Haywire Labor Data Points in Every Direction

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThought to Ponder ...

“I think of all the people I have spoken to who have said, ‘When I know exactly what the next thing is, I will make a move.’ I think of all the people whom I have taught to track who froze when they lost the track, wanting to be certain of the right path forward before they would move. Trackers try things. The tracker on a lost track enters a process of rediscovery that is fluid. He relies on a process of elimination, inquiry, confirmation; a process of discovery and feedback. He enters a ritual of focused attention. As paradoxical as it sounds, going down a path and not finding a track is part of finding the track. Alex and Renias call this ‘the path of not here.’ No action is considered a waste, and the key is to keep moving, readjusting, welcoming feedback. The path of not here is part of the path of here.”

-- Boyd Varty, "The Lion Tracker's Guide to Life"

The View from 30,000 feet

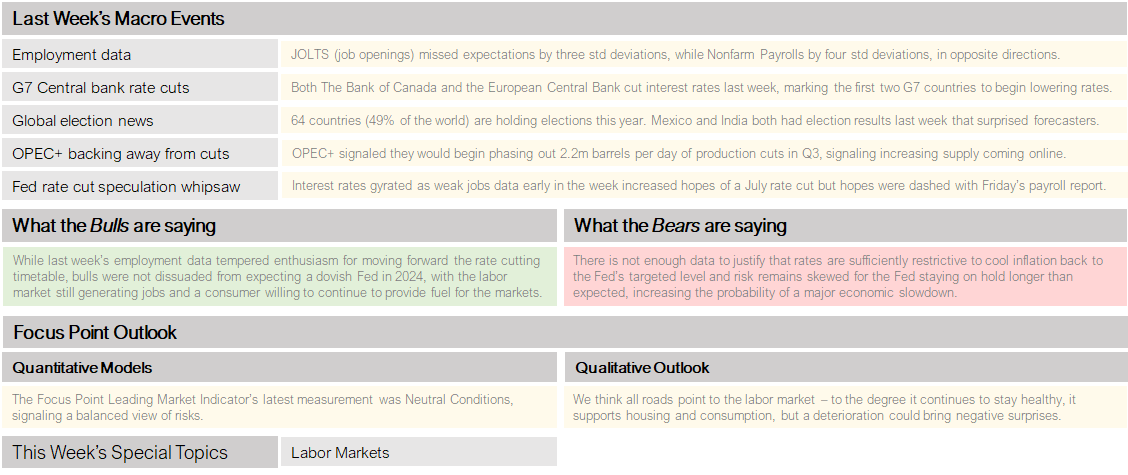

Employment Data

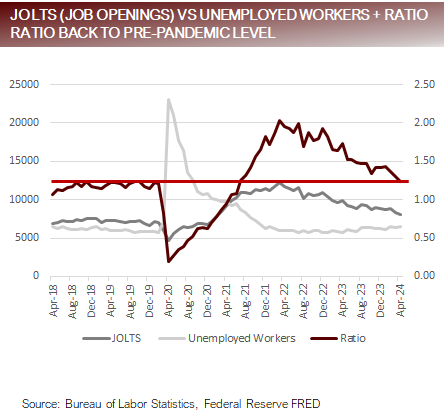

- JOLTS (job opening data) had a massive surprise, three standard deviations below consensus estimates, the driving job openings to unemployed workers ratio back to pre-pandemic levels.

- From Powell press conference May 1, 2024. “I think there’s also other paths that the economy could take, which, which would cause us to want to consider rate And those would be—two of those paths would be that we do gain greater confidence, as we’ve said, that inflation is moving sustainably down to 2 percent, and another path could be, you know, an unexpected weakening in the labor market, for example.”

- The euphoria the JOLTS report didn’t last for long because on Friday Nonfarm Payrolls (Establishment Survey) surprised four standard deviations above consensus estimates, indicating that 272k jobs had been created last month.

- However, concerns about strength were muted by the Unemployment Rate (Household Survey), that rose to 4.0%, calling into question the validity of contradicting survey data.

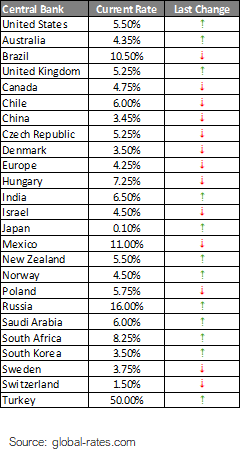

G7 central bank rate cuts

- Taking a sampling of 25 of the largest central banks in the world, last week we crossed a threshold of over half of the central banks in the group easing.

