The Bank of Japan (BoJ) raised interest rates for the first time since 2007 and has eliminated the yield curve control framework. Franklin Templeton Fixed Income Economist Rini Sen expects the bulk of further tightening will likely come in 2025 as the BoJ seeks to reach a sustainable 2% inflation target by end of fiscal year 2025.

The Bank of Japan (BoJ) tightened monetary policy at its March 19 meeting, abolishing the yield curve control framework and raising rates to 0.0%-0.1%, for the first time since 2007 (in a 7-2 majority vote). According to the central bank, the virtuous cycle between wages and prices was assessed to have come into sight, bringing the 2% inflation target within a sustainable and stable possibility by the end of fiscal year 2025 (March 2025). With this, the 1.00% soft cap on the 10-year Japanese government bond (JGB) yield was also removed.

Other major changes to monetary policy were: 1) abolishing of the overshooting target (of the monetary base), 2) a reduction in the upper ranges of JGB buying across tenors (but the lower range was kept unchanged meaning that current pace of buying will continue, seemingly disappointing bond bears) and 3) an end to purchases of exchange traded funds and Japanese real estate investment trusts with a reduction in purchases of commercial paper and corporate bonds, which would eventually discontinue in a year’s time.

The BoJ also said it will continue to conduct emergency purchases of JGBs if yields were to rise significantly and will maintain accommodative financial conditions going forward. As we had previously expected, this seems to rule out an aggressive tightening trajectory.

In our opinion, three major factors guided today’s BoJ pivot, and it had been slow to accept growing inflationary concerns as enough to warrant a change.

The first was the upward revision in the final fourth-quarter gross domestic product numbers, which showed that Japan averted a technical recession. In fact, the BoJ noted that the economy has recovered modestly, although some weak points remain. Industrial production and machinery orders are subdued as auto production disruptions continue to impact shipments. Business investment has been largely flat with housing and public investment weak.

However, we do expect business sentiment to turn, as corporate profits gather steam and firms look to enhance production and productivity leading to higher wage growth, rather than suppressing investments and costs, as has been the case in Japan for decades. Domestic demand will likely improve in the second half 2024, which we believe should give the BoJ further ammunition to move ahead in its tightening path.

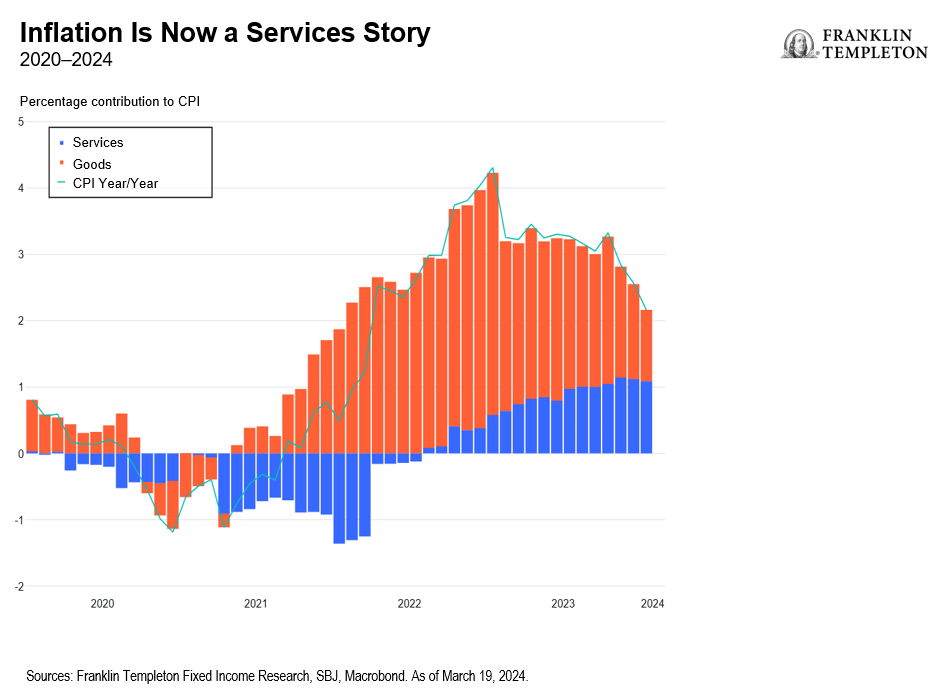

Second, after successive revisions to its inflation forecasts and assessing whether what initially started as a supply shock did turn into a demand-pull inflation problem, the BoJ has found that a virtuous wage price spiral is in the works. We have long argued that a structural change is underway in Japan’s inflation dynamics—firms are passing on higher input costs to end users, utility companies are revising tariffs periodically, inflation hedges are gaining popularity, and wages are lifting slowly. Although many would argue that Japan’s demographics should have already pushed the inflation risk higher, the tailwinds from extensions in the retirement age and more working women are wearing off (labor-force participation rates for men and women aged 55-64 stood at 80.8 in January 2024 and that of women aged 15-64 stood at 74.9, both up from 68.1 and 62.1 in January 20121). A part of this is already evidenced in rising services within the Consumer Price Index (CPI), which is now the bigger contributor to overall inflation as goods prices recede.

