Climate Risk Heats Up

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsClimate risks and regulations are on the rise.

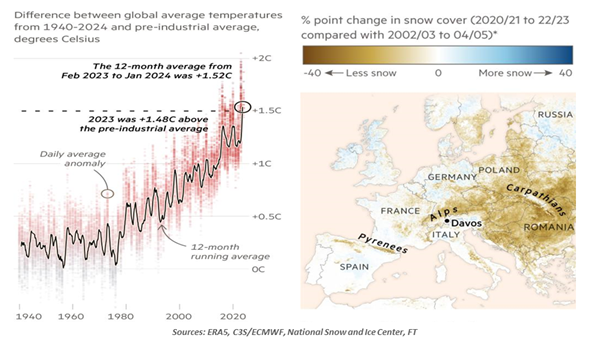

I am struck by how regularly I was able to run outside last month. Chicago’s harsh winter conditions typically limit outdoor activity; even hardy, warmly-dressed runners will stay indoors to avoid injuries from the frozen ground. But this year, locals did not need to spend as much time on treadmills. Most of the U.S. had its warmest February on record, while the rest of the world logged the second-warmest February in history. Weather patterns are shifting, and the consequences go far beyond planning exercise routines.

We are economists, not meteorologists. We must take the changing weather as an exogenous shock, and make plans to deal with the commercial and policy implications of these changes. And the outcomes are starting to show up everywhere we look.

The increasing prevalence of droughts, wildfires and heavy storms are adding to the risks faced by food industries. Crop failures have become more common. Livestock eat a lot of grains and grass; higher input costs will raise the price of meat. Fish are also under stress, with changes to the temperatures and acidity of the oceans causing species to move or be depleted.

Ensuring a secure supply of food is a minimum requirement of the governments of most nations. Imports can compensate when local producers are impaired: in 2022, food shipments helped to compensate for the loss of commodity output from Ukraine. But if the whole world’s harvests are at risk, governments will need to contemplate more comprehensive responses.

Food is not the only supply chain at risk. The Panama Canal was designed to use nearby freshwater lakes to fill its locks. A drought has diminished available water, preventing larger vessels from crossing the canal. Ships must instead traverse the length of South America around Cape Horn, slowing shipments and adding to costs. (This challenge mirrors the rerouting away from the Middle East due to tensions in the Red Sea.) We do not anticipate the COVID-era challenges of everything going awry in supply chains, but the episode did teach us the difficulty of restoring normality once a disruption begins.

Those seeking respite from stress will have to get creative, as well. Warmer tourist destinations will need to contend with shifting shorelines and limited fresh water supplies. Colder climes will also need to adapt: snowfall has become more limited, reducing the number of viable destinations for skiing and winter exploration.

CLIMATE RISKS ARE NOT DISTANT; THEY ARE WITH US TODAY.

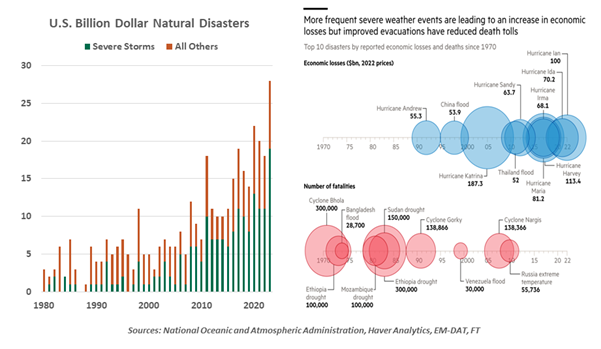

The tangible costs of climate change can feel far-off or overstated. After all, store shelves are still full of food, and anyone who has experienced a blizzard will not be too upset by warmer winters. But the actual effects are becoming harder to ignore, especially in the costs of insurance.

The frequency and severity of major storms is rising, in large part due to warmer oceans bringing more energy into storm systems. Even events like thunderstorms, once considered “secondary perils” to insurers, are showing potential to cause catastrophic damage. Many homeowners are finding themselves priced out of insurance, and living at risk of total loss of their homes. Studies have estimated seven percent of U.K. homes and one in 25 Australian homes will be forced to forego insurance in the decades to come. In the U.S., insurers are simply terminating policies and withdrawing from hurricane-prone markets like Florida and the Gulf Coast.

Private sector initiatives like ESG investing are doing their part, but that part is small. Governments must act to arrest overheating. Policy responses to climate change have had mixed success. Emissions trading schemes did not see global adoption, allowing rich nations to continue buying from polluting exporters.

The European Union has started implementing a carbon border adjustment mechanism (CBAM) to levy an import tax on carbon-intensive imports like steel, cement and fertilizers; the tax will take effect in 2026. The European Commission is also considering a corporate sustainability due diligence directive (CSDDD) that would require companies to include environmental and human rights considerations in their governance. In the U.S., the Securities and Exchange Commission has just finalized a rule requiring firms to report their emissions, climate targets and risks as part of their financial disclosures. The U.S. remains a significant polluter, alongside India and China—all nations that have done little to curb their emissions.

Central banks are also contemplating climate risks. While it may seem beyond central banks’ remits, climate events can affect the economy, markets and the banking system. The European Central Bank’s vice-chair of supervision gave a speech last year anchored on climate jeopardizing financial stability. Bank of England governor Catherine Mann defended the role of central banks in climate policy, as both climate events and mitigating strategies like carbon taxes will impact inflation. Mann keenly observed that central banks often think in terms of risk scenarios, but in this case, “there is no ‘no climate change’ scenario to fall back on.” The Federal Reserve has begun a pilot of climate risk scenario analysis, though Chair Powell has expressed caution that the Fed will not be a climate policymaker.

The challenge of climate change requires global coordination. Even in times of peace, this would be a tall order; in the current era of high polarization, any response will be fraught. But the time for risk identification and mitigation is upon us, and will inform many aspects of our work indefinitely. Despite the greater window for training, we cannot run from this risk.

CLIMATE-RELATED RULES WILL COME FROM MORE THAN JUST THE ENVIRONMENTAL REGULATORS.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2024 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All