Thought to ponder…

“Because of the spirit, I say. Because of the heart. Writing and reading decrease our sense of isolation. They deepen and widen and expand our sense of life: they feed the soul.”

- Anne Lamott, Bird by Bird

The View from 30,000 feet

Thursday marked the final trading day of the week, month and quarter. It seemed only fitting the two major data releases on Thursday delivered the overarching message of 2024 – better than expected growth, mixed with a downshift in the disinflationary trends of last year. On Thursday, Q4 2023 GDP was revised higher and Q4 2023 GDI was released, showing a catch up between GDI and GDP, that squashed the dreams of many a bear. Earlier in the week the Atlanta Fed GDPNow was also revised higher, now projecting Q1 2024 grew at a 2.3% annualized rate. Strategists have been scrambling all quarter to upgrade their GDP and equity market forecasts for 2024, but still look behind the ball, as the both the economy and the equity markets continue to surprise on the upside.

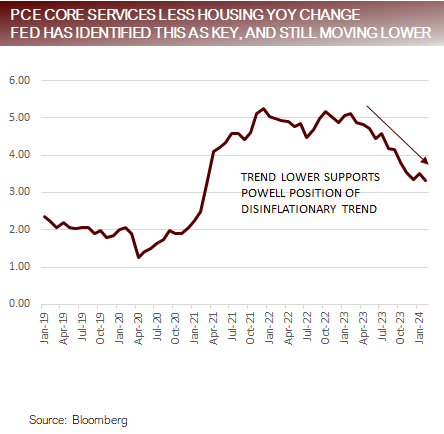

Thursday’s PCE release was inline with expectations showing that the disinflationary trends related to Goods disinflation in 2023 are running out of steam, and it will now be up to housing, wages and the service sector to finish the disinflationary story in the coming year. Last week’s message from the Fed highlighted two camps that are forming within the Fed – The Powell Camp and The Waller Camp. Powell, restated his case last week that he believes the disinflationary trends will persist, although along a bumpy path. Waller, showed another side of the Fed, one that is concerned that disinflationary trends will stall in the coming year. What this means for interest rates this year is the difference between three rate cuts, or as few as zero rate cuts. What this means for equities, however, may be subtle. Either way growth wins, either by virtue of being goosed by lower rates, or by being driven by spending.

Although the path for the remainder of the year will not be linear, there are few negative catalysts showing their faces.

- PCE release highlighted the disinflationary handoff that needs to happen between goods and services

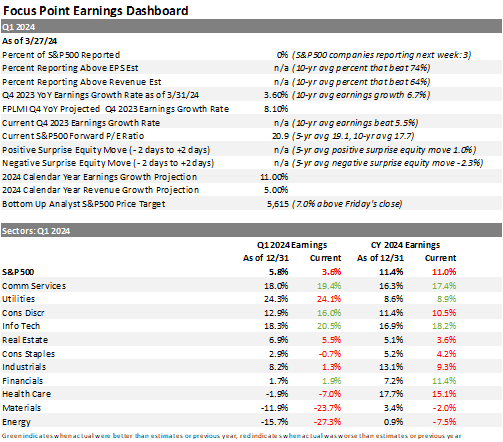

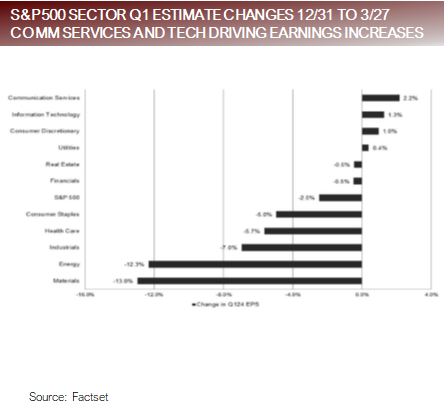

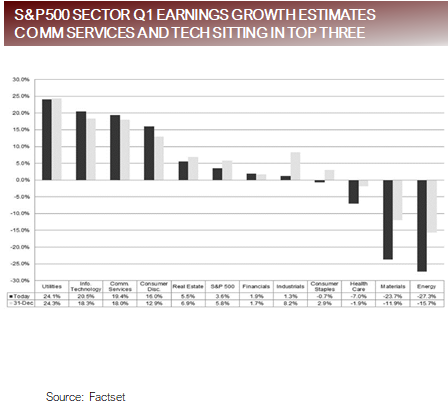

- Preview of Q1 2024 earnings season: Growth still expecting to being led by Comm Services and Tech