- Last week also marked the first rates cuts by the G7, with both the Bank of Canada and the European Central Bank cutting rates. Significant comments from the BoC and ECB indicating tone surrounding rate cuts included:

Bank of Canada

- “continued downward momentum” expected for BoC “no longer needs to be restrictive”

- “increased our confidence that inflation will continue to move towards the 2% target.”

European Central Bank

- “While still elevated, we are seeing those wages on a declining path

- If it (the neutral rate) has increased compared to where it was before Covid, we also know that we are far away from a neutral rate now. By moving from 4% to 3.75%, we are not close to the neutral We still have a way to go.“

- Overall viewed as a “hawkish cut”, with no future commitments, and many references to data dependency

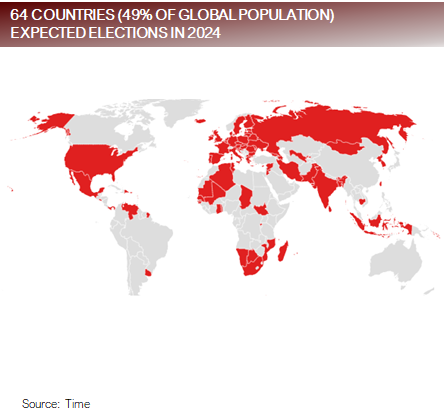

Global Election News

- Americans captivated by their own bizarre election dynamics, pitting what opposing parties are portraying as a showdown between a convicted felon and senile octogenarian got a taste of the types of market volatility that can be associated with an election surprise.

- For our part, Focus Point’s largest concern is that the election in the US later this year will be contested by the In a best case this represents a delay and recounts, as the markets wring their hands, and in a worst case, it could represent a replay of the theatrics of January 6th with wider scale violence.

Mexico

Sheimbaum’s win was widely expected, what was not was the landslide victory of her party in other parts of the government, that could create a less business friendly political environment.

India

Modi win was also widely expected, but the opposite of Mexico, his ruling coalition’s power was surprisingly diminished, potentially limiting power for his unprecedented third term.

OPEC+ backing away from cuts

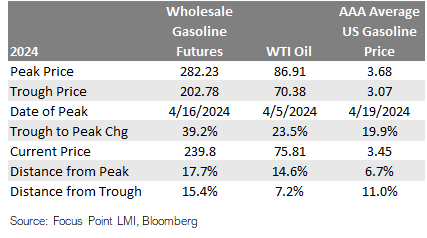

- Eight OPEC+ nations agreed last week to begin reducing production cuts of 2 million barrels of oil a day starting in October. The increases in production would be phased in, with 500,000 barrels per day by the end of 2024.

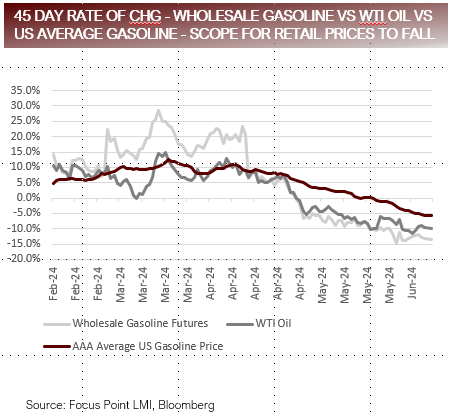

- Since the peak of oil and gasoline prices in April the AAA Average National Gasoline Price has fallen relatively less than oil or wholesale gasoline futures, suggesting further potential downside at the pump which is good news for CPI.

Fed rate cut speculation whipsaw

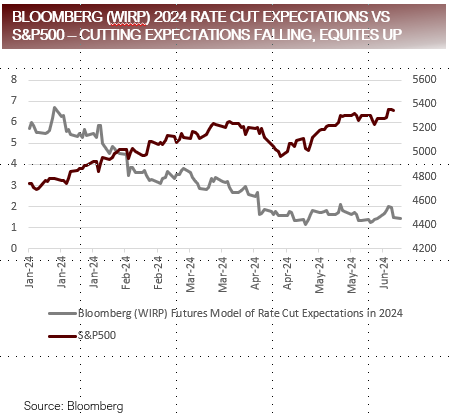

- At the peak of optimism about Fed rate cuts in 2024 on January 12th, the Bloomberg Model for Rate Cut Expectations calculated there were 6.7 rate cuts factored in for 2024.

