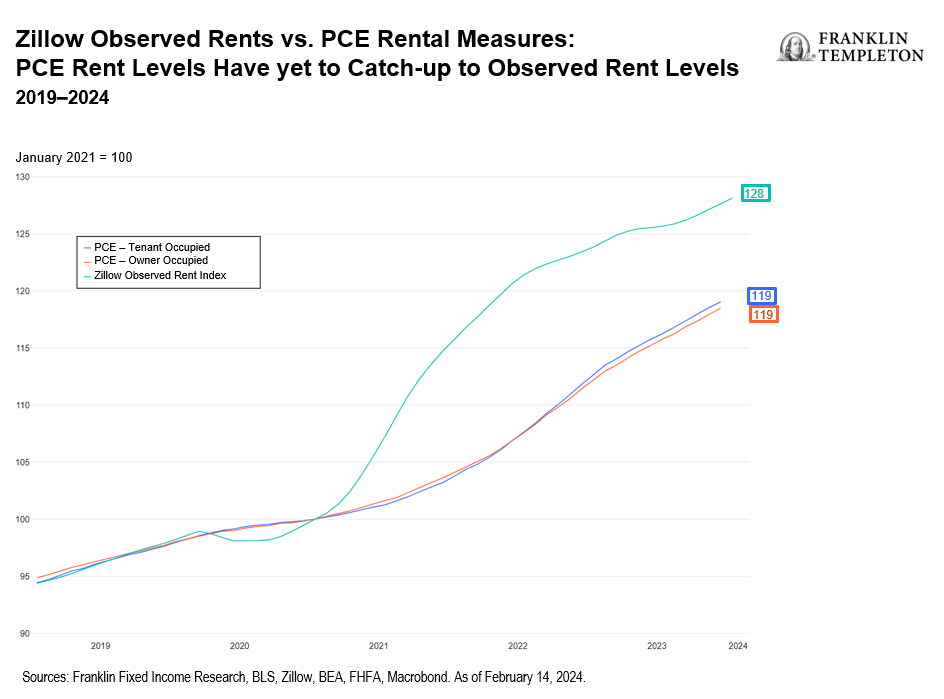

Looking at shelter, this component has been considered a reliable source of ongoing future disinflation, with the expectation that cheaper rental contracts feed into the inflation statistics with a lag. Here, we might be in for another disappointment. Owner-occupied rent accelerated in January. Moreover, my colleague Nikhil Mohan, economist and research analyst, Franklin Fixed Income, has highlighted that since early 2021, rents as measured in the personal consumption expenditures (PCE) have diverged substantially from rents as measured in the Zillow Observed Rent Index (see chart). In recent months, the increase in Zillow-measured rents has slowed, whereas the rent component in PCE keeps rising steadily, in a gradual catch-up. As you can see from the chart, PCE rents have a ways to go to close the gap with rent observed in Zillow. If a catch-up is indeed what is going on, we might still have quite a bit of pent-up inflation pressure in the rental cost component of inflation and therefore shelter might not contribute as much to disinflation as generally assumed.

Core goods prices declined for the third consecutive month. This is good news, confirming that the surge in core goods was largely transitory, and seems to be reversing with the normalization of supply chains.

Looking forward, however, I think we would do well to keep in mind three points:

- The US economy is obviously in rude health. We’ve seen strong numbers on the labor market, continued robust increases in wages, and upside surprises on consumer confidence, retail spending and gross domestic product growth. Against this background, it’s hardly surprising that disinflation has stalled. Yes, there was a transitory component due to supply disruptions which are now being resolved. But as I argued from the very beginning, higher inflation pressures partly reflected strong aggerate demand—and that keeps going. Supply has recovered, including with the productivity rebound I mentioned in my previous article, but not enough to offset continued strong demand.

- Supply shocks are not completely out of the picture. Disruptions in the Red Sea have already caused a rise in transportation costs that eventually might be passed on to consumers, and tensions in the Middle East show no sign of abating. And whether you look at China or Russia, geopolitical risks overall appear on the rise.

- Fiscal policy remains very loose, with very little chance of retrenchment now that we have entered an election year.

When you combine these three considerations with the signals in the latest inflation prints, the risk that inflation will prove stubborn appears significant—and by the way, measures of sticky inflation that the Cleveland Fed and the Atlanta Fed track send a very similar message. It does not mean a risk of inflation rising anew, forcing the Fed to consider additional hikes. But I think it does imply higher uncertainty on how long it will take before inflation is sustainably back to 2%.

The Fed has been wise to dampen market enthusiasm in the past few weeks, after having abetted the irrational exuberance of end-2023. To me, the second half of the year remains the most likely time for a first interest-rate cut, and chances that the fed funds rate might fall by more than 75 basis points (bps) this year appear slim. If anything, we might only see a reduction of 50 bps.

This is not the first time that markets’ fervent hopes of early and large rate cuts have been dashed—and it won’t be the last. Financial markets want to anticipate a significant monetary easing, and I think that when we get the next weak datapoint, or a Fed official making the next dovish statement, we’ll likely see rate-cut expectations surge again. To be dashed yet again, I would wager. So, brace for continued volatility, and I reiterate my call for 10-year Treasury yields in the 4.25%-4.50% range.

Finally, the long run: Activity data and inflation numbers all suggest that monetary policy is not too tight at all. In turn, this means that the neutral rate of interest is higher than what the Fed has penciled in and markets keep expecting. Some Fed officials have recently signaled as much, and I have made this point for quite some time, but it bears repeating—the neutral real rate is likely closer to 2% than to the Fed’s 0.5% estimate, and this implies that the neutral fed funds rate is likely closer to 4%. Investors should bear this in mind as they plan their investment strategy for the easing cycle.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Fixed income securities involve interest rate, credit, inflation and reinvestment risks, and possible loss of principal. As interest rates rise, the value of fixed income securities falls. Low-rated, high-yield bonds are subject to greater price volatility, illiquidity and possibility of default.

Equity securities are subject to price fluctuation and possible loss of principal.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S.: Franklin Resources, Inc. and its subsidiaries offer investment management services through multiple investment advisers registered with the SEC. Franklin Distributors, LLC and Putnam Retail Management LP, members FINRA/SIPC, are Franklin Templeton broker/dealers, which provide registered representative services. Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com.

Please visit www.franklinresources.com to be directed to your local Franklin Templeton website.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© Franklin Templeton Investments

More Volatility/Downside Protection Topics >