“Now Youse Can’t Leave”: What ‘A Bronx Tale’ Taught Me About Macro Economics

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits"I will never forget the look on their faces. All eight of them. Their faces dropped. All their courage and strength was drained right from their bodies. They had a reputation for breaking up bars, but they knew that instant, they'd made a fatal mistake. This time they walked into the wrong bar."

‘C’ Anello [Narrating]

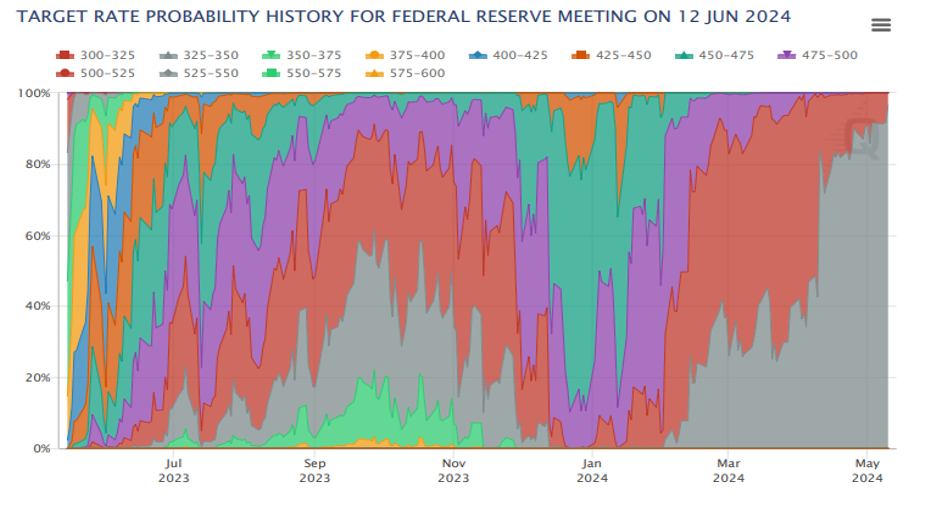

With a few tweaks to this quote, it could capture the sentiment of many Fed Watchers over the past several months reacting to economic releases. It feels like every other week corporate news pundits are justifying a stock market whipsaw with “bad news is good news, but sometimes, bad news is bad news” when trying to predict a rate cut. It would be more entertaining, and just as informative, to watch a blind folded Jim Cramer call a tight horserace through the last furlong between ‘Hard Landing’, ‘Soft Landing’, and ‘No Landing.’

The last rate hike came mid-summer 2023, signaling that the Fed felt like it had done enough heavy lifting to coast back to a ~2% CPI, and the Market’s year-end expectation for the upcoming June meeting was that there would be about .75% worth of rate cuts by then.

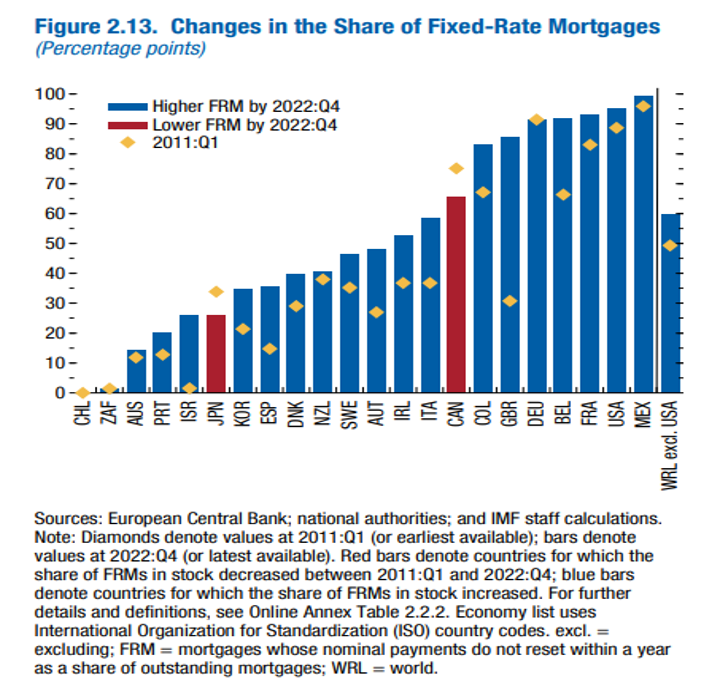

So, what gives? How did the market end up tripping on its own shoelaces while taking a premature victory lap? One possible explanation could be found in the IMF’s April ’24 World Economic Outlook. In “Chapter 2: Feeling the Pinch? Tracing the Effects of Monetary Policy through Housing Markets,” the authors investigate how monetary policy (raising and cutting central bank rates) impacts national consumption through the transfer mechanism of housing prices. One of their findings was that national consumption in countries with a high proportion of fixed-rate mortgages was significantly less curtailed in a rising rate environment than in countries that had a lower proportion of fixed-rate mortgages. Though inflation is not explicitly referenced in this paper, one could reasonably connect the dots that countries with a higher proportion of fixed-rate mortgages should see less of an impact on demand driven inflation as their central banks raise rates to cool down the economy; the rationale being that the average person’s largest source of debt is their house. So, someone with fixed debt payments is less likely to feel the intended squeeze from higher borrowing costs until their rate resets.

The ‘until’ part here is very important to note. For most Americans, ‘until’ on their credit cards is the next billing cycle, about every five years for their car loans, and for home owners ‘until’ likely won’t happen unless they buy a new house, if ever again. That’s the key insight. The 30-year fixed rate mortgage is a uniquely American feature. Not only is a fixed rate mortgage less common in the rest of the developed world (though its popularity is growing post Great Financial Crisis), but even where it is more common, the rates generally reset every few years, even if the borrower has 10 to 20 years to pay back the loan. While the below chart from the IMF does not account for the duration of the locked in rates, defining FRM as anything longer than a year to reset, it emphasizes the pickle the Fed finds itself in versus the rest of the world in using rates to curb demand driven inflation.

When combining the high home ownership rate in the U.S. with the high proportion of fixed rate mortgages, it helps paint a picture as to why Jerome Powell’s tone has changed to “higher for longer” while some of our major trade partners are preparing to ease rates. The gut-wrenching reality is that the rest of the world may be ready to bounce back from economic slowdowns with pent up demand for credit while the U.S. digs in for a war of attrition between economic output and price stability, in other words stagflation. A quick look back in history hints that the U.S. stock market could face some headwinds compared to other major countries if this proves to be the case. Note that during America’s last bout with stagflation in the 70’s, the S&P 500 only outperformed Germany (DAX) and Australia (AS30) while lagging Japan (NKY), Canada (SPTSX), and UK (ASX).

That’s a bit of a gloomy prospect for the U.S. markets if the wait for rate cuts drags out. With a historically low unemployment rate, Powell likely has more time on his side to wait out homeowners to fall on hard times, relocate for work, start families, or any other reason why someone would need a new house versus want a new house. At the very least he has shorter term business, credit card, and car loan resets working in his favor that would ultimately lead to businesses closing and higher monthly payments on the smaller debt; a death by a thousand cuts to the consumer, though those channels of crimping spending may take longer to feel the full effects. The threat of higher rates and pain to the economy should have been enough to curb spending, but in today’s America what’s the fun of saving money if you can’t spend it, right? We could be stuck here for a while.

It’s reminiscent of that classic scene in A Bronx Tale preceding that quote from earlier. Americans had the chance to fall in line but snubbed the Fed’s expectation that they would play nice. Jerome Powell already locked the front door.

Now youse can’t leave.

Tony Jacoby, CFA is a portfolio manager at Shelton Capital Management.

Important Information

It is possible to lose money by investing in a fund. Past performance does not guarantee future results. Investors should consider a fund’s investment objectives, risks, charges and expenses carefully before investing. The prospectus contains this and other information about a fund. To obtain a prospectus, visit www.sheltoncap.com or call (800) 955-9988. A prospectus should be read carefully before investing. Mutual fund investing involves risk, including possible loss of principal.

Shelton Funds are distributed by RFS Partners, a member of FINRA and affiliate of Shelton Capital Management.

INVESTMENTS ARE NOT FDIC INSURED OR BANK GUARANTEED AND MAY LOSE VALUE.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Live Virtual Event: Join Now

Upcoming Virtual Events View All