- At the peak of pessimism about Fed rate cuts in 2024 on April 30th, the Bloomberg Model for rate Cut Expectations calculated there were 1.1 rates cuts factored in for 2024.

- Between Jan 12 and Jun 7, the S&P500 rose from 4784 to 5347, an increase of 8%, while the 10-yr Treasury yield moved from 3.94 to 4.45. The big picture is, rates are significantly higher, equities are significantly higher, and rate cut expectations have fallen.

- This tells us something else is at play driving markets higher. That something is earnings. The Price-to-Earnings on the S&P500 has fallen in this same window has gone from 22.2x to 22.1x. Meaning, as the S&P500 has gone higher in price it has become less expensive on a valuation basis.

SPECIAL TOPIC: Labor Markets

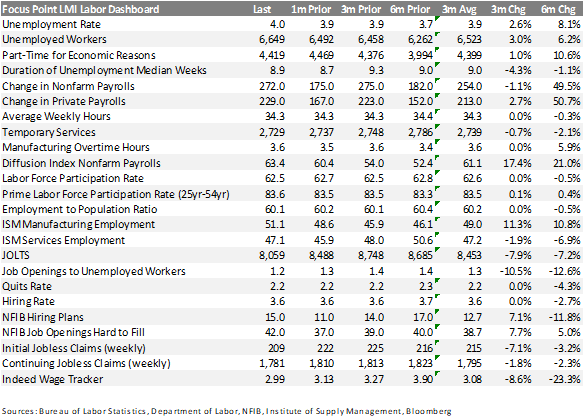

- Trends in labor markets have been Out of the 24 data sets we measure to evaluate the health of the labor markets, 8 are now improving, 4 are neutral and 12 are deteriorating, which is a steady improvement over the last three months.

- Key take-aways from the data include:

- Part-Time Workers for Economic Reason has been rising along with Nonfarm Payrolls, indicating there may be a double counting driving the increase in Nonfarm Payrolls because part-time workers could be counted twice.

- The steady increase in the Diffusion Index of Nonfarm Payrolls along with rising Labor Force Participation for Prime Age, are trends indicating strength in the labor force.

- There has been a recent uptick in hiring plans of small businesses, while at the same time the same group surveyed indicates job openings are hard to fill.

- Survey data from JOLTS report, in particular, has been weak.

- There have been a lot of questions raised in the last week about the possible adjustments to Nonfarm Payrolls once the Quarterly Census of Employment and Wages (QCEW) is completed in August, with expectations for large revisions lower.

Pulling it it all together

- Global central banks last week confirmed the direction of rates: They didn’t do much to confirm the pace of movement.

- Real rates have been over 2% for over a year. Historically real rates at this level has been associated with overly restrictive monetary policy which eventually causes excessive strain in the system. As inflation comes down the Fed, along with other global central banks, would like to reduce rates because if they don’t, falling inflation will cause real rates to move even higher causing policy to become more restrictive, which is not what they are trying to accomplish at this point in the game.

- Another key take-away from last week is that elections can be major sources of With three options for an election in the US being, a Biden victory, a Trump victory, or a contested election, the markets have not yet begun to price in the third of these scenarios, which may be the most likely.

- Markets have been fighting a wall of worry in 2024, with equities rising as expectations for rate cuts have been Equities have been able to sustain momentum because earnings have carried the day, and despite being nearly 500 points higher than it was in January, the S&P500 is now trading at a lower valuation because earnings have risen.

- We continue to lean bullish from the neutral until we see a confirmed deterioration in the employment market that starts to erode expectations for consumption and earnings growth.

- We are less optimistic that the pace of gains we saw in the first half of the year will continue because consensus expectations have moved significantly higher since the beginning of the year, so there is a much higher bar for earnings or GDP to This is not necessarily negative but points to a more tempered pace of equity appreciation that is prone for bouts of disappointment.

For more news, information, and strategy, visit the Innovative ETFs Channel.

DISCLOSURES AND IMPORTANT RISK INFORMATION

Performance data quoted represents past performance, which is not a guarantee of future results. No representation is made that a client will, or is likely to, achieve positive returns, avoid losses, or experience returns similar to those shown or experienced in the past.