Exhibit 1: Japanese Inflation Is Now a Services Story

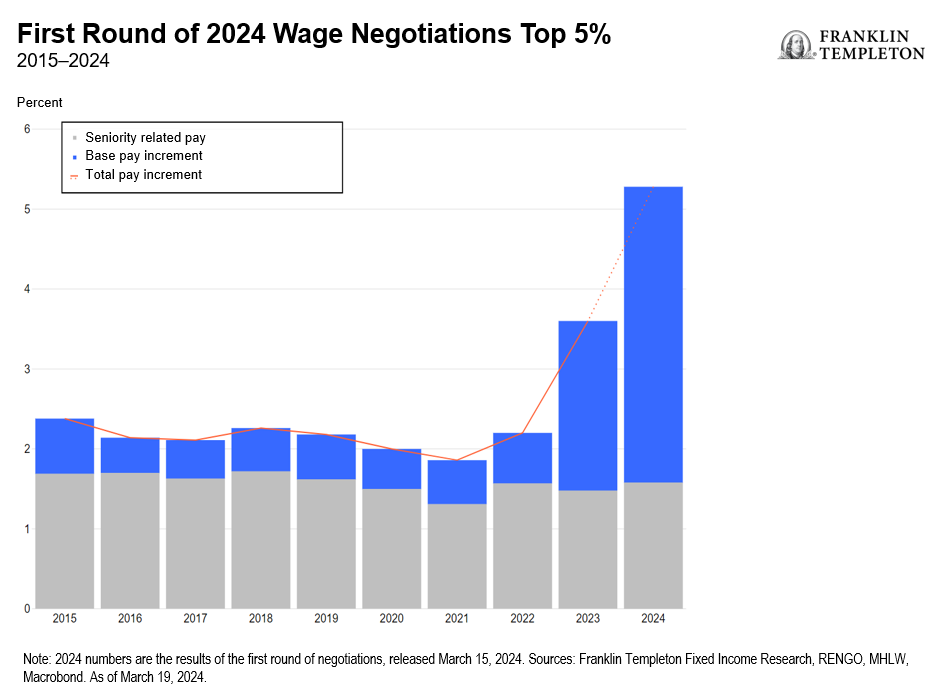

The third and admittedly (by the BoJ) the biggest driver for the policy move was the strong wage gains in the first round of this year’s Shunto wage negotiations (see Exhibit 2 below). As reported by Rengo, Japan’s Trade Union Confederation, the first round yielded a total wage hike of 5.28% with base wages at 3.70%. For perspective, the 2023 average wage gains stood at a total 3.60%, with 2.12% gains in base pay. Larger firms including the likes of Toyota and Nissan do make up the bulk of the initial rounds of negotiations, and past data has shown subsequent rounds drag the overall averages lower (as smaller firms make up the majority in later rounds and are usually unable to match the magnitude of hikes). However, the central bank has mentioned it expects sharp gains even from smaller firms in the weeks ahead, as heard anecdotally.

Even if we consider a marginal adjustment lower, a full year pay increase of close to 5% will still be the highest recorded wage gain since 1991. The second and third rounds of the negotiations will be declared on March 22 and April 4, respectively.

Exhibit 2: Wage Negotiations in Japan

These developments helped the BoJ to finally make a move, but we think the pace of adjustment will be gradual. Governor Kazuo Ueda’s press conference largely bordered on neutral, mentioning that future rate hikes will be contingent on inflation. We remain of the view that inflation will be stubborn and sticky, with the path of wage gains, household spending, private consumption and the extension of subsidies (especially energy which are due to end in April) governing the trajectory. The BoJ will likely be data-dependent in its future course of action. We will be also watchful of incoming data, which is why we expect the bulk of the tightening to come in 2025 (with likely two smaller hikes in 2024).

In the next few months, wage data should start to reflect the ongoing Shunto gains, energy and other COVID-19 related subsidies (like on travel, accommodation, etc.). And, their impact on CPI would have worn off and growth would have sufficiently turned a corner.

The markets have seemingly taken the huge buildup of the end to negative Japanese rates in their stride. We think in a way, the BoJ warmed markets into it, not least because of its tedious decision-making. We expect this watchful process to continue, with subsequent policy tweaks to give enough backdrop to not spur a surprise.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Fixed income securities involve interest rate, credit, inflation and reinvestment risks, and possible loss of principal. As interest rates rise, the value of fixed income securities falls. Low-rated, high-yield bonds are subject to greater price volatility, illiquidity and possibility of default.

Equity securities are subject to price fluctuation and possible loss of principal.

International investments are subject to special risks, including currency fluctuations and social, economic and political uncertainties, which could increase volatility.

Any companies and/or case studies referenced herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton. The information provided is not a recommendation or individual investment advice for any particular security, strategy, or investment product and is not an indication of the trading intent of any Franklin Templeton managed portfolio.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S.: Franklin Resources, Inc. and its subsidiaries offer investment management services through multiple investment advisers registered with the SEC. Franklin Distributors, LLC and Putnam Retail Management LP, members FINRA/SIPC, are Franklin Templeton broker/dealers, which provide registered representative services. Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com.

1. Source: Statistics Bureau of Japan. As of March 19, 2024.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments