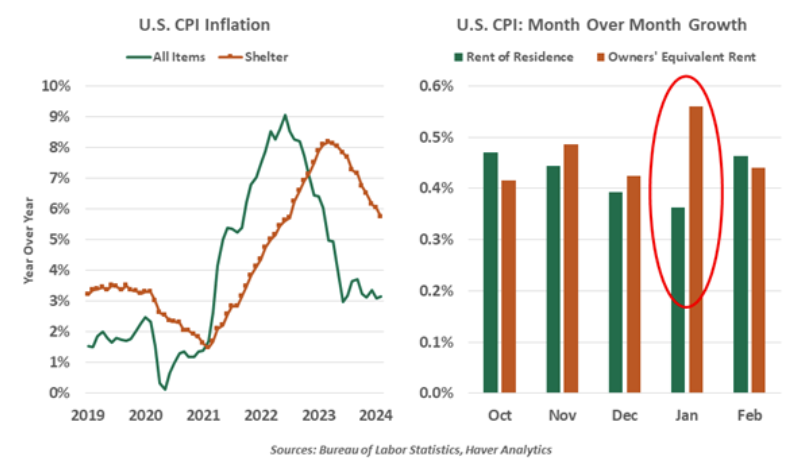

Shelter costs are keeping inflation measures elevated.

The importance of the housing market has led us to focus on it across many dimensions. We have discussed its short supply, the role of mortgages as a defense against inflation and promises of greater residential investment. Today, housing has captured our attention as a consequential and frustrating driver of inflation.

Shelter costs followed headline inflation up in this cycle, but have remained stubbornly elevated even as most other components improved. The majority of U.S. households own their homes; in the consumer price index (CPI), their monthly costs are captured by a concept called owners’ equivalent rent (OER). The measure is theoretical; it does not use actual house prices or interest rates, which combine to drive mortgage costs. Its impact on inflation is significant, as OER represents over 25% of the CPI basket (and combined with rent, the shelter category exceeds 35% of the CPI).

High housing inflation is casting more attention on these measures, and a divergence in their growth rates in January was alarming. The rent and OER indices usually move in tandem, as they are closely related. In January, the two measures grew at starkly different rates.

As part of routine annual benchmarking, the weights in the OER formula were rebalanced to add 5% more weight toward single-family detached housing. Rents on these units have been growing more rapidly than they have for apartments, which created the jump in inflation. The weights are now fixed for the year ahead, and further divergence is unlikely—at least, until the next reset.

The surprise was magnified after the Bureau of Labor Statistics (BLS) emailed a more detailed explanation to a subset of “super user” economists who had inquired about the surprise. The BLS then clarified that no new information was contained in the message.

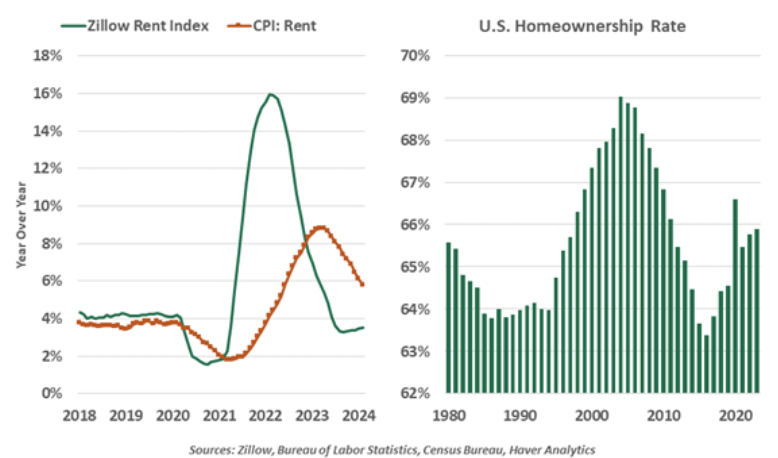

The episode highlights the current sensitivity to housing as we grapple with the outlook for inflation. After collapsing in 2020 and then recovering, the CPI measure of rents is growing almost twice as fast as alternative indicators of asking rents (such as the Zillow index shown in the chart). Economists have been expecting the two to converge, but the process has been slow.

The measures use different reference sets, which may explain the different trajectories. Indices published by Zillow or Redfin draw from listed vacancies on their own portals, often large buildings under professional management.

The BLS draws from consumers’ reported expenditures; their housing costs encompass a much wider variety of property types. Most homeownership is of single-family detached homes, which are less likely to be listed on large rental data aggregation platforms. Further, rentals on detached homes are rare, making it difficult to calculate the OER.

HOUSING COSTS MAY NOT EASE AS QUICKLY AS WE HAD HOPED.

All of this casts some doubt over the notion of when and whether shelter costs will moderate. The outlook for housing remains a story of strong demand and constrained supply. The prices of and rents on property will continue to be supported by tight labor markets and a growing population; we are still in need of places to live.

Bringing shelter costs under control will be vital to holding down inflation and managing expectations. When shelter is excluded from the CPI, we find that price growth has been below 2% for nine months in a row. The housing line is one of the first we look at when new inflation data comes out; we expect that it is the same way within the Federal Reserve.

The forces holding up shelter prices, like a growing population and longer lifespans, are good problems to have. But until the stock of dwellings catches up with demand, the high cost of housing will remain a burden.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2024 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© Northern Trust

Read more commentaries by Northern Trust