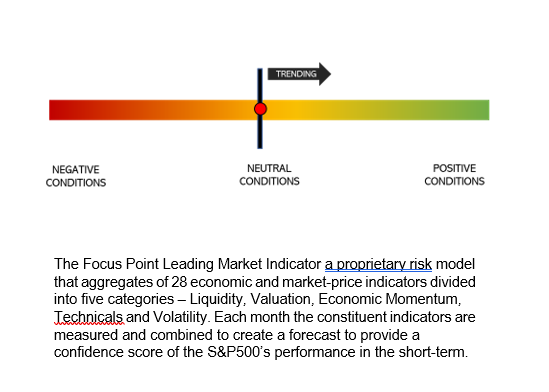

- The Focus Point Leading Market Indicator ticks slightly higher at month end driven by loosening financial conditions

- The most Frequently Asked Question from clients this week: Do higher interest rates matter to the economy?

- Focus Point Sector Rotation Update: Extreme momentum signal indicates a slow grind higher could continue

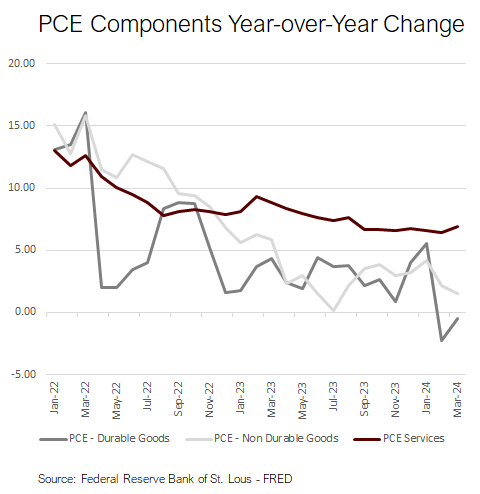

PCE highlighted the disinflationary handoff that needs to happen between goods and services

- The headline month-over-month PCE printed 3%, which came in slightly below the consensus estimate of 0.4%. While the year- over-year headline and core PCE printed inline with consensus estimates, at 2.5% and 2.8%, respectively. The year-over-year numbers did not dip below the estimate because the prior month was revised higher. The net was, everything was pretty much inline with estimates, which does little to motivate the Fed to move.

- The bigger pictures is represented on the chart to the right, which represent the annual change in the three largest components of PCE, Durable Goods (furnishings, motor vehicles, recreational goods…), Non-Durable Goods (clothing, food and beverages, gasoline..) and Services. Key in this chart is that Services have not budged since last fall, the sole story is about goods. Durable goods have actually been experiencing deflation. For the PCE story to continue to unfold in a favorable direction to support rate cuts, services must join the disinflationary bandwagon. However, note Services are actually moving higher at the moment.

Putting it all together

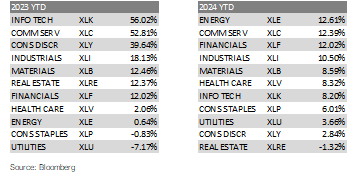

- Looking at equity index performance over the first three months of 2024, it looks a lot like a continuation of the trends of 2023. However, looking underneath the surface there have been a lot of changes.

- Ten out of eleven sectors are up on the year, with S&P500 up 10.55%. The average sector is up 7.62%, and the median sector is up 8.32%. To give this some perspective against last year, the median sector last year was about 6% lower than the average, suggesting that performance was driven by a chosen few at the top last year, while much more evenly distributed this year. The same trends, though not detailed here, are true across market caps and international geographies.

- In addition to the broadening out story, the other trends impacting markets this year have included:

- Continued consumer spending supporting corporate profits, despite signs that the labor markets are softening.

- A reawakening of global manufacturing survey data, possibly signaling a transition away from recessionary mindsets.

- Stagnant disinflationary trends calling into question, if and when, inflation will return to the Fed’s target inflation rate.

- A rift appearing within the Fed with one side believing in the disinflationary trends of yesteryear, and the other side skeptical that the disinflationary trends will persist. Net these together and we have a lower expectation for rate cuts.

For more news, information, and analysis, visit VettaFi | ETF Trends.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Focus Point Capital

Read more commentaries by Focus Point Capital