Investor sentiment and stock market valuations are getting increasingly stretched as indexes trek higher, but solid underlying breadth has been a positive offset for now.

As headline stock indexes have marched higher this year (and since the recent October 2023 low) without a serious pullback, investor sentiment has started to look increasingly optimistic and frothy, which we think is a building risk to the market (with caveats mentioned later). Unsurprisingly, those in the trend-following camp have grown increasingly excited as the S&P 500 has taken out its January 2022 high and crossed the 5,000 level.

What the duck

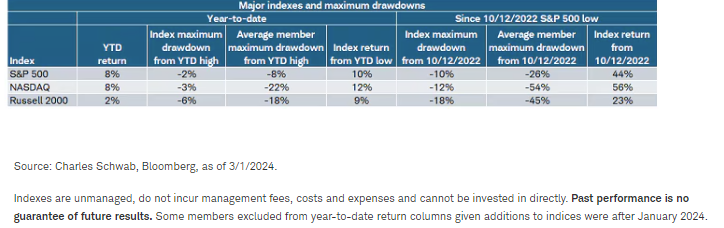

The reality is the stock market is acting a little more like a duck than a bull: calm on the surface but paddling like the dickens underneath (chef's kiss to Michael Caine, who coined that phrase). Check out the performance table below, which is posted on my (Liz Ann's) X feed every morning. Per the third column, the S&P 500 and Nasdaq have suffered no more than a -3% drawdown from a year-to-date high—but that's at the index level. Looking under the surface yields a very different picture. Although not as extreme for the S&P 500, the average Nasdaq member maximum drawdown from year-to-date highs is a whopping -22% (yes, that's a bear-market-level decline).

Glancing at the right half of the table above, you'll see even sharper extremes of churn under the surface. Since the major market lows of October 2022, the S&P 500 is up 44% (far right column), but the index's average member maximum drawdown has been -26% over that same period. In the case of the Nasdaq, those performance numbers are +56% and -54%, respectively.

[There is an important aside with regard to the Nasdaq. Per Leuthold Group research, the number of Nasdaq-traded securities ballooned by nearly 60% (about 2000 new issues) from mid-2020 to mid-2022. Not all of those issues were companies with real operations. Some of them were warrants and others were special purpose acquisition companies (SPACs), which can distort a variety of breadth measures.]

Generals vs. soldiers

We've written and spoken extensively about market breadth. It's unfortunate, with two wars underway, that a battlefront analogy is most illustrative. When it's only a few generals on the front line—even if they're five-star generals—and the soldiers having fallen behind, it's not a strong front. Conversely, even if a general or two falls behind, if more soldiers have moved up, it's a stronger front.

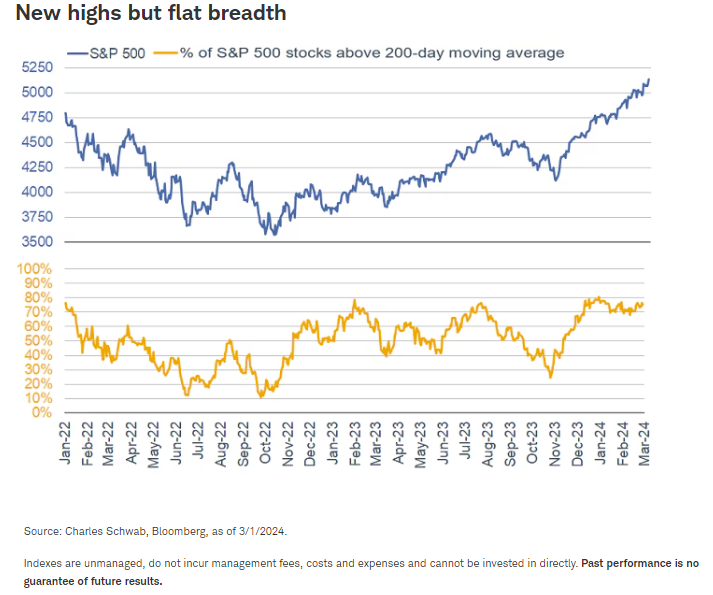

As shown below, this year has been marked—so far—by the S&P 500 marching to an all-time high (top part of chart), yet the percentage of stocks trading above their 200-day moving averages (bottom part of chart) has been flat. The early part of the rally off last October's low was accompanied by a sharply rising share of stocks trading above their moving averages; but that has clearly faded over the past couple of months.

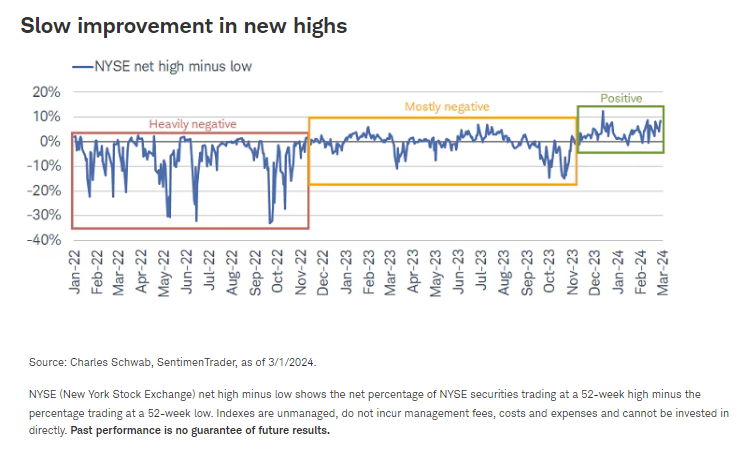

Another breadth measure—and a trademark of healthy bull markets—is a growing percentage of stocks hitting 52-week highs relative to 52-week lows. As per SentimenTrader data, and shown in the chart below, across the very broad New York Stock Exchange (NYSE), more securities have been recording new highs than lows, which is a stark change from 2022 and even most of last year.

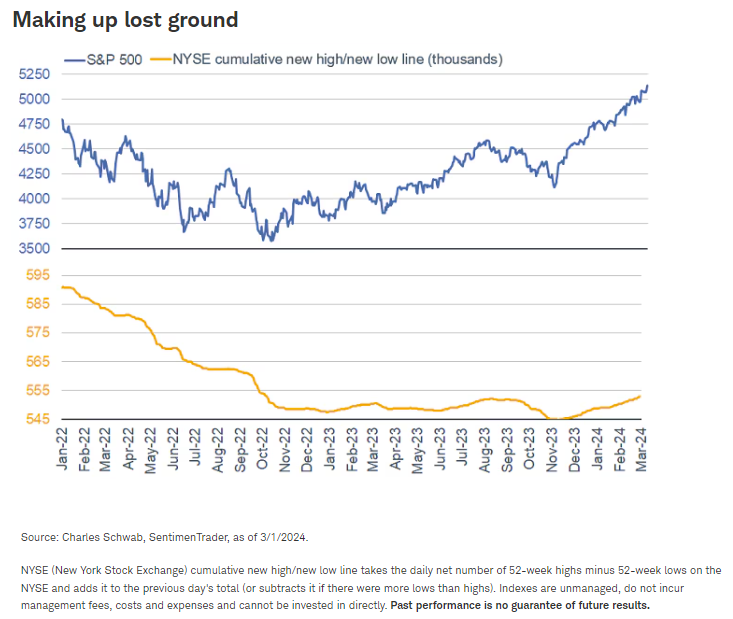

There's a caveat, highlighted in the chart below. So many NYSE issues fell to 52-week lows in 2022—with 2023 not offering a lot of improvement—that the past few months have only made a slight difference in the cumulative new high/new low line. It has started to turn higher, but more work needs to be done here.

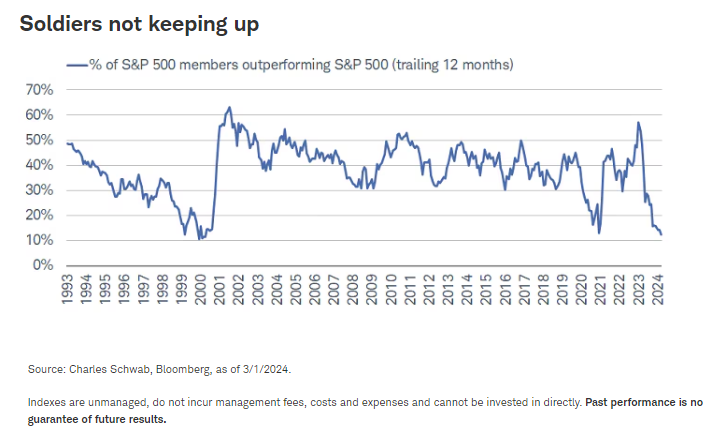

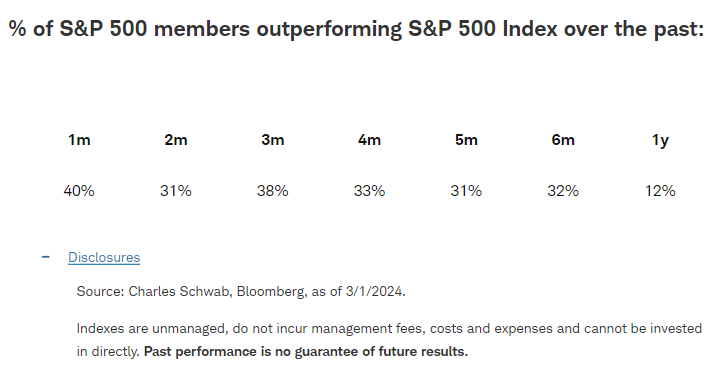

Notwithstanding some improvement in breadth, as shown below, it's still the case that a historically low percentage of S&P 500 stocks have outperformed the S&P 500 over the past 12 months. This is improving over shorter trailing spans, as shown in the table below the chart. In fact, over the past month, 40% of S&P 500 stocks have outperformed the index. This is improving news, but more soldiers need to continue to advance.

Not as "mag" anymore

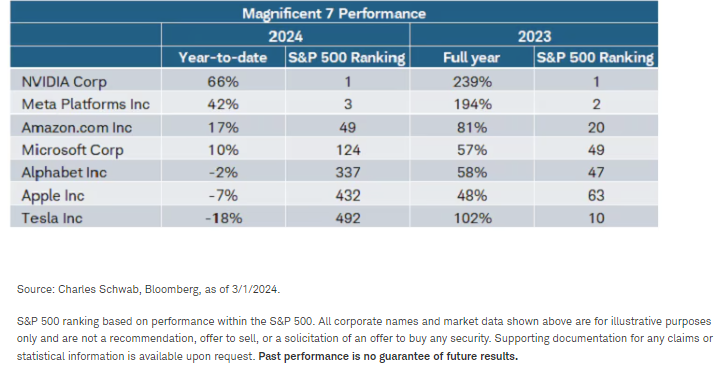

The obsession over the so-called "Magnificent 7" (Mag7) group of stocks hasn't abated, but again, under the surface is where the real story is told. The moniker was originally based on capitalization—with the stocks representing the seven largest stocks by market cap in both the S&P 500 and Nasdaq. Interestingly, they are no longer the largest seven stocks, with Tesla having dropped out (and leap-frogged by Berkshire Hathaway and Eli Lilly, with Broadcom closing in as well).

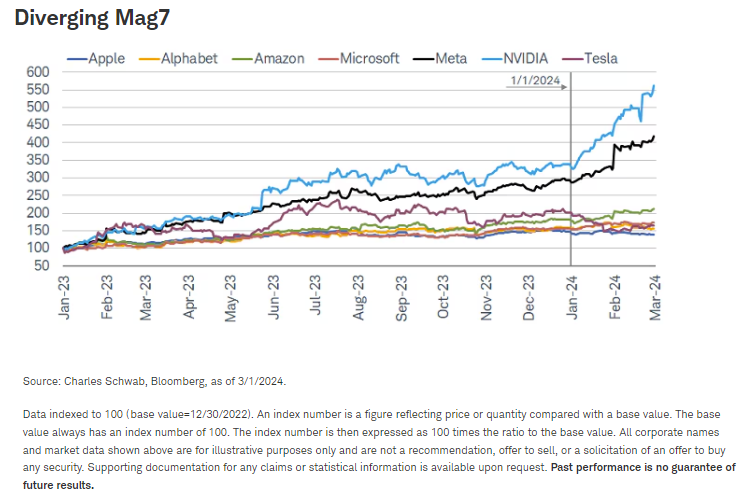

The chart below shows their performance since the beginning of 2023, and what's clearly noticeable is the widening divergence in performance so far in 2024 vs. 2023.

As shown in the right side of the table below, all seven Mag7 stocks were strong performers last year—up double- or triple-digits and ranked within the top 13% of the S&P 500 index. But what a difference the turn of the calendar has made. As shown in the left side of the table, so far this year, the performance ranges from +66% to -18%, with Tesla and Apple having fallen to near the bottom of the performance ranking pack.

Party like it's 1999?

Lots of comparisons are being made between the dominance of a small handful tech and tech-related stocks driving performance over the past year and the dot-com bubble leading into 2000. We think there are important differences today; not least being less of a "denominator" problem (i.e., an earnings problem or the E in P/E) today relative to the late 1990s, when profits for many companies were (pipe) dreams, not reality.