Focus Point LMI LLC

For more information, please visit www.focuspointlmi.com or contact us at [email protected] Copyright 2024, Focus Point LMI LLC. All rights reserved.

The text, images and other materials contained or displayed on any Focus Point LMI LLC Inc. product, service, report, e-mail or web site are proprietary to Focus Point LMI LLC Inc. and constitute valuable intellectual property and copyright. No material from any part of any Focus Point LMI LLC Inc. website may be downloaded, transmitted, broadcast, transferred, assigned, reproduced or in any other way used or otherwise disseminated in any form to any person or entity, without the explicit written consent of Focus Point LMI LLC Inc. All unauthorized reproduction or other use of material from Focus Point LMI LLC Inc. shall be deemed willful infringement(s) of Focus Point LMI LLC Inc. copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Focus Point LMI LLC Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Focus Point LMI LLC Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.

All unauthorized use of material shall be deemed willful infringement of Focus Point LMI LLC Inc. copyright and other proprietary and intellectual property rights. While Focus Point LMI LLC will use its reasonable best efforts to provide accurate and informative Information Services to Subscriber, Focus Point LMI LLC but cannot guarantee the accuracy, relevance and/or completeness of the Information Services, or other information used in connection therewith. Focus Point LMI LLC, its affiliates, shareholders, directors, officers, and employees shall have no liability, contingent or otherwise, for any claims or damages arising in connection with (i) the use by Subscriber of the Information Services and/or (ii) any errors, omissions or inaccuracies in the Information Services. The Information Services are provided for the benefit of the Subscriber. It is not to be used or otherwise relied on by any other person. Some of the data contained in this publication may have been obtained from The Federal Reserve, Bloomberg Barclays Indices; Bloomberg Finance L.P.; CBRE Inc.; IHS Markit; MSCI Inc. Neither MSCI Inc. nor any other party involved in or related to compiling, computing or creating the MSCI Inc. data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such data. Such party, its affiliates and suppliers (“Content Providers”) do not guarantee the accuracy, adequacy, completeness, timeliness or availability of any Content and are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, or for the results obtained from the use of such Content. In no event shall Content Providers be liable for any damages, costs, expenses, legal fees, or losses (including lost income or lost profit and opportunity costs) in connection with any use of the Content. A reference to a particular investment or security, a rating or any observation concerning an investment that is part of the Content is not a recommendation to buy, sell or hold such investment or security, does not address the suitability of an investment or security and should not be relied on as investment advice.

This communication reflects our analysts’ current opinions and may be updated as views or information change. Past results do not guarantee future performance. Business and market conditions, laws, regulations, and other factors affecting performance all change over time, which could change the status of the information in this publication. Using any graph, chart, formula, model, or other device to assist in making investment decisions presents many difficulties and their effectiveness has significant limitations, including that prior patterns may not repeat themselves and market participants using such devices can impact the market in a way that changes their effectiveness. Focus Point LMI LLC believes no individual graph, chart, formula, model, or other device should be used as the sole basis for any investment decision. Focus Point LMI LLC or its affiliated companies or their respective shareholders, directors, officers and/or employees, may have long or short positions in the securities discussed herein and may purchase or sell such securities without notice. Neither Focus Point LMI LLC nor the author is rendering investment, tax, or legal advice, nor offering individualized advice tailored to any specific portfolio or to any individual’s particular suitability or needs. Investors should seek professional investment, tax, legal, and accounting advice prior to making investment decisions. Focus Point LMI LLC’s publications do not constitute an offer to sell any security, nor a solicitation of an offer to buy any security. They are designed to provide information, data and analysis believed to be accurate, but they are not guaranteed and are provided “as is” without warranty of any kind, either express or implied.

FOCUS POINT LMI LLC DISCLAIMS ANY AND ALL EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY, SUITABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE.

Focus Point LMI LLC, its affiliates, officers, or employees, and any third-party data provider shall not have any liability for any loss sustained by anyone who has relied on the information contained in any Focus Point LMI LLC publication, and they shall not be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits and opportunity costs) in connection with any use of the information or opinions contained Focus Point LMI LLC publications even if advised of the possibility of such damages.

A message from Advisor Perspectives and VettaFi: Join us on June 27 for the Midyear Market Outlook Symposium, where advisors will gain insights into macroeconomic trends, active ETFs, investing abroad, and more to navigate 2024's challenges.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All