We recently highlighted how Chinese equities have fallen out of favor, amid lingering economic concerns. Investors have turned sour on prospects for China’s growth, reflected in elevated capital outflows.

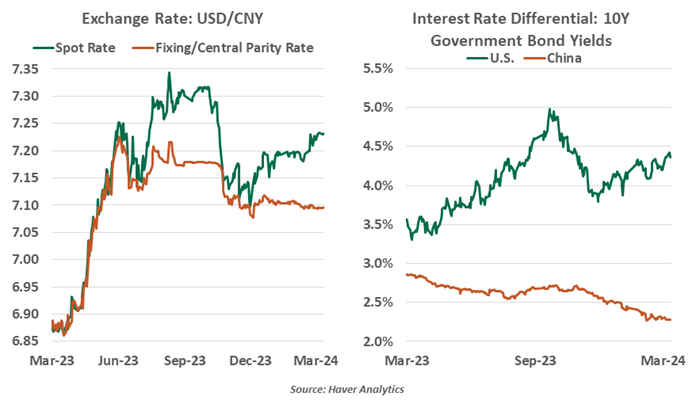

The apprehension appears to have spread to currency markets. The Chinese yuan (CNY) breached 7.2 against the dollar last month, a level that policymakers had been defending for months. The CNY is not free-floating like other major currencies: it is actively managed by China’s central bank (the PBoC). The PBoC establishes a starting level (or fixing) each day, and the yuan is allowed to trade 2% above or below the fixing.

The CNY has been trading close to the weaker end of the of its daily band in recent weeks. The yuan’s poor run is largely explained by the widening U.S.-China interest rate differential. U.S. Treasuries are offering much higher yields than those in China, driving investors toward American bond markets. Prospects of a delayed and more gradual easing cycle by the Fed, along with expectations of proximate easing from the PBoC, have added to the downward pressure.

A weak currency should be good news for an economy which is referred to as the world’s factory, as it could help China export its way out of trouble. But Chinese exports are already garnering increased scrutiny from the West. Concerns over excess production and dumping were at the core of talks during U.S. Treasury Secretary Yellen’s recent visit to Beijing. By allowing the CNY to depreciate further, China faces the risk of being labeled a currency manipulator by the U.S., a declaration that would initiate additional trade restrictions.

Lasting currency weakness will further dent sentiment, as the yuan is often considered an indicator of confidence in China’s domestic economy, and make Chinese equities even less attractive for global investors.

These factors explain why the appetite for another bout of currency depreciation is low. The PBoC has been continuously setting a stronger fixing to support the yuan.

LETTING THE CNY DEPRECIATE WOULD DO MORE HARM THAN GOOD TO THE CHINESE ECONOMY.

One simple way for central banks to prop up the value of their currencies is by raising interest rates. The PBoC lacks that option, as it has been forced to ease rates in an attempt to stimulate activity. Instead, policymakers have been relying on tools such as asking state-owned banks to sell dollars to prop up the value of the CNY. As in the past, the PBoC can also cut banks’ foreign currency reserve ratio and boost the cost of shorting the currency.

Another potential action step would be to tighten controls over its capital account. Substantial amounts of money have been departing China, on the instruction of both foreign and domestic investors. Bringing the gates down would stop the flow, but such an action could be seen as a desperate measure. It would also make attracting new investment much more difficult.

With the Fed unlikely to cut before September 2024 and China trying to fend off deflation, the pressure on the currency is likely to persist in the near term. While some see manipulation behind the yuan’s decline, it is more likely the result of natural causes. The United States, and China’s other trading partners, should keep this in mind.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2024 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© Northern Trust

Read more commentaries by Northern Trust