During the fourth quarter of last year (the books are just closing on its reporting season), top-line growth for the Mag7 was 15% year-over-year. Profit margins were up more than 600 basis points year-over-year, which resulted in year-over-year earnings growth of about 60%. To put that into perspective, the remaining 493 stocks in the S&P 500 actually lost money last quarter, with a year-over-year earnings decline of about 2%.

Valuations are undoubtedly stretched for the Mag7, but they have some of the strongest balance sheets of all U.S. companies, generating gobs of free cash flow. Per Goldman Sachs analysis, the Mag7 reinvests about 60% of that cash flow into capital spending and research/development, which is more than three times what the other 493 companies reinvest.

Yes, the stocks are over-owned and richly valued, but all-or-nothing makes less sense than periodic rebalancing in the interest of keeping concentration risk in your own portfolios at bay. In the meantime, there is a widening array of stocks stealthily performing better this year. We continue to emphasize a factor-oriented approach (screening/investing based on characteristics), with focus on quality-oriented factors like strong free cash flow, ample interest coverage, positive earnings trends, etc.

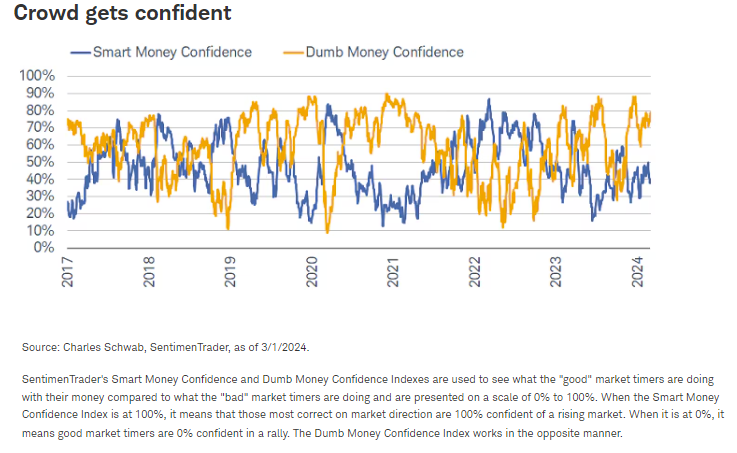

Everyone's feeling good

Enthusiasm around the Mag7 and other megacap stocks has contributed to a stretched sentiment environment. As shown in the chart below, SentimenTrader's (ST) "Dumb Money Confidence" (DMC) is back in excessive optimism territory and hovering near the upper end of its historical range. That's mostly to be expected, given the DMC crew tends to get most exuberant at market peaks and most dour at market bottoms. Conversely, the "Smart Money Confidence" (SMC) crew usually turns quite bullish at market bottoms and thus moves inversely with the DMC.

Yet, in an odd twist, both confidence indexes have moved higher recently. Per ST, there have only been five prior instances in the DMC and SMC indexes' history when both increased by at least 10% over the prior month and were at or above the 50% threshold (as is the case now). Forward returns in those periods—1999, 2004, 2007, 2013, and 2023—were mixed, especially since two of those years preceded rough bear markets.

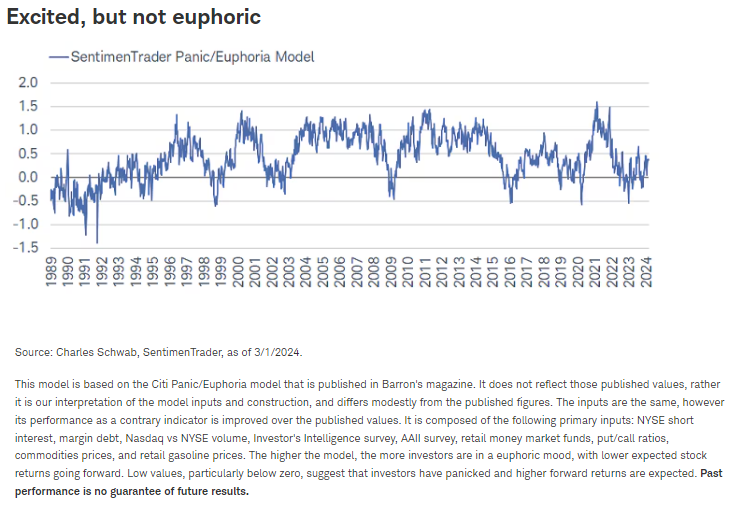

Corroborating the excitement expressed in DMC has been a move higher in ST's Panic/Euphoria Index, which is based off the version originally created by the late, great Tobias Levkovich at Citi. We like it because it's an amalgamation of sentiment indicators across the attitudinal and behavioral spectrum. As shown below, the index has climbed from its low point at the end of 2022; but fortunately, it isn't anywhere near peak euphoria levels of past cycles.

The good news is that the index's current level is supportive of sentiment being able to run hotter and the market having more runway ahead. The rub is that certain components within the index have gotten quite stretched and are consistent with increasing levels of frothiness. Flows into equity funds (particularly high-flying areas like the Tech sector) have gotten aggressive, the equity put/call ratio is hovering near the lower end of its historical range, and the American Association of Individual Investors (AAII) bull/bear spread is quite high, among others.

Pay up

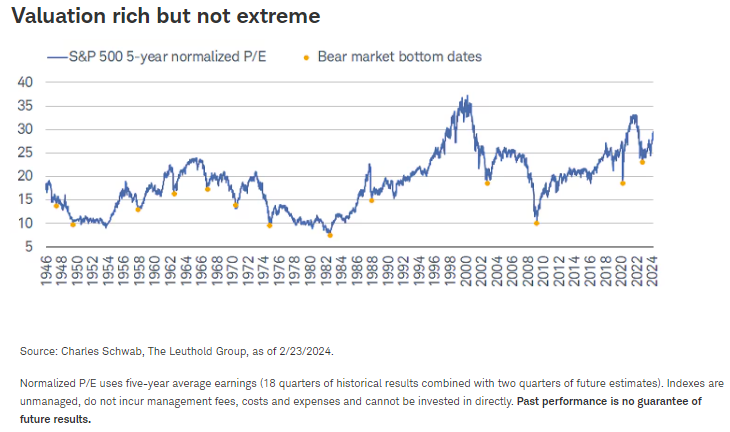

Tying this all together, it's worth noting that the market has gotten more expensive as sentiment has grown more exuberant. Shown in the chart below is the five-year normalized price-to-earnings (P/E) ratio for the S&P 500. This comes from our friends at The Leuthold Group and uses four-and-a-half years of trailing earnings data, combined with two quarters of forward estimates to get a smoothed "E" component in the P/E.

With the market having surpassed its January 2022 high, we can now definitively say that the October 2022 low for the S&P 500 was the most expensive trough in history (shown via the far-right yellow dot in the chart). It didn't take long in the market's run since last October to get back to the expensive end of this P/E's historical range. However, like the Panic/Euphoria Index, it's not yet back to extremes seen in prior cycle peaks.

This gets to two important points we like to emphasize whenever talking about valuation and sentiment. First, we like to think of valuation as a sentiment indicator; or better yet, an indicator of sentiment. There have been times—like in early 2009 and during most of the 1970s—when investors weren't willing to pay anything for stocks. There have also been times—like in the late 1990s and throughout 2021—when investors were willing to accept nosebleed valuations. Today, we're getting closer to the latter environment.

Second, and related to the earlier points made about sentiment, frothy sentiment in and of itself is not a contrarian market timing tool (and vice-versa in times of pessimism). It is true that for many sentiment metrics, the current zone of optimism tends to be consistent with weak forward equity returns; however, a negative catalyst is typically needed to push stocks in the other direction. This could come in the form of surprises in economic and/or inflation data, adjustments in the outlook for Federal Reserve policy, or a breakdown in the market's underlying breadth.

In the meantime…

Investor sentiment and valuation are stretched, but there have been some signs of improving market breadth. With indexes like the S&P 500 and Nasdaq trading at/near all-time highs, but with lots of churn under the surface, investors should be mindful of concentration risk within their own portfolios. Periodic (and portfolio-based) rebalancing can help alleviate that concentration risk and stay in gear with the market via "adding low and trimming high." For those investors looking for opportunity amid the churn, we recommend staying up in quality and using a factor-oriented approach.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk including loss of principal.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Performance may be affected by risks associated with non-diversification, including investments in specific countries or sectors. Additional risks may also include, but are not limited to, investments in foreign securities, especially emerging markets, real estate investment trusts (REITs), fixed income and small capitalization securities. Each individual investor should consider these risks carefully before investing in a particular security or strategy.

All corporate names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security. Supporting documentation for any claims or statistical information is available upon request.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

Rebalancing does not protect against losses or guarantee that an investor's goal will be met. Rebalancing may cause investors to incur transaction costs and, when a non-retirement account is rebalanced, taxable events may be created that may affect your tax liability.

Schwab does not recommend the use of technical analysis as a sole means of investment research.

Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

Indexes are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. For additional information, please see schwab.com/indexdefinitions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Charles Schwab

More Large Cap Growth Topics >